Has Micron Earnings finally proved that memory is no longer cyclical, but one of the market’s most strategic AI trades?

Did Micron Earnings Beat Expectations?

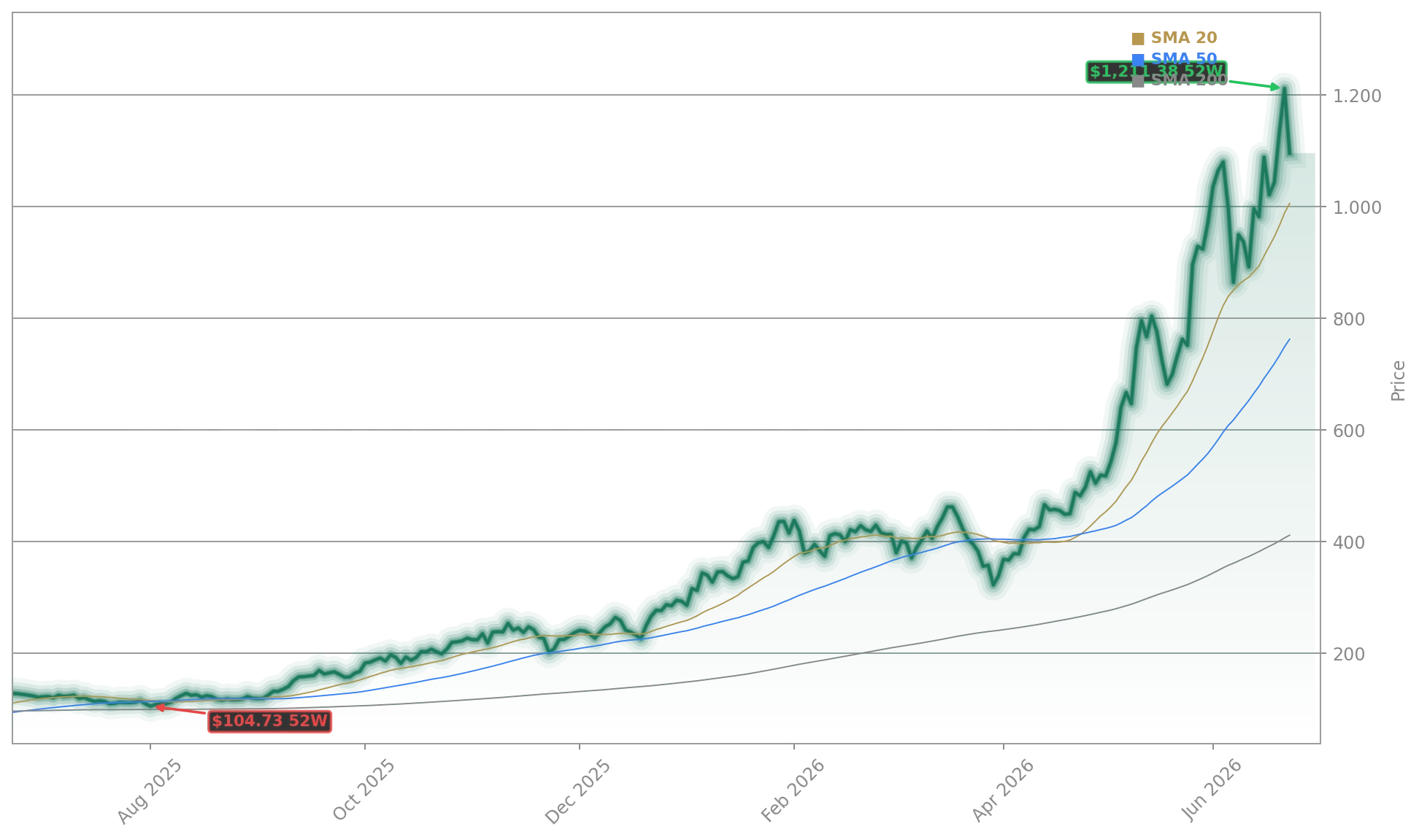

Micron Technology, Inc. delivered a historic fiscal Q3 2026 performance: $41.46 billion in revenue — a 346% year-over-year surge — and $25.11 in non-GAAP EPS, crushing the $20.86 consensus. Gross margin hit 84.9%, up from 74.9% in Q2 and far exceeding the 81% whisper number. The beat wasn’t marginal — it was structural. Cloud Memory and Core Data Center units combined for $25.3 billion in revenue, up 415% YoY and now representing 61% of total sales. With $25.39 billion in operating cash flow and $18.3 billion in adjusted free cash flow, Micron’s financial execution rivals software leaders — not traditional hardware firms. The company’s balance sheet strengthened to $30.2 billion in cash, marketable investments, and restricted cash.

What Does Micron Earnings Mean for the S&P 500?

As the fourth-largest holding in the Invesco QQQ Trust and a top-10 component of the S&P 500, Micron Technology, Inc. is no longer a niche semiconductor play — it’s a macro driver. Its 763% one-year gain and $1.37 trillion market cap mean its volatility directly impacts index futures, options flows, and sector rotation. Tonight’s results triggered an immediate 200-point surge in NASDAQ futures and lifted the entire SOX index. When Micron Earnings land, Wall Street doesn’t just price memory — it prices AI’s economic viability. With the S&P 500 trading at 20.8x forward earnings versus Micron’s 9.5x, the disconnect highlights how the market views memory as a non-cyclical, AI-enabled growth engine — not a commodity business.

How Does Micron Compare to AI Peers Like NVIDIA and Meta?

While NVIDIA dominates AI compute, Micron Technology, Inc. owns the critical memory bottleneck — and tonight’s results confirm its pricing power is now on par with, if not exceeding, chip peers. NVIDIA’s Q1 2026 revenue grew 85%, while Micron’s Q3 surged 346%. Where Meta and Alphabet report AI-related revenue growth in percentages, Micron reports it in tens of billions: $13.77 billion in Cloud Memory revenue alone. Crucially, Micron’s guidance implies $200 billion in annualized revenue — a scale that rivals legacy tech giants. Unlike Meta, which faces regulatory and ad-market headwinds, Micron’s demand is contractually locked: $22 billion in cash deposits from multi-year Strategic Customer Agreements. That visibility explains why Needham raised its price target to $1,550, TD Cowen to $1,500, and Susquehanna to $1,750 — all citing “sold-out HBM4 capacity through 2026 and deep 2027 allocations.”

Is the Memory Cycle Really Over?

For decades, memory was the textbook definition of a boom-bust cycle — until AI rewrote the rules. Micron Earnings reflect a structural shift: hyperscalers like Amazon, Microsoft, and Google are no longer buyers of memory — they’re long-term partners signing multi-year, floor-priced agreements. CEO Sanjay Mehrotra stated plainly: “In the AI era, memory has become a strategic asset for our customers.” That reframing is why CJ Muse of Cantor Fitzgerald projects $200 EPS by calendar 2027 — implying a $1,000+ stock at just 5x earnings. Goldman Sachs maintains a neutral rating but acknowledges “Micron’s earnings power is enormous,” while RBC Capital Markets upgraded to “Outperform,” citing “unprecedented margin durability.” The risk isn’t cyclical collapse — it’s capacity catch-up. Micron expects $27 billion in FY2026 capex and $10 billion in Q4 alone, with Idaho fabs online in 2027 and New York mega-fabs in 2030. But as one analyst noted: “It takes 36 months to build a fab — and AI demand is compounding every quarter.”

Micron Earnings: What’s Next for Wall Street?

Micron’s record fiscal Q3 financial results and even stronger outlook for Q4 reflect the strategic value of memory in the AI era.— Sanjay Mehrotra, CEO of Micron Technology, Inc.

The immediate catalyst is clear: Micron Technology, Inc. has validated the AI infrastructure thesis at scale. But the next test is duration — and that hinges on HBM4E ramp in 2027, G9 NAND adoption, and whether long-term contracts extend beyond 2027. With 39 buy ratings, 4 holds, and just 1 sell among analysts, consensus is bullish — yet the stock’s 10% post-earnings jump suggests the market still hadn’t fully priced in the magnitude of tonight’s guidance. As TD Cowen emphasized, “This isn’t just a beat — it’s a re-rating of memory’s role in compute.” For investors, the question is no longer whether Micron Earnings are strong — but whether the entire semiconductor supply chain can sustain this pace. The answer will shape the NASDAQ’s trajectory through year-end.