Can a surprise Unity Software Earnings upgrade and bold AI pivot really flip Wall Street’s bearish script on this battered tech name?

How did Unity Software Earnings surprise Wall Street?

Unity Software Inc. (U) delivered a rare dose of good news for investors late Thursday, issuing preliminary first‑quarter numbers that comfortably beat its own prior guidance and consensus estimates. The company now expects Q1 2026 revenue between $505 million and $508 million, well above its earlier range of $480 million to $490 million and ahead of the roughly $489 million analysts were modeling.

Profitability is improving even faster. Adjusted EBITDA is projected at $130 million to $135 million, up from a previous forecast that hovered around $100 million and well above the Street’s $109 million expectation. That implies a meaningful margin uplift for a business long criticized for weak profitability despite strong top‑line growth.

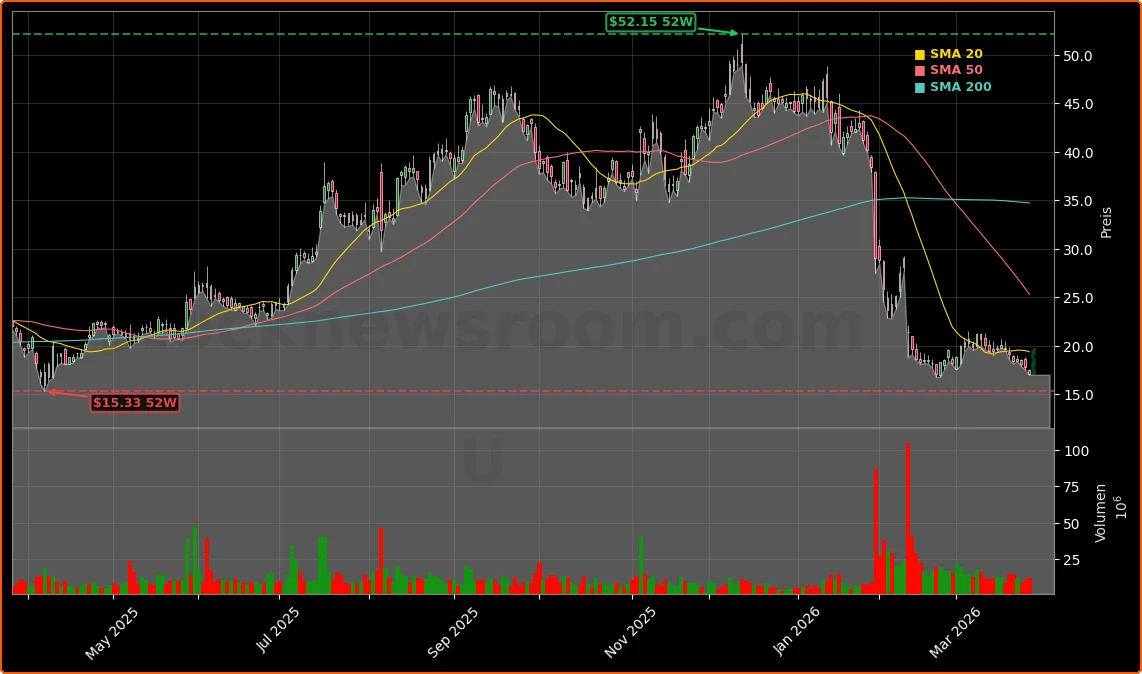

The upbeat Unity Software Earnings update immediately changed the tone around the stock. Shares had closed regular Thursday trading at $17.13 on the NYSE, down sharply from recent highs and reflecting deep skepticism about the company’s strategy. In after‑hours trading, the stock ripped higher by more than 14% at one point, with pre‑market quotes on Friday pointing to levels around $19.64, though still far below its 52‑week peak.

Why is Unity Software refocusing its business now?

Beyond the headline Unity Software Earnings beat, management paired the guidance hike with a significant strategic reset. The company plans to shut down the ironSource Ads Network by April 30, 2026, and pursue a sale of its Supersonic mobile game publishing unit. Advisors have already been engaged to run a divestiture process for Supersonic.

These units came into Unity via the ironSource merger, but investors have increasingly questioned their strategic fit and margin profile. Exiting these non‑core ad businesses is designed to simplify the portfolio and steer capital and talent toward higher‑growth, higher‑margin areas like its AI‑enhanced advertising stack and its core Create engine business.

A central driver behind the stronger Unity Software Earnings outlook is Unity Vector, the company’s AI‑powered user acquisition and ad optimization platform. Unity highlighted Vector’s outperformance as a key factor in both revenue acceleration and the upgraded EBITDA guidance. Management now expects what it calls “Strategic Grow” revenue to jump roughly the high‑40% range year over year, underlining how quickly AI‑driven ad tools are scaling inside the business.

This pivot is also a direct response to intensifying competition in game development and tooling. Alphabet’s Google recently showcased Gemini‑powered tools for game coding, stoking worries that major platforms could commoditize parts of Unity’s offering. By doubling down on differentiated AI infrastructure and its massive developer ecosystem, Unity aims to keep creators locked into its engine and monetization stack.

How do Unity Software Earnings stack up to peers?

From a Wall Street standpoint, the updated Unity Software Earnings narrative comes after a brutal de‑rating that saw the stock lose roughly two‑thirds of its value from its recent 52‑week high. That sell‑off reflected concerns over slowing growth, execution missteps, and the risk that third‑party AI tools could disintermediate parts of the business, especially on mobile.

Even after the post‑guidance bounce, Unity’s valuation screens more modest than many software peers on metrics like price‑to‑sales, price‑to‑earnings growth, and price‑to‑book. That has prompted a handful of more constructive calls on the name. Citizens, for example, recently reiterated a “Market Outperform” rating and a $37 price target, arguing that the sell‑off has been excessive and that Unity’s AI growth potential is underappreciated.

The upgrade in Unity Software Earnings guidance also puts the company back into the broader AI conversation alongside larger platform players. While Unity is nowhere near the scale of NVIDIA in AI infrastructure or Apple in consumer devices, its engine remains a critical piece of the real‑time 3D and gaming ecosystem. The company’s success or failure in monetizing AI across games, digital twins, and immersive experiences will shape how it competes with Epic Games’ Unreal Engine and the growing universe of AI‑native tools.

For US investors comparing opportunities across the NASDAQ and S&P 500, Unity sits squarely in the high‑beta, turnaround‑tech bucket. It is not yet the kind of cash‑rich compounder that mega‑caps like Tesla aspire to be; instead, it represents a potential rebound story where execution on the new strategy will drive whether the recent Unity Software Earnings momentum is a one‑off or the start of a multi‑quarter re‑rating.

What’s next for Unity Software and its stock?

Technically, the stock remains in repair mode. The sharp rally off the $17–$18 area has so far helped avert a breakdown below recent lows that would have signaled fresh downside. However, chart watchers note that a more durable bullish signal would only emerge if the shares can reclaim and hold above the 50‑day moving average, currently in the mid‑$20s.

Short interest around 8% of the free float adds another layer of volatility. A few more positive Unity Software Earnings reports or additional disclosure showing sustained AI‑driven growth could trigger a short squeeze, amplifying any move higher. Conversely, any hint that Vector’s momentum is slowing or that the exit from ironSource and Supersonic is more disruptive than planned could quickly revive the bear case.

Fundamentally, the path forward hinges on three questions: Can Unity maintain double‑digit growth as it sheds non‑core revenue? Will AI‑enabled products like Vector and its in‑engine AI tools translate into durable, high‑margin streams? And can management restore enough confidence to expand enterprise deals beyond gaming into automotive, industrial, and other real‑time 3D verticals?

For now, the upgraded Unity Software Earnings guidance, margin improvement, and portfolio simplification mark a clear positive inflection. The next full quarterly release and management commentary will be crucial in proving that this is not just a tactical bounce, but the beginning of a more disciplined, AI‑led growth chapter for Unity Software Inc..