Is the sharp drop in Zscaler’s stock a temporary panic or a serious warning sign for the long-term Zscaler Forecast?

Why did BTIG walk away from Zscaler?

Zscaler, Inc. was among the biggest decliners in the S&P 500 and Nasdaq 100 on Thursday after BTIG downgraded the stock from Buy to Neutral and removed its prior $209 price target. The firm cited weakening demand signals from recent field checks and rising competitive pressure, concluding it no longer had conviction in a bullish near-term Zscaler Forecast despite management’s upbeat guidance.

BTIG’s move is notable because it comes on the heels of a strong quarter. Zscaler reported revenue of about $815.8 million, up 25.9% year over year, and annual recurring revenue (ARR) of $3.36 billion, also up 25%. Management lifted full-year revenue guidance to a range of $3.309 billion to $3.322 billion, reinforcing the top-line momentum behind its Zero Trust Exchange platform.

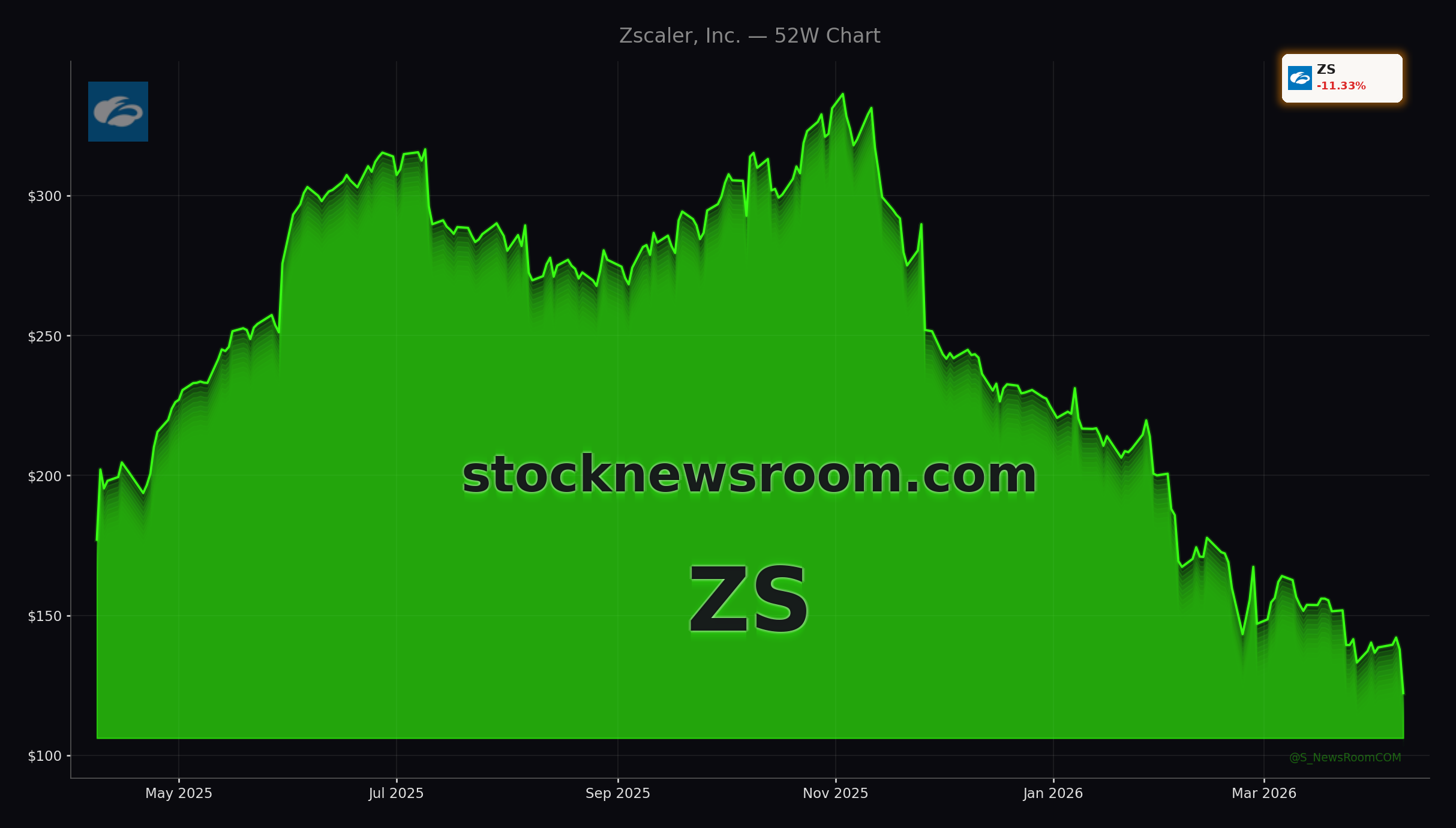

Yet the stock has fallen roughly 44% year to date and now trades near $122, far below its 52‑week high around $337, as investors rotate out of premium-valued software and toward profitable AI leaders like NVIDIA. BTIG argues that multiple compression, ongoing GAAP losses, and integration risk from deals such as Red Canary cloud the Zscaler Forecast for a clean rerating in the near term.

How does the Zscaler Forecast compare with peers?

Part of the pressure on Zscaler stems from tougher competition and an investor base that increasingly demands both growth and profitability. Cybersecurity heavyweights Palo Alto Networks and CrowdStrike are setting a high bar: Palo Alto Networks has delivered non‑GAAP operating margins above 30% for three straight quarters, while CrowdStrike recently reported ARR of $5.25 billion, up 24% year over year, alongside its first positive GAAP net income.

By contrast, Zscaler still posts GAAP losses, and its organic ARR growth of 21% (excluding the Red Canary acquisition) trails the reported 25% figure. That gap between headline and organic numbers is drawing scrutiny as portfolio managers reassess risk across richly valued software names. Valuation remains elevated, with Zscaler trading around 7.4x forward sales and a forward P/E near 30x, even after the selloff.

Despite BTIG’s caution, the broader analyst community remains constructive on the Zscaler Forecast. Recent surveys show the majority of Wall Street firms rating the stock Buy or Strong Buy, with average price targets still well above the current share price. One recent review of brokerage recommendations pegged Zscaler’s average recommendation near a 1.4 on a 1‑5 scale, equivalent to an aggressive Buy stance, even as quantitative systems like the Zacks Rank sit closer to Hold.

What are the growth drivers for Zscaler?

Under the surface, Zscaler continues to expand its platform and addressable market. The company’s core growth pillars are AI Security, Zero Trust Everywhere, and Data Security, supported by more than 160 global data centers and a cloud-native architecture that inspects billions of daily transactions. Management argues that enterprises are still in the early stages of replacing legacy VPN and firewall stacks with cloud-delivered Zero Trust, a foundation that underpins a long-term bullish Zscaler Forecast.

Recently, Zscaler has doubled down on AI agent security, aiming to secure the wave of autonomous agents and copilots being rolled out by large enterprises. That initiative leverages its existing data lake and Zero Trust controls to monitor and govern AI interactions, a niche where rivals like Palo Alto Networks and CrowdStrike are also investing heavily. Early indications suggest this AI push is helping Zscaler land larger, more strategic deals, though investors are waiting to see a clear impact on revenue growth and margins.

At the same time, Zscaler has expanded its Zero Trust ecosystem through partnerships with companies like P0 Security and Versa, integrating with Versa Secure SD‑WAN to tighten secure connectivity for distributed networks. These alliances support the narrative that Zscaler can remain a central security fabric for multicloud and hybrid environments, even as hyperscalers and platform vendors broaden their own offerings.

What does the Zscaler Forecast mean for investors now?

For U.S. investors, the key question is whether the post-downgrade slide marks a buying opportunity or a value trap. Valuation models that focus on discounted cash flow and long-term margin expansion still see upside, with some independent fair-value estimates significantly higher than today’s price. However, relative metrics versus software peers paint a less generous picture, suggesting Zscaler still commands a premium despite decelerating share-price momentum.

Trading-oriented services highlight weak sentiment and a short bias in the near term, recommending strict risk controls for anyone stepping into the stock. Meanwhile, high-yield structured products such as UBS’s 22.11% contingent coupon notes linked to Zscaler underscore just how volatile the name has become; investors in those notes face the risk of substantial losses if the stock remains under pressure.

Market commentators like Jim Cramer have argued that Zscaler “shouldn’t have been hit all that hard” given its fundamentals, but even they suggest trimming exposure on rallies when portfolios are overloaded with similar cybersecurity names such as Tesla-adjacent AI beneficiaries or direct rivals like CrowdStrike and Palo Alto Networks. The consensus: respect the volatility while acknowledging that the long-term Zscaler Forecast still hinges on execution in AI security, sustained double-digit ARR growth, and a credible path toward durable GAAP profitability.

In the end, today’s BTIG downgrade does not dismantle the Zero Trust thesis, but it does reset expectations. For long-term investors, the Zscaler Forecast remains tied to whether the company can convert its strong top-line trajectory and expanding AI footprint into cleaner earnings and cash flow. The next few quarters of billings, margin trends, and competitive wins will show whether this reset becomes a springboard for renewed upside or simply a new normal for a maturing – but still pivotal – cloud security leader.