Is Volkswagen’s dominance in the shrinking convertible niche a hidden strength or a warning sign for long‑term investors?

Volkswagen AG: Stock under pressure while strategy shifts

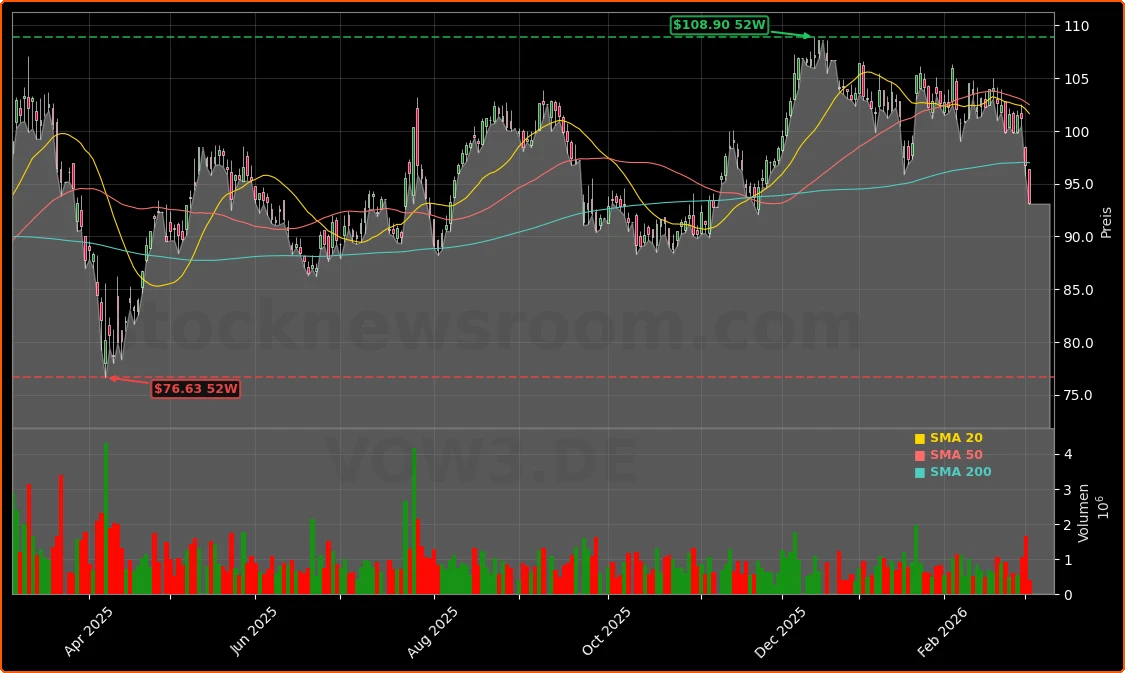

Volkswagen AG’s VOW3 shares recently changed hands at about $93.16, down roughly 3.7% from the prior close of $96.74. That decline comes against a mixed backdrop for global autos: U.S.-listed peers such as Tesla and traditional OEMs on the NYSE have been volatile as investors reassess growth expectations, EV adoption curves and capital intensity. Even without precise VW earnings figures in front of us, the price move indicates investor caution toward cyclical, export-heavy European manufacturers in a world of high energy costs, fragile trade routes and geopolitical tension.

For U.S. and international portfolios, Volkswagen typically screens as a value play: a large, diversified automaker with substantial exposure to Europe and China, trading at a discounted multiple to many S&P 500 auto and tech-adjacent names. The recent pullback raises the question of whether the risk/reward is improving – and that’s where understanding VW’s product mix, including niche segments such as the Volkswagen convertible market, becomes important. Dominance in a shrinking category will not drive group earnings, but it can shape brand perception and reveal how management handles legacy products as market conditions change.

Macro headwinds complicate the picture. Elevated European energy prices hit energy-intensive industries disproportionately, and export-oriented German manufacturers face added margin pressure from supply-chain uncertainty and potential trade friction. These factors matter for VW’s cost base and pricing strategy in Europe, while demand in China and North America determines how much of that pressure can be offset with volume and mix.

Volkswagen convertible market: Dominance in a shrinking niche

The Volkswagen convertible market leadership story is rooted in a stark structural decline. In Germany, only 33,924 new convertibles were registered in 2025, around 17% fewer than in 2024 – and 2024 was already near a multi-year low. That means just about one in every 84 new cars sold in the country is now a convertible, a dramatic shift from 2009 when over 100,000 convertibles were registered and the segment was more than three times as large.

This collapse reflects both demand and supply. Consumer preferences have shifted toward SUVs and crossovers that promise a blend of perceived freedom, higher seating position and practicality. Automakers, under pressure to simplify lineups, cut costs and fund electrification, have pruned low-volume body styles including convertibles. Many brands now offer no drop-top models at all; others maintain one or two halo cars.

Within that context, Volkswagen has emerged as the clear number one player in the German cabrio segment. The T-Roc Cabriolet was the best-selling convertible in 2025, effectively making VW the market leader on a brand level almost single-handedly. In other words, the Volkswagen convertible market is now less a broad competitive battlefield and more a narrow stronghold in which VW faces fewer rivals but also less absolute demand.

For equity investors, this is a classic case of relative versus absolute dynamics. In relative terms, VW’s share is impressive: it owns a disproportionately large piece of what remains of the market. In absolute terms, however, the segment is too small to materially drive consolidated revenue or operating profit. The strategic question becomes whether maintaining and modestly refreshing models like the T-Roc Cabriolet delivers an adequate return on capital or merely siphons engineering and marketing resources away from growth areas.

BMW and other competitors: What VW’s cabrio dominance really tells us

On the competitive side, BMW ranks second in German convertible sales, while premium peers such as Mercedes-Benz also maintain a presence in the segment with higher-priced models. From a U.S. investor’s lens, this echoes a broader split in the global auto industry: premium brands focus on high-margin, often lower-volume emotional products, while mass brands like Volkswagen blend emotional halo cars with scale-focused platforms.

In the Volkswagen convertible market, VW effectively straddles the line. The T-Roc Cabriolet is not a stripped-down cheap convertible; it is based on a crossover platform that taps into the SUV trend while offering open-top driving. That positioning allows VW to monetize the halo effect – reinforcing lifestyle branding and pricing power – without committing to an entirely standalone low-volume platform. By contrast, BMW’s traditional emphasis has been on rear-wheel-drive coupes and convertibles that serve performance-oriented buyers at higher price points.

The fact that Volkswagen rather than a premium specialist now leads convertible registrations underscores how the segment’s center of gravity has moved from aspirational sports cars to lifestyle SUVs with removable roofs. It also hints that VW’s modular platform strategy is working: by spinning variants like cabriolets off mainstream architectures, the company can flexibly scale production up or down as the niche expands or contracts without crippling unit economics.

For U.S. investors familiar with how Ford or General Motors have cut sedans and coupes to prioritize trucks and SUVs, the European convertible story will feel familiar. Where Detroit has been aggressive in exiting unprofitable segments, Volkswagen is taking a more nuanced approach – allowing certain emotional products to survive if they can be economically built on shared platforms. Whether that discipline holds over time is an important monitoring point for shareholders.

Volkswagen AG product portfolio: Managing decline and growth simultaneously

The Volkswagen convertible market is only one piece of a complex portfolio puzzle. VW must simultaneously manage multiple transitions: from ICE to EV, from sedans and wagons to SUVs and crossovers, and from hardware-centric business models to software-defined vehicles and digital services. Each of these shifts requires heavy capital expenditure and R&D, raising the bar for any legacy segment to justify continued investment.

Convertibles sit squarely in the legacy bucket. The collapse in registrations over the past decade indicates that the addressable market is structurally smaller, not merely suffering a cyclical dip. At the same time, discontinuing all convertibles carries reputational risk, especially for a brand with deep roots in open-top motoring from the classic Beetle Cabrio to the Golf Cabriolet. VW’s current approach – limited offerings like the T-Roc Cabriolet that leverage mainstream platforms – appears to be a compromise between heritage and hard-nosed capital efficiency.

From a valuation standpoint, investors should not assign any significant growth premium to the Volkswagen convertible market. Instead, the key is whether VW can keep it margin-neutral or margin-accretive while freeing up engineering capacity for EVs, battery tech and software. If the company can maintain a lean, profitable convertible line without incremental platform complexity, the segment can remain a small positive contributor and a brand asset rather than a drag.

In comparison, U.S.-listed automakers like Tesla have no legacy open-top volumes to defend and can allocate capital purely based on forward-looking EV economics. That contrast partly explains why equity markets tend to assign much richer multiples to pure-play EV and tech-adjacent names than to diversified automakers wrestling with legacy assets. For VW, demonstrating ruthless portfolio discipline – including around convertibles – is one way to narrow that multiple gap over time.

Volkswagen AG valuation context for Wall Street portfolios

For international investors benchmarking against the S&P 500 and NASDAQ, Volkswagen is predominantly a value and income candidate, not a high-growth story. The shares have been under pressure, and while we do not have VW’s exact price/earnings ratio or enterprise-value-to-EBIT multiples in this context, European auto majors typically trade at single-digit P/Es, reflecting cyclical risk and capital intensity. Leadership in the Volkswagen convertible market does little to change that high-level valuation narrative, but it can influence perceptions of brand strength and pricing power.

Analyst coverage from large banks such as Citigroup, JPMorgan and UBS usually focuses far more on VW’s EV rollout, software strategy, exposure to China and cost-cutting programs than on niche body styles. Ratings from houses like Deutsche Bank or RBC Capital Markets often come with cautiously optimistic language: acknowledging VW’s strong industrial base and scale advantages while flagging execution risk in electrification and software. Whether those firms label the stock as “Buy”, “Hold” or “Underperform” tends to hinge on macro views and confidence in management’s ability to deliver on mid-term margin targets.

For U.S. investors constructing diversified portfolios, the main question is whether VOW3 offers enough upside versus risks to justify an allocation relative to U.S.-listed peers. Currency exposure to the euro, European macro uncertainty and regulatory risk in the EU and China all factor in. The convertible niche becomes relevant here primarily as a signal: VW is willing to let structurally shrinking segments decline gracefully while concentrating incremental capital on higher-return areas. If that interpretation holds, it supports the thesis that the company is gradually becoming more shareholder-focused.

Relative to growth stocks in the NASDAQ, VW will likely remain a lower-multiple, higher-yield position. But within the global auto basket – including Ford, General Motors and Japanese OEMs – disciplined management of legacy portfolios, including the Volkswagen convertible market, can help VW earn a valuation at the upper end of the traditional-automaker range.

Risk factors: Cyclicality, geopolitics and structural demand shifts

Owning VOW3 is not without significant risk. The first and most obvious is cyclical demand. Autos remain a big-ticket, credit-sensitive purchase, and any recession in Europe or slowing growth in China would weigh on VW’s volumes. A niche like convertibles is particularly sensitive: when consumer confidence falls, discretionary purchases like cabriolets are often deferred first. This adds volatility to a segment that is already structurally shrinking.

Geopolitics is another critical risk. Export-oriented German manufacturers depend on stable trade relationships and secure transport routes. Disruptions in key shipping lanes, trade disputes or sanctions can raise logistics costs, delay deliveries and pressure margins. For VW, whose supply chain and sales network span Europe, China, and other major markets, such shocks can ripple quickly through earnings. Higher European energy prices also increase production costs, especially for plants in Germany, challenging VW to maintain competitive pricing globally.

Structural demand shifts compound these challenges. The secular move toward SUVs and crossovers has already hollowed out traditional segments like sedans, wagons and now convertibles. In the Volkswagen convertible market, the fact that the T-Roc Cabriolet – a crossover-derived model – tops the sales charts reflects both adaptation and limitation: VW has successfully migrated the convertible concept onto a modern platform, yet total demand continues to erode. If consumer tastes continue to drift toward enclosed, tech-laden vehicles with advanced driver assistance and infotainment, true open-top models may retreat further into niche territory.

Regulatory pressure, especially on emissions, adds another layer. Convertibles based on ICE platforms must comply with increasingly stringent CO2 and pollutant standards in Europe. If compliance costs rise faster than consumers’ willingness to pay, profitability will be squeezed. VW will need to decide over the coming product cycles whether to electrify any future convertibles or gradually let them disappear from the lineup in favor of EV crossovers and hatchbacks.

Strategic implications and outlook for the Volkswagen convertible market

Looking ahead, the Volkswagen convertible market is unlikely to return to its former size. Instead, investors should think of it as a managed sunset business embedded within a broader transformation story. VW’s near-monopoly-like position in Germany gives it some pricing power and brand visibility, but not meaningful growth. The key will be how the company uses the segment to support overall brand equity while redeploying capital to EVs, software and mobility services.

Several strategic paths are possible. One is a continued focus on crossover-based convertibles like the T-Roc Cabriolet, refreshed periodically but not radically reengineered, keeping development costs low. Another is the introduction over time of an electric convertible built on a scalable EV platform, serving as a halo product that signals VW’s ability to blend sustainability with driving emotion. A third path, if economics deteriorate, would be a gradual exit from convertibles altogether, relying instead on design and technology to project aspirational appeal.

For now, management appears to be following the first path: sustaining the existing Volkswagen convertible market presence with minimal incremental complexity. That approach seems prudent given the need to preserve resources for higher-impact initiatives. Investors should monitor product announcements, capex plans and commentary on model portfolio decisions during earnings calls to gauge whether VW continues to apply strict return-on-investment criteria to niche segments.

Ultimately, the way Volkswagen handles the convertible niche will serve as a microcosm of its broader strategy. If the company can demonstrate that it will not chase volume for volume’s sake, even in historically beloved segments, but instead prioritize profitability and capital efficiency, it strengthens the case for multiple expansion from today’s discounted levels.

Conclusion

Conclusion: For global investors assessing VOW3, the Volkswagen convertible market is not a primary earnings driver but a revealing test case. VW’s dominance in a shrinking niche highlights both its brand strength and its ability to leverage modular platforms. What matters more for valuation is how decisively the company manages this decline while funding its EV and software ambitions. If Volkswagen can keep convertibles as a lean, profitable, brand-enhancing sideline rather than a resource drain, the segment will quietly support, rather than hinder, the long-term investment thesis.

Further Reading

- Convertible car registrations in Germany hit multi-year low in 2025 (dpa-AFX)

- German auto industry faces pressure from high energy costs and export uncertainty (Reuters)

- Global automakers, EV transition and investor valuation frameworks (Bloomberg)

- Volkswagen AG bei Yahoo Finance (Yahoo Finance)