Is the Walmart Strategy of AI, e-commerce expansion and rising dividends enough to justify its premium valuation in a slowing economy?

How does Walmart Strategy shape the stock’s profile?

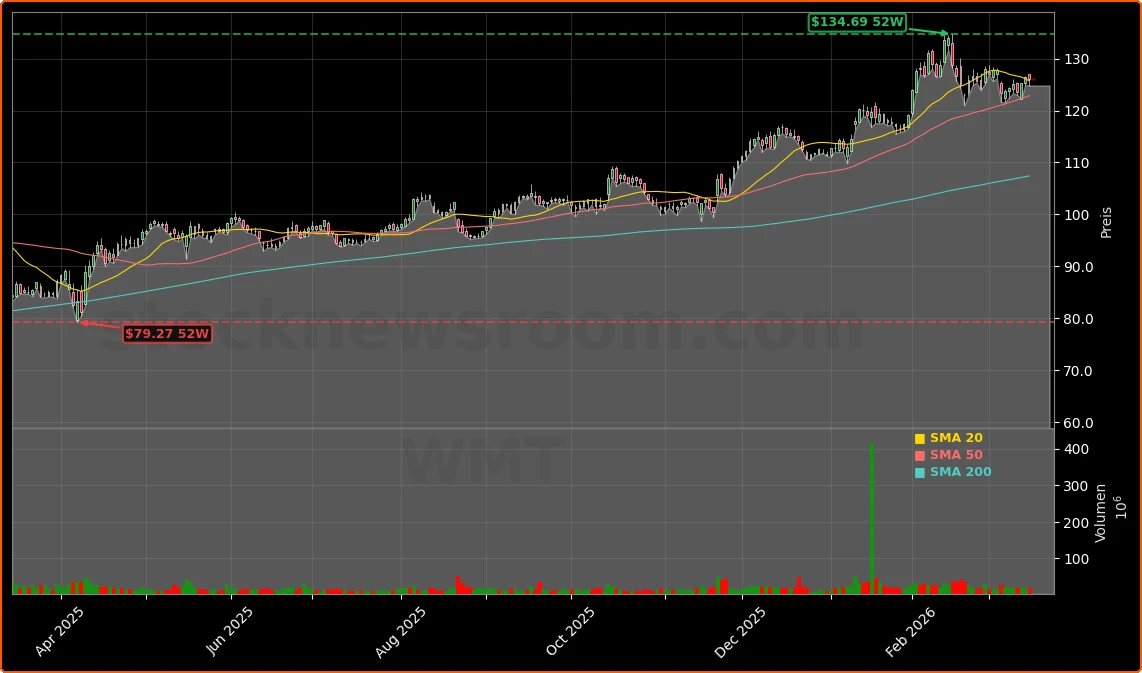

At roughly $126 per share and below its 52-week high, Walmart still commands a premium valuation, trading near 42 times forward earnings. That multiple prices in a lot of optimism, but it reflects a business that has outperformed the S&P 500 over the past decade as it pivoted from pure brick-and-mortar to an omnichannel model. The Walmart Strategy now rests on three pillars: dominant grocery, rapid e-commerce expansion, and disciplined capital returns anchored by a rising dividend.

Historically, the retailer has been one of the strongest recession plays on Wall Street. During the dot-com bust, the Great Recession, and the COVID-19 crash in 2020, the stock posted positive annual gains while the broader market struggled. Roughly 60% of sales now come from grocery, making Walmart Inc. the world’s largest grocer and reinforcing its role as a defensive consumer-staples name similar in profile, though not in format, to Costco and Altria.

Where is Walmart’s digital growth coming from?

A core element of the Walmart Strategy is turning the company into a true e-commerce competitor to Amazon and, indirectly, to ecosystem players like Apple in terms of consumer attention and data. Global e-commerce net sales grew about 24% in the last fiscal year and now represent roughly 23% of total global revenue. That growth is not just from shipping parcels; it includes a rapidly scaling pickup and same-day delivery operation that leverages Walmart’s dense store network.

Recent results highlight particularly strong momentum in international markets, where digital sales climbed at a double-digit pace and total international revenue grew around 7.5% year over year. Subscription offerings such as Walmart+ are pulling in more affluent customers who previously might have favored Apple Pay-driven app ecosystems or warehouse clubs like Costco. The strategic goal is clear: embed Walmart into everyday digital routines and monetize traffic through higher-margin services such as advertising and memberships.

How critical is AI to the Walmart Strategy?

Artificial intelligence is emerging as a second growth engine behind e-commerce. The Walmart Strategy increasingly depends on AI to optimize inventory, personalize online search and recommendations, and improve in-store operations, from dynamic pricing to workforce scheduling. While this does not grab headlines like generative AI at NVIDIA or cloud hyperscalers, the financial impact could be substantial: even modest efficiency gains at Walmart’s scale translate into billions in operating leverage over time.

For investors, AI adoption matters less as a buzzword and more as a margin lever that could justify today’s valuation premium versus peers like Target. As the company rolls out more AI-driven automation in distribution centers and store backrooms, Wall Street will watch gross and operating margin trends closely to see whether technology spend is translating into sustainable profitability gains.

What do dividends, institutions and analysts signal?

Another leg of the Walmart Strategy is steadily enhancing shareholder returns. The company recently approved a 9.2% dividend increase, well above its historical pace, and will go ex-dividend on March 20, with payment set for April 6. The forward dividend yield sits around 0.8%, modest in absolute terms but potentially meaningful if high-single-digit growth continues.

Institutional behavior reinforces the constructive long-term narrative. Asset managers such as DoubleLine ETF Adviser LP have initiated sizable new positions, making Walmart a top holding, while firms like Hilltop Holdings and Elevation Point Wealth Partners sharply boosted their stakes. Consensus on Wall Street remains favorable, with analysts collectively rating the shares a “Moderate Buy” and an average price target in the mid-$130s, implying mid-single-digit upside from current levels. The main bear argument is valuation risk if e-commerce and AI monetization were to slow, but so far the execution behind the Walmart Strategy has kept skeptics at bay.

Walmart’s blend of grocery dominance, digital expansion and AI-driven efficiency makes it one of the few consumer names that can play both offense and defense in modern portfolios.

— stocknewsroom.com analysis

Conclusion

In sum, the Walmart Strategy blends defensive grocery strength with accelerating digital and AI capabilities, offering a rare combination of recession resilience and structural growth. For long-term investors building core positions in the consumer-staples space, the stock remains a credible candidate, even at a premium multiple. The next few quarters of e-commerce, margin and dividend growth will be crucial in determining whether Walmart continues to justify its strategy-driven valuation edge over the broader S&P 500.

Further Reading

- Walmart Inc. (WMT) Stock Price, News, Quote & History (Yahoo Finance)

- 3 Consumer Staples Stocks Built to Create Long-Term Wealth (The Motley Fool)

- Is Walmart a Recession-Proof Stock? (The Motley Fool)

- Walmart’s International Business Shows Strength: Momentum Ahead? (Zacks Investment Research)