Can Lennar Earnings calm investors after a revenue miss and lower delivery target, or are housing headwinds just getting started?

Did Lennar Earnings Beat or Miss Estimates?

Lennar Corporation reported second quarter 2026 diluted EPS of $1.24, matching the consensus estimate per FactSet. On an adjusted basis — excluding $23 million in pretax mark-to-market losses on technology investments — EPS was $1.31, a 5.6% beat versus the $1.24 consensus. However, total revenue of $7.939 billion fell short of the $8.08 billion analysts anticipated, representing a 1.8% miss. Homebuilding revenue totaled $7.616 billion, down 2.9% year-over-year, driven by a 5% decline in average sales price to $371,000 — offset partially by a 2% increase in deliveries to 20,519 homes. Gross margin on home sales held at 15.6%, within prior guidance but below the 17.8% recorded in Q2 2025.

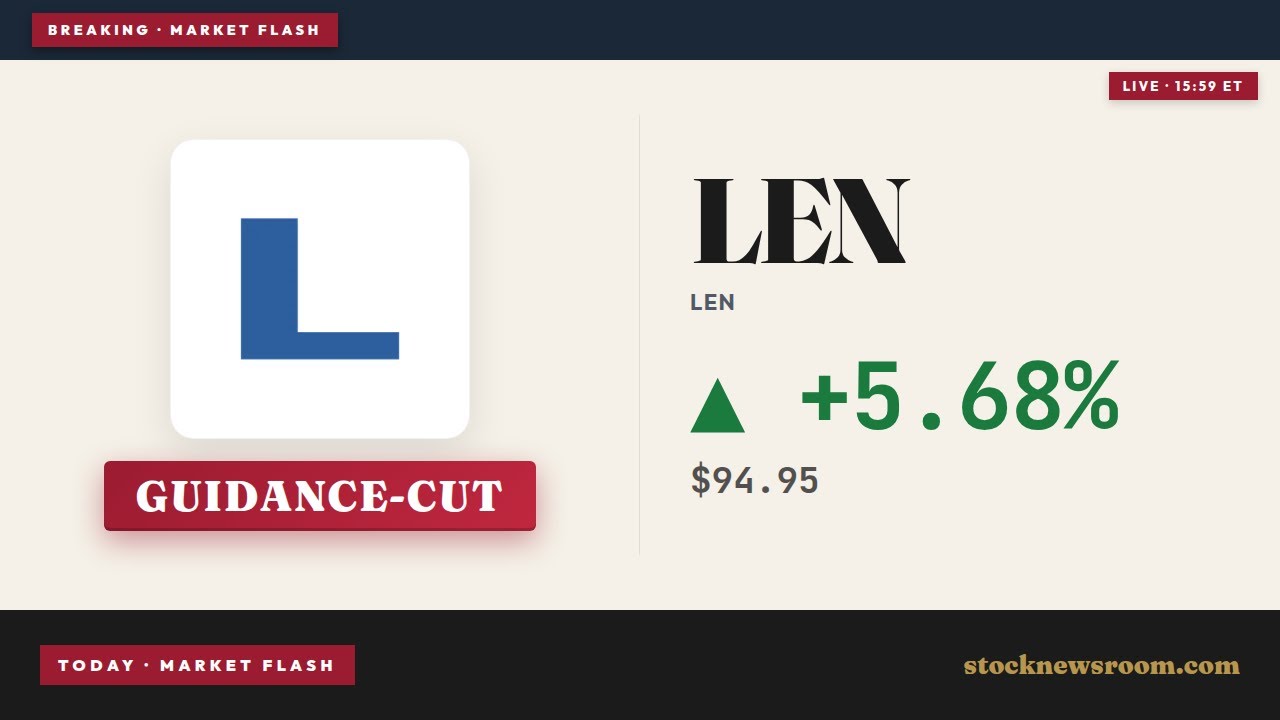

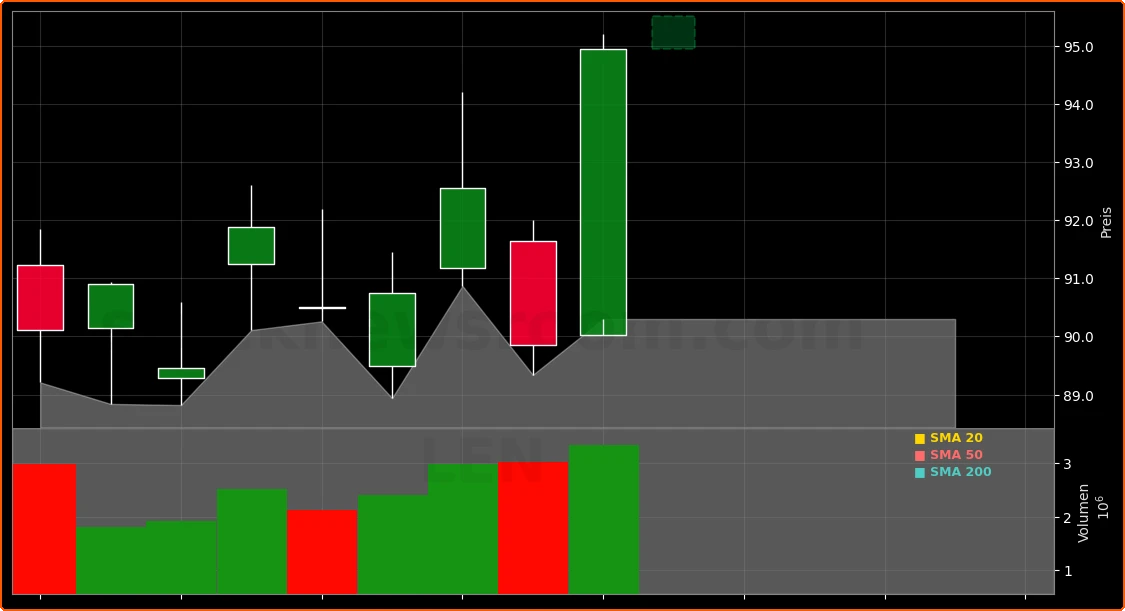

How Did Lennar Corporation’s Stock React?

Lennar Corporation shares declined 1.7% to $93.30 in after-hours trading, following a 5.7% intraday gain that lifted the stock to $94.95 at the close. The after-hours drop reflected investor concern over the revenue shortfall and the downward revision to full-year guidance — not earnings per se, given the EPS alignment with expectations. The stock remains down 7.6% year-to-date, underperforming the iShares U.S. Home Construction ETF, which is down 2.8% over the same period.

What Guidance and Strategic Details Did Lennar Corporation Provide?

Management moderated its full-year 2026 home delivery target from ~85,000 to 82,000–83,000 homes, citing ‘stubborn headwinds’ — including elevated mortgage rates, geopolitical uncertainty, and persistent affordability gaps. For Q3 2026, Lennar Corporation expects deliveries of 20,500–21,500 homes, average sales price of $375,000–$380,000, gross margin of ~16%, and SG&A as a percentage of home sales of 8.8%–9.0%. Backlog stood at 16,818 homes valued at $6.6 billion, while new orders declined 4% year-over-year to 21,749 homes. The company repurchased 5 million shares for $447 million and ended the quarter with $1.8 billion in cash and no borrowings under its $3.1 billion revolver.

What Are Analysts and Media Saying About Lennar Earnings?

Barrons highlighted the revenue miss and noted Lennar’s gross margin compression versus peers, citing land-banking costs and margin pressure from incentives — currently at 12.9% versus a normalized 4%–6%. The Wall Street Journal emphasized CEO Stuart Miller’s characterization of ‘stubborn headwinds’ and the strategic pivot toward volume-driven scale and cost discipline. Citigroup maintained its ‘Neutral’ rating but raised its price target to $102, citing improved inventory turnover and a narrowing incentive gap. RBC Capital Markets upgraded Lennar Corporation to ‘Outperform’, citing the strengthening balance sheet, record-low cycle time of 121 days, and the upcoming investor deck outlining its asset-light transformation. Oppenheimer reiterated its ‘Outperform’ rating but cautioned on near-term margin sensitivity to interest rate volatility.

What Does This Mean for Investors?

Our second quarter of fiscal year 2026 was defined by the same stubborn headwinds that have challenged the housing market for the past several years — persistently elevated mortgage rates, constrained affordability, and cautious consumer sentiment, exacerbated by geopolitical uncertainty creating a resurgent inflation reading of 4.2% driven by higher energy prices.— Stuart Miller, Executive Chairman, Chief Executive Officer and President of Lennar Corporation

Lennar Earnings confirm the company’s operational resilience amid macroeconomic stress — with delivery volume holding, margins stabilizing, and capital discipline intact. The guidance cut is a pragmatic acknowledgment of market reality, not a deterioration in execution. With $1.8 billion in cash, a net homebuilding debt-to-capital ratio of just 9.4%, and a newly announced investor deck outlining its technology and land-light model, Lennar Corporation is positioning itself for margin recovery as housing demand normalizes. The next catalyst arrives Friday, June 12, with the 11:00 a.m. ET earnings call and publication of the updated investor presentation — offering clarity on the path to sustained 16%+ gross margins and long-term earnings growth. For investors, Lennar Earnings signal not weakness, but strategic patience — and the foundation for a durable rebound once affordability improves. Lennar Earnings remain a critical barometer for the broader homebuilding sector — and the company’s ability to convert scale, efficiency, and technology into shareholder value remains intact.