Can the Tesla Robotaxi still meet high autonomy expectations despite accidents, valuation risks, and frustration in Europe?

How is the Tesla Robotaxi performing after recent accidents?

The focus of the markets is currently on the Tesla Robotaxi, which has been operating in Austin with a small fleet since June 2025. Recently, five more accidents were reported, bringing the total number of crashes since launch to 14. While this may seem manageable at first glance, statistically, this results in an accident every 57,000 miles—significantly worse than the approximately 229,000 miles per crash for average U.S. drivers and about 500,000 miles according to data from the traffic safety authority for police-reported accidents. Notably, despite having a safety driver in the front seat, the Tesla Robotaxi performs four to eight times worse than human drivers.

At the same time, the company is struggling for regulatory clarity. In California, Tesla argues that the Robotaxi operation does not fully fall under the state’s rules for autonomous vehicles, as safety drivers and remote assistants are involved. Concurrently, the company is resisting restrictions on marketing terms such as “driverless,” “self-driving,” or “Robotaxi,” after previously suffering a defeat in a case regarding “Autopilot” and “Full Self-Driving.” This complex situation raises doubts about whether the Tesla Robotaxi is ready for a broad rollout.

What role does the Tesla Robotaxi play in Tesla’s extremely high valuation?

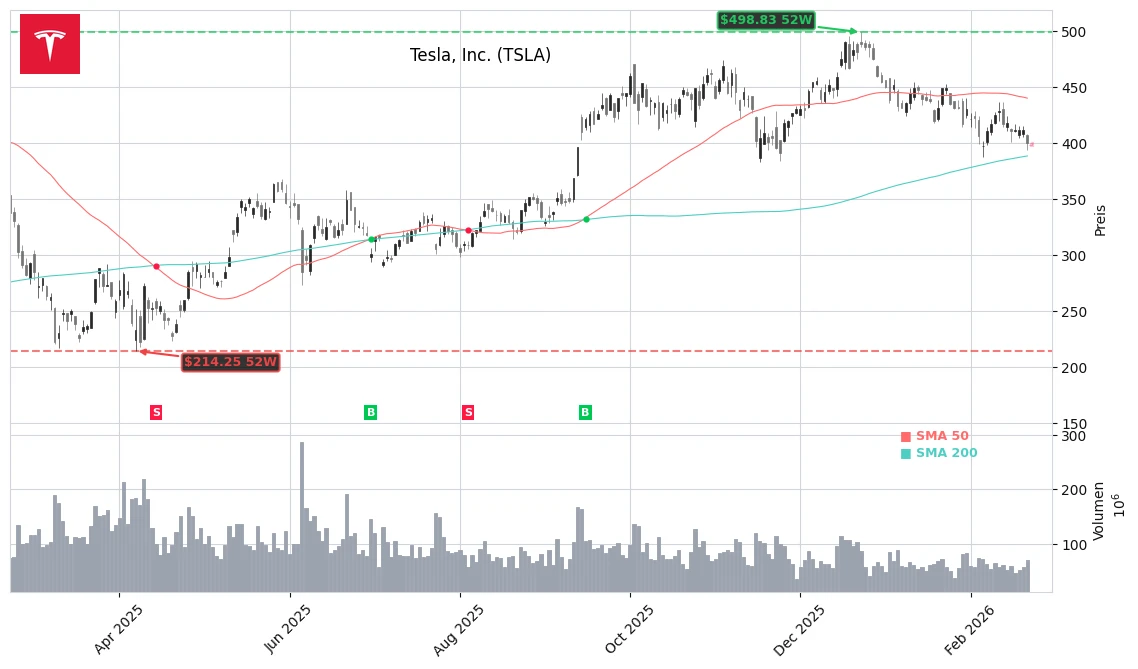

Despite all the risks, many investors are betting that the Tesla Robotaxi will eventually become a high-margin platform business. The stock is trading at a very high price-to-earnings ratio; some estimates suggest a forward P/E ratio in the high triple digits for 2026. This includes not only a profitable electric vehicle and energy storage manufacturer but also a scaled ride-hailing service based on the Tesla Robotaxi and software revenues from FSD subscriptions.

At the same time, the traditional EV business is stagnating. Deliveries in Europe have recently fallen sharply, operational margins are under pressure, and the stock is back below $400 despite AI hype. Additionally, there is a massive investment plan: For 2026, Tesla is budgeting over $20 billion in investments, following $8.5 billion in 2025. These funds are intended primarily for AI data centers, Cybercab production lines, expansion of the Robotaxi fleet, and new AI-capable assets. If the Tesla Robotaxi fails to deliver safety and scalability in a timely manner, the stock may face a significant valuation discount given these high expectations.

How is Tesla performing in Europe?

While Tesla focuses on autonomy and software in the U.S., the company is increasingly under pressure in Europe. New registrations fell by 17% in January to just around 8,000 vehicles—the 13th consecutive decline. The market share in the region, including the EU, UK, Switzerland, Norway, and Iceland, dropped to just 0.8%. Industry observers point to several factors: the model portfolio is aging, affordable EVs from competitors like BYD, MG, or Zeekr are gaining market share, and a large stock of leasing returns is putting downward pressure on used car prices. In many countries, buyers can now relatively easily opt for used Teslas, further slowing new car sales.

Additionally, reputational damage is compounded—both from discussions around Autopilot and the Tesla Robotaxi, as well as the political polarization surrounding Elon Musk. For Tesla, this means that the growth story in Europe relies more than ever on new products and a convincing AI strategy—mere price reductions no longer seem sufficient.

Can Optimus secure the bet on autonomy?

Alongside the Tesla Robotaxi, the humanoid robot Optimus is becoming central to the strategy. Tesla is converting parts of the Fremont factory from producing models S and X to a production line for Optimus. Musk plans a long-term capacity of up to one million robots per year. The business model resembles the combination of hardware plus subscription that Tesla already pursues with its vehicles: one-time acquisition costs for the robot, supplemented by ongoing software and service revenues as Optimus learns new skills or is integrated into different work environments.

Bottom Line

On the stock market, Optimus is increasingly seen as the second major AI pillar alongside the Tesla Robotaxi, which offers significant profit potential in the long run. However, in the short term, its contribution remains limited: Optimus is still in the development phase and is currently only deployed in Tesla factories to learn routine tasks. For investors, this means: the potential is great, but the proof of commercial scalability is still outstanding.

Related Sources

- Tesla, Inc. – Stock Price and Metrics (Yahoo Finance)

- Tesla has a Robotaxi problem, and that’s bad news for the stock (The Motley Fool)

- Below $400 Again, Is Tesla Stock a Buy? (The Motley Fool)

- Tesla’s Europe problem keeps getting worse (CNBC)