Is the latest bullish Texas Instruments Forecast the start of a durable analog upcycle or just another short-lived semiconductor bounce?

How does the Texas Instruments Forecast change after Stifel?

Stifel analyst Tore Svanberg moved Texas Instruments to Buy from Hold and raised the firm’s price target to $250 from $215, implying roughly 16% upside from the previous close. The upgrade comes after a six-year investment cycle in which Texas Instruments poured heavy capital into expanding its manufacturing footprint, pressuring profitability and free cash flow. Stifel now argues that this spending phase is largely behind the company, setting up an analog “upcycle” where higher volumes and better utilization can drive margins and cash generation.

The new Texas Instruments Forecast from Stifel highlights “multiple tailwinds,” including recovering demand for everyday analog chips across industrial and automotive end markets, stronger pricing power in specialty products, and a more favorable supply-demand balance after years of capacity constraints. The call helped push TXN up about 2.8% on Thursday, extending gains after a 4%–5% jump earlier in the week tied to improving sector sentiment and expectations for a stronger Q1 2026 update.

Despite Stifel’s bullish stance, the broader analyst community still leans neutral. Many on Wall Street maintain Hold ratings, pointing to a trailing P/E near the high 30s and recent earnings misses that left some investors cautious. The Texas Instruments Forecast now rests on whether the company can translate its heavy capex and diversified customer base into a clear inflection in free cash flow over the next 12–24 months.

What sets Texas Instruments apart from NVIDIA and Apple?

Compared with high-flying AI names like NVIDIA and ecosystem giants like Apple, Texas Instruments plays a quieter but critical role in the semiconductor stack. The company focuses on analog chips and embedded processors that go into industrial machinery, factory automation, automotive systems, power management, and consumer electronics. These products typically have long life cycles, recurring demand, and less abrupt pricing swings than leading-edge GPUs.

That profile has attracted long-term growth managers. ClearBridge’s Large Cap Growth Strategy, for example, initiated a TXN position in Q1 2026, emphasizing the company’s “unique free cash flow story” and the fact that 30%–40% of its customer base sits in industrials. For investors who already have aggressive exposure to AI beneficiaries such as NVIDIA or EV names like Tesla, TXN offers a way to balance portfolios with a more predictable, cash-generative semiconductor business once the current lull passes.

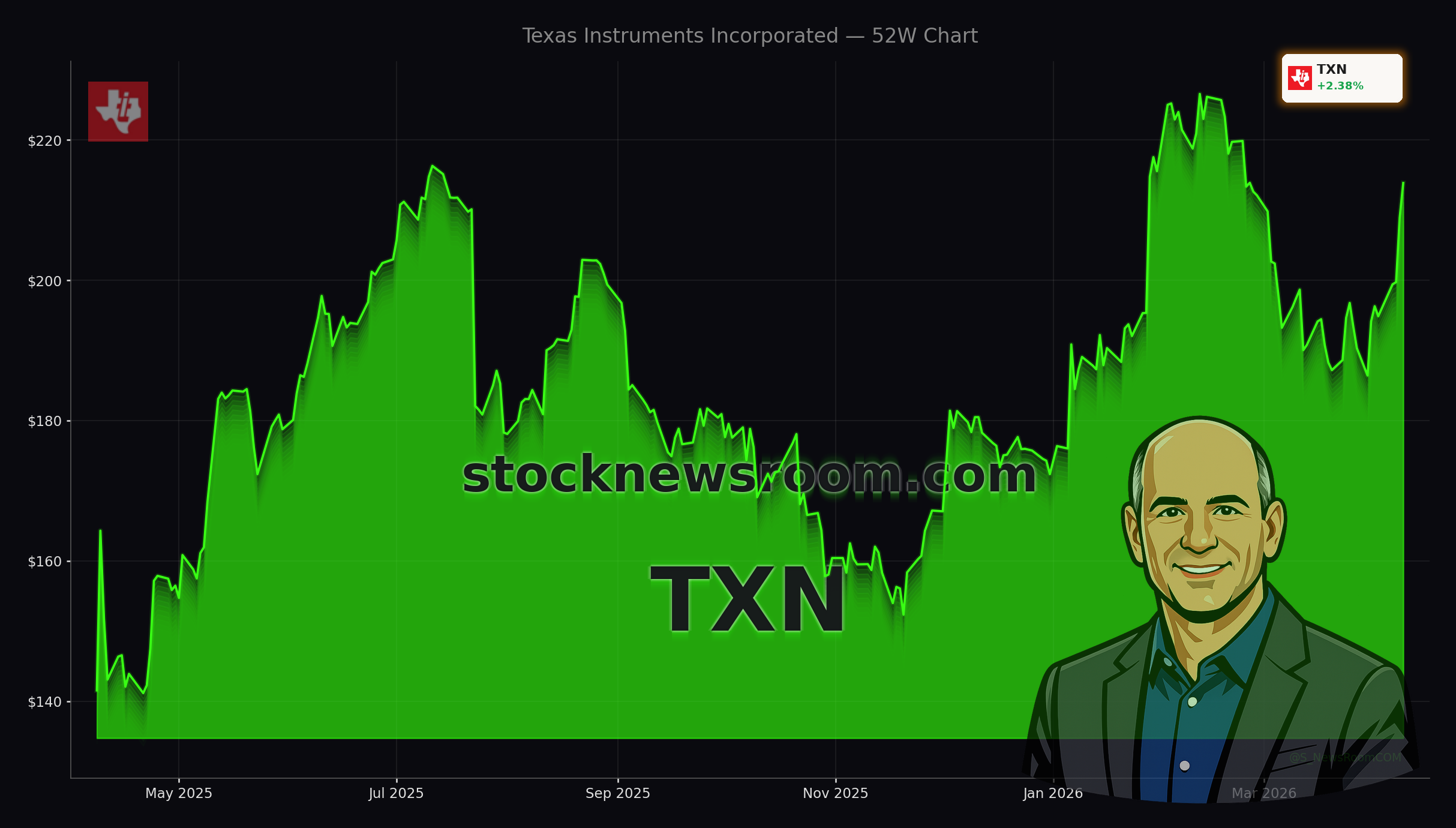

Still, the Texas Instruments Forecast is not risk-free. Some institutional holders, including Hunter Associates Investment Management and CCLA Investment Management, trimmed stakes in late 2025 and early 2026, signaling that not all fund managers are comfortable with valuation and near-term earnings visibility. Mixed positioning across funds underscores that investors are debating how much of the eventual recovery is already priced into a stock that is more than 30% higher over the last 12 months and trading not far below its 52-week high.

Is the Texas Instruments Forecast supported by fundamentals?

Fundamentally, the bullish Texas Instruments Forecast rests on three pillars: normalized free cash flow, industrial and automotive growth, and the strength of its vertically integrated manufacturing model. The company has spent years bringing more production in-house, which improves control over quality and supply but temporarily depressed cash flow due to elevated capex. As utilization rises and capex moderates, both Stifel and active managers expect free cash flow to improve “meaningfully,” supporting dividends and potential buybacks.

Texas Instruments already has a reputation on Wall Street for a robust dividend track record, which appeals to income-focused investors searching for yield in the technology sector. The stock’s current move above key technical support levels, along with a recent surge in price momentum, has drawn in short-term traders as well. Technical research points to important support near the low $200s and resistance in the high $210s to low $220s, a range that the Stifel upgrade could help the stock break through if follow-up earnings and guidance cooperate.

Sector-wide trends are also helping. Semiconductor industry forecasts now point toward roughly $1.3 trillion in revenue by 2026, with AI infrastructure, EVs, and industrial automation driving demand. While high-performance computing remains dominated by players like NVIDIA, the broader build-out requires large volumes of reliable analog and power-management chips—the exact niches where Texas Instruments has a leading share. That backdrop lends credibility to a constructive Texas Instruments Forecast as cyclical headwinds in PCs and consumer electronics fade.

How should U.S. investors position around Texas Instruments?

For U.S. investors, TXN is increasingly viewed as a core holding in the analog and mixed-signal segment of the S&P 500’s technology sleeve rather than a high-beta growth trade. The average Wall Street price target around the low-to-mid $210s suggests modest near-term upside, but Stifel’s $250 target and other bullish analyses argue that consensus may be too conservative if the free cash flow ramp materializes. Hedge fund ownership has also ticked higher, with more portfolios adding or increasing stakes into late 2025.

Given the elevated valuation, some managers rotate partially into higher-beta AI names or cyclical plays, while others prefer the steadier profile of Texas Instruments relative to mega-cap innovators such as Apple. The latest Texas Instruments Forecast effectively sharpens this debate: is the stock a premium-priced defensive within semis, or a still-underappreciated cash-flow compounder heading into its next analog upcycle?

We believe Texas Instruments is exiting a heavy investment phase and entering an analog upcycle that can drive stronger free cash flow and market share gains.— Tore Svanberg, Stifel analyst

Investors will get more clarity with the upcoming Q1 2026 earnings release and guidance. Management commentary on order trends in industrial, automotive, and communications, as well as updated capex plans, will be crucial in confirming or challenging the increasingly optimistic Texas Instruments Forecast now circulating on Wall Street.