Is AMD suddenly the market’s clearest AI infrastructure winner as Nvidia’s next big rack system slips further into the future?

Why Is AMD Surging While Nvidia Stalls?

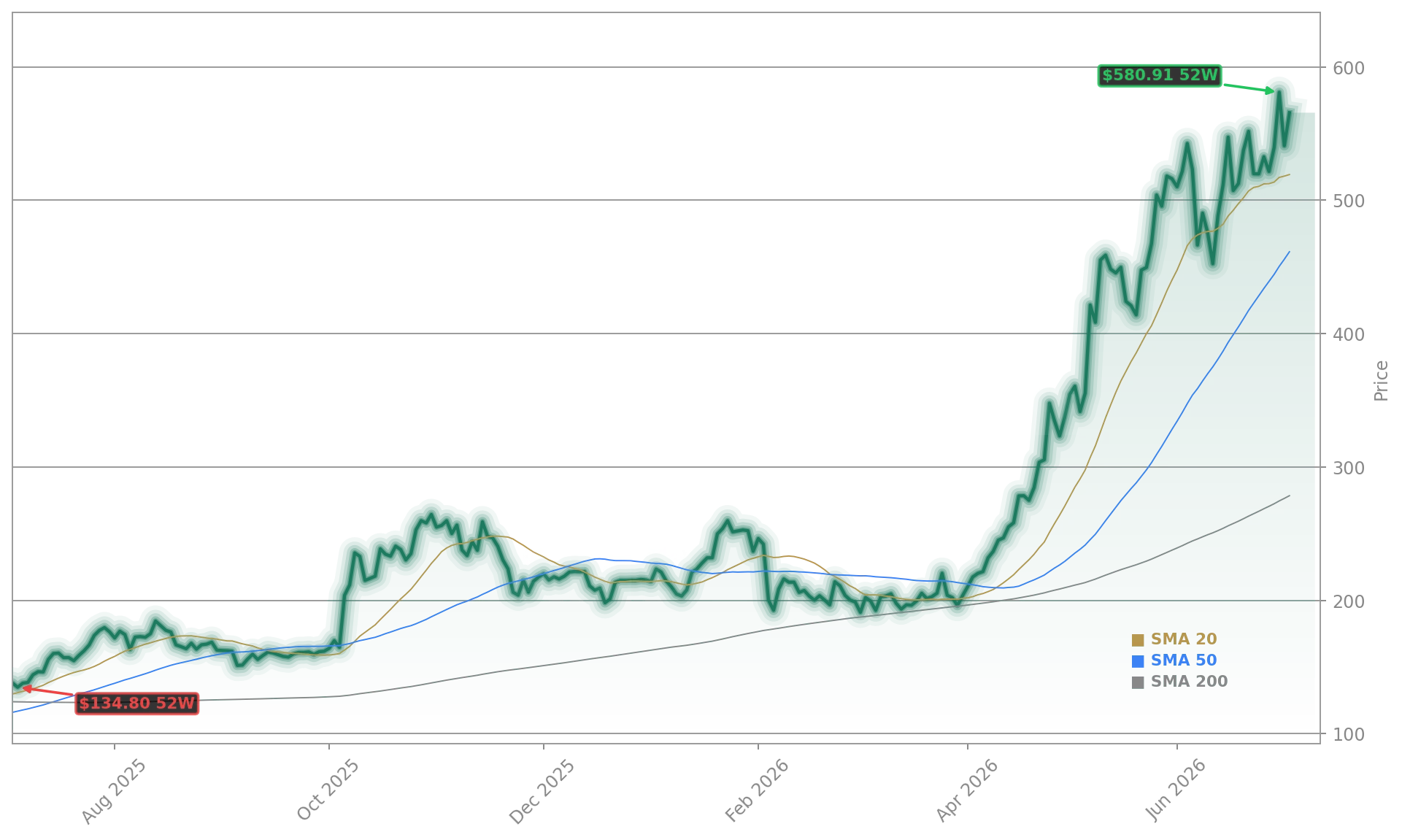

Advanced Micro Devices, Inc. jumped 9.69% to $568.95 on Monday, July 6, 2026 — its strongest intraday move in over three months — as Wall Street digested two pivotal developments: Goldman Sachs raised its price target from $450 to $640 and reaffirmed its Buy rating, and SemiAnalysis confirmed a material delay in NVIDIA’s Kyber rack system. Originally slated for 2027, Kyber — designed to integrate 144 high-end GPUs into a single AI supercomputer rack — is now expected no earlier than 2028 due to manufacturing failures in its PCB midplane. That gap gives AMD critical runway to scale its MI300X and upcoming MI325X deployments across cloud and enterprise data centers.

What Does the AMD AI Forecast Say About Server Demand?

The AMD AI Forecast now emphasizes server-side momentum — a shift from pure GPU acceleration to integrated CPU+AI compute stacks. Goldman Sachs analysts cite strong upside potential in AMD’s EPYC server CPU business, noting that over 70% of enterprise AI agent deployments rely on AMD-powered infrastructure to interface with legacy systems. This aligns with AMD’s June 16 agreement with Rackspace Technology for phased deployment of 30 MW of AMD AI Compute — a deal signaling real-world traction beyond benchmark sheets. Wells Fargo’s Aaron Rakers also boosted AMD’s price target to $615 on June 30, citing ‘underappreciated server CPU tailwinds’ and ‘strong design-win conversion in Tier-1 cloud partners.’

How Are Competitors Reacting to the Shift?

While NVIDIA grapples with Kyber’s delay, competitors are moving fast. Google is accelerating deployment of its in-house TPU v6 chips, but SemiAnalysis notes that AMD’s MI300X is now the second-most-deployed AI accelerator across eight major cloud partners — including Amazon Web Services, Microsoft Azure, and Google Cloud — all set to begin Rubin-series deliveries this fall. Meanwhile, Intel’s year-to-date outperformance has not translated into AI infrastructure share gains; its Gaudi 3 adoption remains concentrated in niche labs, not hyperscale production. Analysts at Truist Securities and UBS have downgraded near-term AI chip growth assumptions for Intel, citing ‘execution risk’ versus AMD’s proven scalability. In contrast, AMD’s Ventures division recently co-led a funding round for Turing — an autonomous driving startup deploying AMD chips in 10% of its AI stack — reinforcing its growing ecosystem credibility.

Is the AMD AI Forecast Too Optimistic?

AMD will be one of the biggest beneficiaries of the next phase of AI infrastructure spending, especially in the agentic AI era. AMD’s CPU architecture powers most enterprise servers, making it highly relevant as AI agents connect with existing corporate infrastructure.— Goldman Sachs analysts

Not according to current market signals. AMD’s implied volatility ratio (IVR) hit 102 — its highest level in 12 months — reflecting strong institutional demand and options positioning favoring upside continuation. Traders like Andrew, who added positions early and took partial profits at $550, $560, and $570, reflect broad-based momentum. The stock has not closed below its one-month moving average since its April breakout, and its 160% year-to-date gain is supported by tangible infrastructure wins — not just sentiment. Still, volatility traders caution that elevated IVR demands structured, directional premium selling — not neutral strategies — as momentum remains intact. With the S&P 500 up 1.8% and Nasdaq rebounding from last week’s semiconductor selloff, AMD’s strength is anchoring broader AI hardware leadership in the current quarter.