Is the latest Uber Forecast of massive upside driven by real cash flows or just robotaxi hype on Wall Street?

How does the Uber Forecast compare to Wall Street targets?

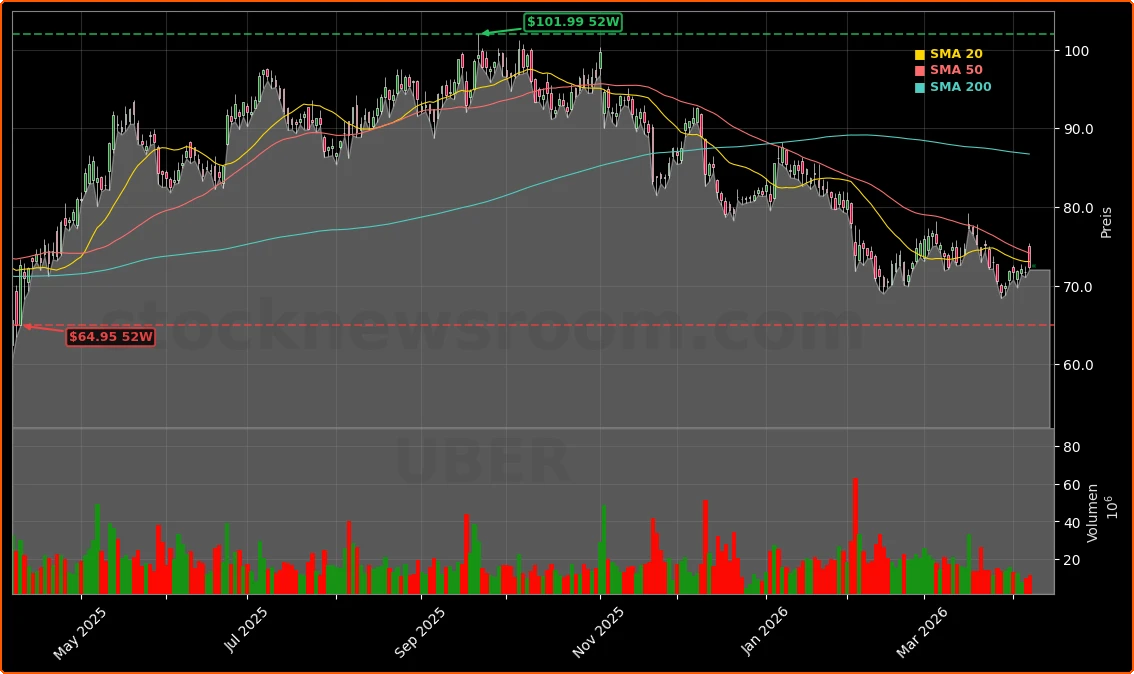

Uber Technologies, Inc. (Uber) currently changes hands at $72.38, modestly higher on the day but still down double digits year to date after a sharp selloff from late 2025 highs. Quant-driven models see a 12‑month target around $123.73, implying roughly 71% upside from current levels. This Uber Forecast is supported by 47 buy or strong-buy ratings against just one sell, signaling broad institutional confidence that the stock’s pullback is more sentiment-driven than fundamental.

Traditional research desks are slightly more conservative but still positive. Wells Fargo recently trimmed its price target from $100 to $95 while keeping an “Overweight” rating, citing near-term weather headwinds and heavy investment but leaving its longer-term thesis intact. Bernstein SocGen Group reiterated its “Outperform” rating with a $110 target after Uber announced a multi-year autonomous vehicle partnership, reinforcing the view that robotaxis could unlock substantial value from 2027 onward.

With the shares trading at about 29% below the 52-week high and at roughly 15x trailing earnings, valuation screens as undemanding relative to expected revenue growth around the high teens and a rapidly scaling cash-flow profile. For many US growth investors, the current Uber Forecast effectively frames the stock as a high-beta reopening and AI-adjacent play at a discount.

Are robotaxis the key to the Uber Forecast?

The most aggressive Uber Forecast scenarios hinge on autonomous vehicles reshaping the cost structure of ride-hailing. Uber’s $1.25 billion partnership with Rivian to deploy 50,000 purpose-built robotaxis by the end of 2026 and expand into 15 cities is the centerpiece of that thesis. CEO Dara Khosrowshahi has called AVs a “multitrillion-dollar opportunity” for the platform, positioning Uber as the distribution layer that connects fleets to riders rather than owning all the hardware risk itself.

On top of Rivian, Uber signed a separate multi-year agreement with Zoox that will roll out custom autonomous vehicles starting in Las Vegas in summer 2026 and then Los Angeles by mid‑2027. These deals give the company multiple shots on goal, similar to how NVIDIA supplies chips across many AI players instead of betting on just one application. If robotaxis achieve scale, investors expect structurally higher margins as driver costs shrink, with some long-term models flagging a five-year bull case above $300 per share.

However, the Uber Forecast for AV adoption is not without risk. Commercialization timelines, regulatory approvals and revenue-sharing economics with partners could all slip, compressing the expected margin uplift. That uncertainty explains why price targets vary widely even among bullish analysts, from the mid‑$90s at Wells Fargo to more than $120 in some quantitative projections.

How strong are Uber’s core cash flows today?

While autonomous vehicles dominate the long-run Uber Forecast narrative, the current bull case rests firmly on execution in the existing rides, delivery and freight segments. Uber delivered $52.01 billion in full-year 2025 revenue, up 18.3% year over year, and $14.366 billion in Q4 revenue, up just over 20%. More importantly for equity holders, Q4 2025 free cash flow hit a record $2.80 billion, up 65% year over year, helping push full-year free cash flow to $9.76 billion.

Delivery continues to be a quiet engine of improvement. Delivery segment Adjusted EBITDA grew 40% year over year in Q4 2025, aided by a rising advertising business where management recently lifted its long-term penetration ceiling beyond the previous 2% estimate of gross bookings. That higher-margin ad revenue resembles what Apple and other platform companies have done by monetizing intent and traffic rather than just transactions.

Not everything is moving straight up. Long-term debt climbed from $8.34 billion to $10.52 billion year over year as Uber funded AV infrastructure and leaned into a $20 billion share repurchase authorization. Insurance reserves also rose, and the Freight segment showed no growth in the latest quarter. Bears argue that leverage and execution risk could pressure the multiple if growth slows or regulatory costs rise, though cash generation currently provides a sizable buffer.

What should US investors watch next in the Uber Forecast?

For US portfolios benchmarked to the S&P 500 and Nasdaq, Uber now screens as a high-growth, cash-generative tech platform trading below its peak multiples, somewhat akin to where Tesla sat before its major re‑rating around autonomous driving. The key short-term catalyst for the Uber Forecast is whether Q1 2026 gross bookings land within the guided $52 billion to $53.5 billion range and if management reiterates its AV rollout timetable.

Regulation is another swing factor. Any shift in worker-classification rules that raises driver costs, or AV partnership terms that push more economics to the hardware providers, would compress the take rate and undercut the robotaxi margin story. Conversely, smooth deployments in Las Vegas and Los Angeles, combined with further buyback execution, could close part of the gap toward price targets in the $110–$125 band over the next 12–18 months. For growth-focused US investors, the Uber Forecast effectively comes down to whether they believe the company can maintain 20% revenue growth while converting more of that into durable free cash flow.

Related Coverage

For a deeper dive into how the Rivian partnership could reshape the economics of autonomy for shareholders, investors can read our detailed look at Uber’s $1.25 billion robotaxi deal with Rivian and its potential to become a long-term margin machine. Those tracking AI-exposed names alongside Uber may also want to examine valuation risk in software, as discussed in our analysis of Palantir’s AI strategy and the recent 6.2% share price drop testing the bull case, which offers a useful contrast in how the market prices different kinds of tech optionality.

AVs will unlock a multitrillion-dollar opportunity for Uber.— Dara Khosrowshahi, CEO of Uber Technologies, Inc.

Overall, the Uber Forecast from Wall Street and quantitative models points to meaningful upside, driven by record free cash flow, expanding delivery margins and real progress on robotaxis. For American investors, the stock now represents a leveraged play on both global mobility demand and the commercialization of autonomy. The next few quarters of bookings data and AV milestones will determine whether Uber starts to close the gap toward bullish price targets or remains one of the more controversial growth stories on the NYSE.