Can Lennar Earnings prove that lower home prices today will translate into stronger margins and shareholder returns tomorrow?

What Do Lennar Earnings Reveal About Housing Demand?

Lennar Corporation reported Q2 2026 results on June 11, 2026—delivering 20,519 homes, a 2% increase year-over-year, while holding full-year guidance at 82,000–83,000 units. Yet revenue fell to $7.94 billion (from $8.38 billion), and EPS slid to $1.24 versus $1.81. The driver wasn’t weak deliveries—it was a $371,000 average sales price, the lowest since Q1 2017. That’s 5% below Q2 2025 and $41,000 below the current median existing-home price of $412,000. Lennar’s earnings highlight a structural pivot: competing on accessibility, not premium positioning. With first-time buyers now just 21% of the market—the lowest share in 44 years—Lennar’s price discipline is less a retreat and more a targeted response to a $1.2 million national housing shortage.

How Is Lennar Balancing Incentives and Margins?

Buyer incentives remained at 12.9%—well above the historical 4%–6% norm—but CEO Stuart Miller emphasized a key inflection: the gap is narrowing for the first time in three years. That’s critical context for Lennar Earnings interpretation. While gross margin on home sales dipped to 16% (from 18%), construction cycle time fell to a record 121 days, and construction costs improved 2% sequentially. Lennar also repurchased 5 million shares for $447 million at an average $89.35—near current levels—demonstrating confidence in its asset-light model (less than 5% of land on the balance sheet). Citigroup recently reiterated its ‘Neutral’ rating on Lennar Corporation, citing ‘pricing pragmatism as a competitive moat in a frozen affordability environment.’

What Does $371,000 Mean for Mortgage Affordability?

A $371,000 home financed at today’s 6.47% 30-year fixed rate carries a principal-and-interest payment of ~$2,340—$260 less than the $412,000 median resale home. That difference is material for buyers earning $75,000–$85,000 annually—precisely the cohort squeezed out of ownership. Lennar’s earnings show that new construction is now, unusually, the most accessible path to homeownership. This dynamic benefits not just Lennar, but downstream players like Home Depot (HD), whose pro-channel push faces headwinds in a low-turnover market—underscoring why RBC Capital Markets recently downgraded Home Depot to ‘Underperform’ amid ‘weakening builder order flow.’

How Are Competitors Responding to Lennar Earnings?

D.R. Horton and Toll Brothers are mirroring Lennar’s playbook—building smaller, more affordable floor plans and layering in financing incentives. Yet Lennar stands apart in execution: its 121-day cycle time is the industry’s fastest, and its 13% year-over-year drop in construction costs over two years outpaces peers. That operational edge supports its margin recovery outlook: guidance for Q3 2026 points to average prices of $375,000–$380,000 and gross margin stabilization near 16%. Goldman Sachs notes Lennar’s ‘margin floor appears in sight,’ with incentive compression now the most credible catalyst for near-term EPS expansion. For the S&P 500’s homebuilding sub-index—down 12% year-to-date—Lennar Earnings may mark the turning point.

What’s Next for Lennar Earnings and Shareholders?

The fundamental shortage of housing in America has not been solved. Demand is real, deferred, and building.— Stuart Miller, CEO of Lennar Corporation

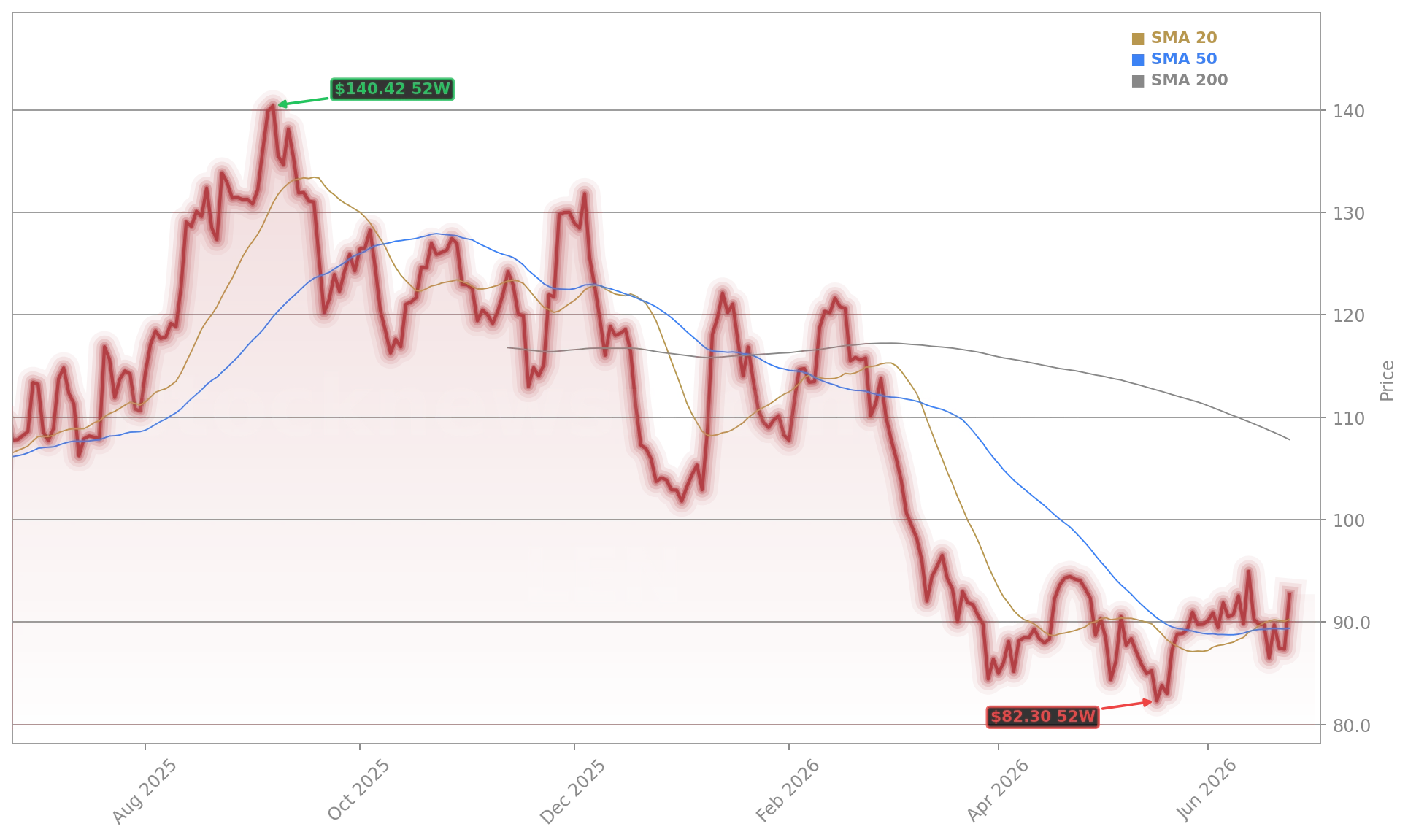

Lennar Corporation’s stock rose 6.08% to $92.66 on Wednesday, June 24, 2026—outperforming the broader S&P 500 and NASDAQ. With a $19.96 billion market cap and year-to-date decline of 14%, the shares remain discounted relative to long-term earnings power. Mortgage rate trajectory remains the wildcard: a Fed pause or cut could accelerate incentive normalization. Meanwhile, Lennar’s Q2 2026 results confirm a durable strategy—not a distressed reaction. As Miller stated plainly: ‘Demand is real, deferred, and building.’ That’s not just housing rhetoric; it’s the foundation for margin recovery, share buybacks, and renewed investor confidence. Related coverage includes Lennar Earnings +5.7% as Q2 Revenue Miss Sparks Warning, which analyzes investor sentiment post-guidance, and Home Depot Downgrade: $18B Deal Push Raises New Risks, examining how Lennar’s pricing pressure ripples into building materials demand.