Can record TSMC Earnings powered by AI demand keep driving chip stocks higher, or is the market already pricing in perfection?

How strong were TSMC Earnings this quarter?

Taiwan Semiconductor Manufacturing Co. posted first‑quarter revenue of 1.13 trillion New Taiwan dollars, or about $35.6 billion, up roughly 35% year over year and marginally above consensus estimates around NT$1.12 trillion. March alone was striking, with sales jumping 45.2% from a year earlier, underscoring the powerful tailwind from AI accelerators and high‑performance compute chips. Early commentary out of the company suggests demand at the 3‑nanometer and 5‑nanometer nodes remains particularly tight, driven by cloud AI build‑outs and networking silicon.

On Wall Street, expectations for the full TSMC Earnings release on April 16 are high. Analysts are looking for approximately $35.5 billion in revenue and earnings per share near $3.26, implying that gross margins could land in the mid‑60% range, potentially a record. Management has previously guided to a full‑year growth target of at least 30%, and several semiconductor analysts now argue that pace looks conservative given how quickly AI‑related orders are scaling.

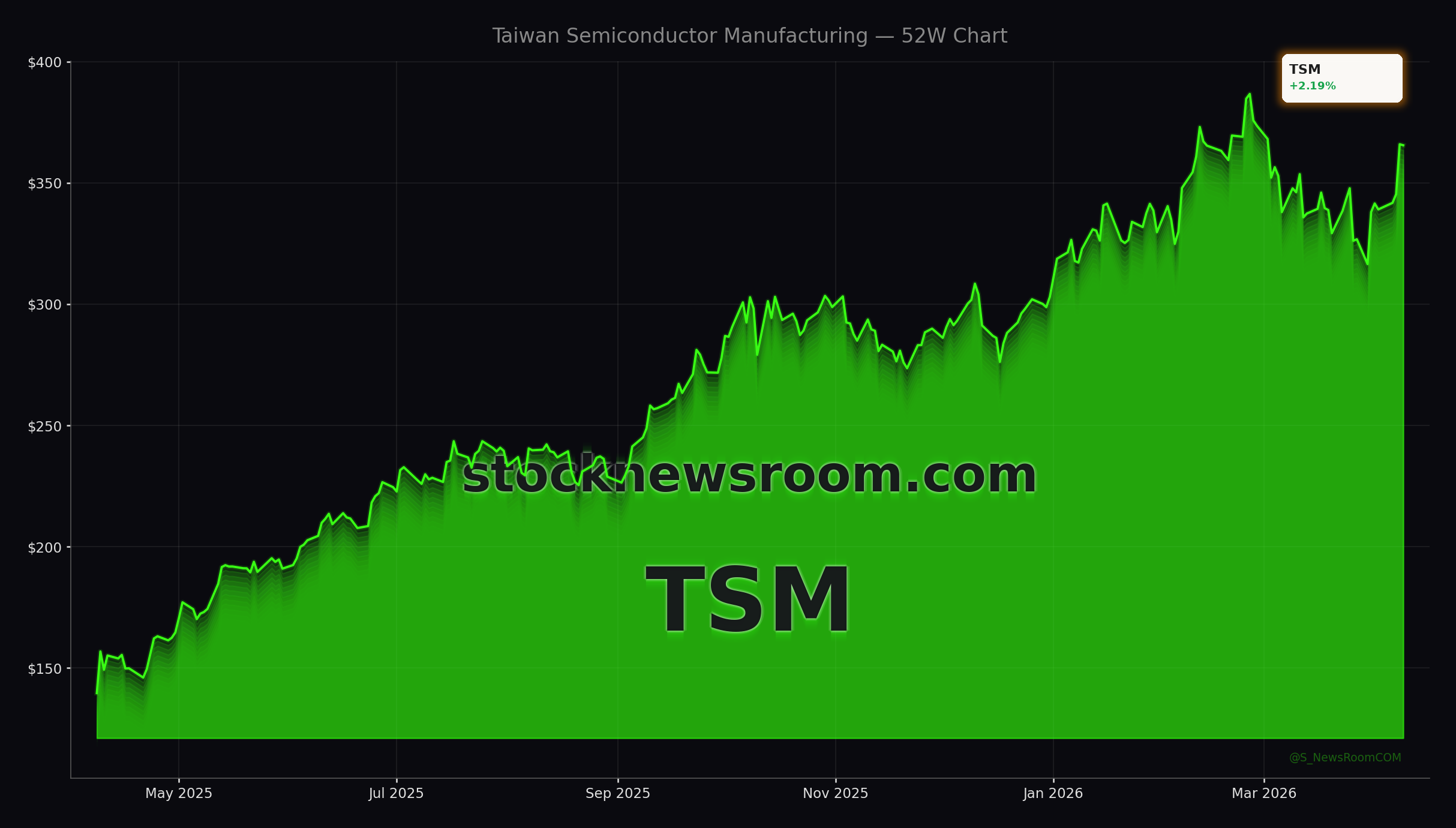

In New York trading, Taiwan Semiconductor (TSM) closed Thursday at $366.40 and recently changed hands around $365.49, down 0.11%, while pre‑market quotes point to a move higher toward $373.51, up a little over 2%. The stock has surged more than 100% over the past 12 months, turning TSMC into the most valuable company in Asia and a top‑tier heavyweight on the NYSE by market cap.

What do TSMC Earnings signal for the AI supply chain?

The latest TSMC Earnings are effectively a barometer for the entire AI hardware ecosystem. The foundry manufactures many of the world’s most advanced chips for customers including NVIDIA, Apple, Advanced Micro Devices and Broadcom. With AI infrastructure spending running into the hundreds of billions of dollars, TSMC’s order book has become a direct proxy for hyperscaler capex and the pace of AI adoption in data centers.

Analysts note that roughly a fifth of TSMC’s wafer revenue now comes from AI accelerators and related high‑performance compute products. That mix should continue to rise as clients roll out next‑generation GPUs and custom silicon for both AI training and inference. Price hikes on leading‑edge nodes have also been a quiet but important driver: several research houses estimate that increases on TSMC’s most advanced processes were a key factor in the Q1 revenue beat and in its expanding margin profile.

Competitive dynamics are also in focus. Intel is pushing its “five‑nodes‑in‑four‑years” roadmap and targeting process leadership with Intel 18A in 2025 to close the gap with TSMC, while Samsung is investing heavily in foundry capacity of its own. For now, however, Taiwan’s champion still produces the vast majority of sub‑5‑nanometer logic chips globally, and recent earnings momentum suggests its technology lead remains intact.

How is Wall Street reacting to TSMC and peers?

TSMC’s run has been fueled by strong institutional demand. Several U.S. investment firms have recently disclosed large positions or increases, even as some others lock in partial profits after the rally. Citigroup has reiterated its bullish stance on the stock, raising its price target for the Taiwan‑listed shares to NT$2,800 and boosting profit estimates through 2028 on the back of AI‑driven growth. Other firms, including Bernstein SocGen Group, have also lifted their targets, arguing that both AI and non‑AI segments remain structurally strong.

Not all voices are unreservedly positive. Some valuation models flag TSMC as potentially overvalued after its 136% one‑year surge, especially when factoring in geopolitical risk around Taiwan and the elevated energy and capex requirements for advanced fabs. Yet even cautious analysts concede that TSMC’s earnings power is rising quickly as utilization improves and pricing on advanced nodes firms up.

For U.S. investors, the read‑through extends far beyond one stock. Strong TSMC Earnings tend to support sentiment for high‑beta chip names across the NASDAQ and S&P 500, particularly those directly tied to AI compute and memory. They also matter for downstream beneficiaries like Tesla, which relies on advanced chips for autonomous driving and infotainment, and cloud software names that depend on continued AI infrastructure build‑out.

What risks remain for TSMC and global chip stocks?

Despite the upbeat TSMC Earnings backdrop, several risks are front and center for Wall Street. Rising geopolitical tensions across the Taiwan Strait have put supply‑chain resilience in the spotlight, with some customers exploring greater geographic diversification even as they continue to lean on TSMC’s technology. Energy security and cost inflation are additional watch points, given the immense power needs of cutting‑edge fabs and AI data centers.

Competition is another theme to monitor. More companies are designing their own chips, from hyperscalers like Google to CPU designers like Arm, which is now using TSMC to fabricate its first in‑house AGI CPU. AI startup Anthropic and a long tail of specialized chip firms are also looking to bring inference‑focused processors to market. While much of this new silicon will still be manufactured at TSMC, it underscores how rapidly the landscape is evolving.

Investors will be listening closely on April 16 for commentary on smartphone and PC demand, potential inventory corrections triggered by higher memory prices, and any update to long‑term margin targets. With the stock hovering below, but not far from, recent 52‑week highs, guidance will be crucial in determining whether the latest TSMC Earnings can justify further multiple expansion.

Related Coverage

For a deeper dive into how the AI narrative has powered the recent share-price surge, see “Taiwan Semiconductor AI Expansion Fuels +6.1% Rally”, which explores whether TSMC’s expansion plans fully justify its stunning rally or if markets are pricing in too much future growth today. For a contrasting look at how legal and governance risks can hit high‑multiple tech names, read “Snowflake Lawsuit -11.8% Crash as Insider Deals Face Scrutiny”, highlighting why even AI‑exposed cloud favorites can face sharp drawdowns when investor confidence is shaken.

In sum, the latest TSMC Earnings confirm that the AI hardware boom is still in full swing and that the company remains the critical bottleneck for cutting‑edge chips worldwide. For investors on Wall Street, that means TSMC’s quarterly reports will continue to set the tone for the entire semiconductor complex and for mega‑cap tech sentiment. The next few quarters will show whether record demand, margin expansion and massive capex can keep powering the stock’s ascent despite rising competition and geopolitical uncertainty.