Is the Volkswagen transformation facing a comeback despite margin pressure and weakness in China, or is it headed for a prolonged dry spell?

Volkswagen AG: How Hard is Margin Pressure Hitting?

Those looking at the figures for Volkswagen AG today see a heavyweight in distress. The operating result has significantly collapsed, with a margin of around 2.3% — a level too low for a global industrial corporation to invest comfortably in the long term. The main causes are overcapacity in the global automotive market and increasingly fierce competition, forcing even established players to cut prices. The weakness in China is particularly severe, where Volkswagen achieved about 42% of its deliveries in its peak year of 2020, but is projected to drop to around 30% by 2025.

Additionally, there was a weak start to the year in Europe: In January, the group’s car registrations fell by 3.7% year-on-year, with the core brand Volkswagen losing even 10.6%, resulting in 85,841 new registrations. High cost structures, discount wars, and significant investment needs in electrification and digitalization further pressure profitability. All of this makes it clear why the Volkswagen transformation is not a moderate adjustment but a true test of endurance.

Volkswagen AG: Where is the Strong Cash Flow Coming From?

On the other hand, there is a financial situation that offers solid leeway. In the core automotive business, more money is flowing in than going out again. After investments, around €6 billion in net cash flow remains, and even after deducting all debts, there are more than €34 billion in liquidity reserves in the automotive sector. This means Volkswagen is not operating in crisis mode but is navigating the structural change with a well-filled financial “reserve tank.”

The discrepancy between the low margin and high cash flow is explained by tight management: inventory levels have been reduced, supply chains optimized, investments stretched over time, and cost programs intensified. These measures improve cash flow in the short term without immediately impacting the profit and loss statement. Analysts like RBC Capital Markets emphasize that net cash flow is above market expectations despite the weaker development in China. For the Volkswagen transformation, this means: the resources to pre-finance software, platforms, and new models are available.

Volkswagen Transformation: Is the Shift in Software Enough?

The biggest bottleneck is no longer in the metal but in software. The once-anticipated Trinity project — a highly digital electric vehicle — has been postponed due to excessive complexity. The same applies to the SSP platform, which was supposed to provide a unified technical foundation for future electric vehicles from compact cars to luxury models. Both initiatives are closely tied to the software unit CARIAD, which was supposed to deliver a unified operating system for the group but has been progressing too slowly.

To gain momentum here, Volkswagen is relying on external support: the partnership with US electric vehicle manufacturer Rivian aims to bring modern software architectures, agile development methods, and a different engineering culture into the company. Citigroup analysts see such collaborations as an opportunity to reduce software risks but point out that implementation must be consistent and swift for the Volkswagen transformation to result in marketable digital products.

Volkswagen AG: How Stable is the Core Business in Europe?

Despite all the problems, Volkswagen remains Europe’s dominant car manufacturer with around 27% market share — a strategic shield in times of upheaval. Within the group, the brands are reorganizing: Škoda is seen as a reliable profit generator, Cupra as an emotional growth driver, while the core brand Volkswagen is under particular pressure as it bears both volume and cost burdens. New models are expected to stabilize demand here, but restructuring costs will weigh on short-term results.

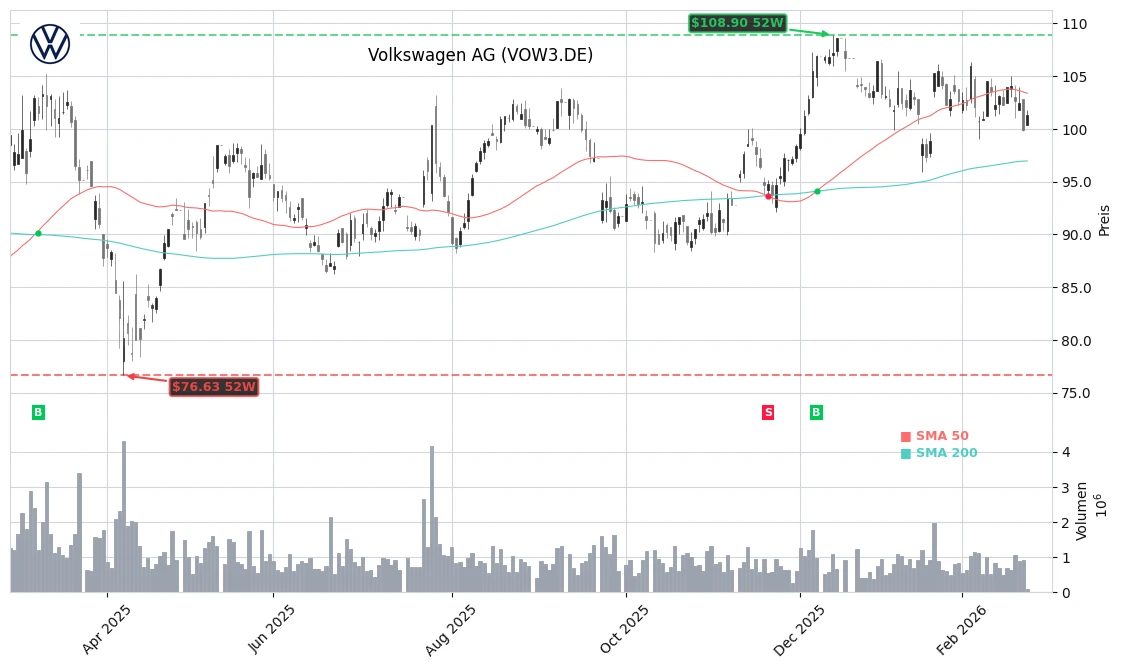

The situation in the premium segment is differentiated. Audi is in the midst of restructuring, while Porsche feels that the adoption of electric mobility in the luxury segment is slower than expected. Overall, however, the strong position in Europe gives the group time to gradually implement software projects, platform changes, and electrification. Whether the current stock price increase to $101.30 marks the beginning of a sustainable revaluation depends crucially on whether the Volkswagen transformation translates from financial to earnings levels.

Volkswagen is currently earning weakly but managing its finances disciplinedly — this combination could make the difference in the transformation.

— Editor in Chief

Bottom Line

Volkswagen stands between weak margins and strong billion-dollar cash flow, but has enough financial leeway to advance the challenging Volkswagen transformation. For investors, this presents a classic risk-reward profile: operational uncertainty meets a solid balance sheet and market position. The key will be whether software partnerships, cost programs, and new models can take effect quickly enough — if successful, the Volkswagen transformation could soon be reflected in the stock price.

Related Sources

- Volkswagen Group Annual Report (Volkswagen AG)

- Analyst Commentary on Volkswagen from RBC Capital Markets (RBC Capital Markets)

- European Automotive Market: Registration Statistics (ACEA)

- Volkswagen AG on Yahoo Finance (Yahoo Finance)