Can Micron Earnings justify sky-high AI memory expectations, or is Wall Street about to discover how expensive perfection can be?

Why Is Micron Earnings So Critical for the NASDAQ?

With Micron Technology, Inc. now the third-largest stock in the NASDAQ — ahead of many legacy tech giants — its earnings carry outsized influence on index composition, ETF flows, and sector leadership. The company’s 270% year-to-date surge has outpaced NVIDIA, Apple, and the broader SOX semiconductor index, making it both a beneficiary and a litmus test of AI-driven infrastructure spending. A miss on guidance — especially around high-bandwidth memory (HBM) order visibility or gross margin trajectory — could trigger cascading downgrades across the memory supply chain, including peers like SK Hynix and Samsung. Unlike typical earnings reports, Micron Earnings aren’t just about one company; they’re a real-time stress test for the entire AI capital expenditure narrative underpinning the 2026 bull market.

What Do Analysts Expect From Micron Earnings?

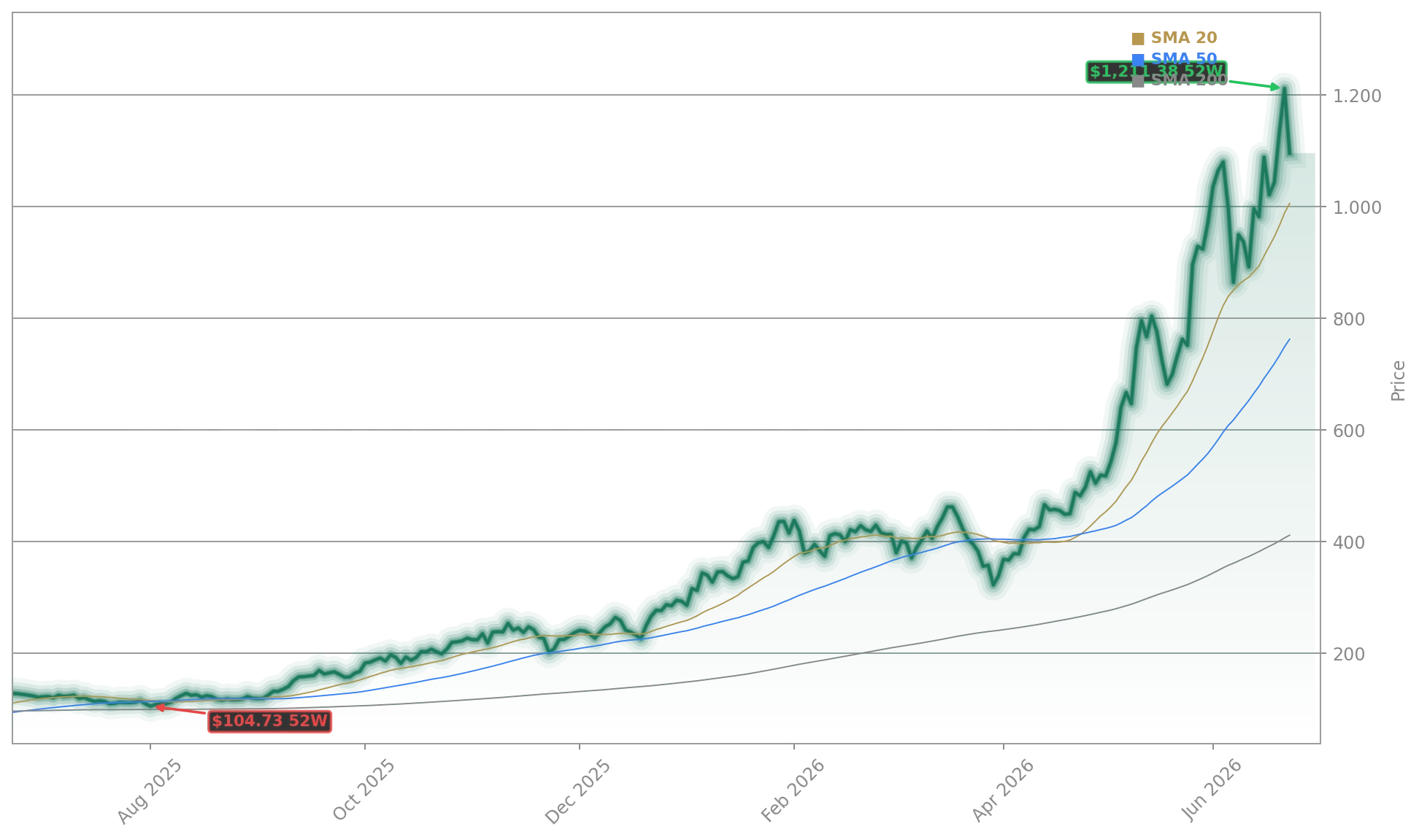

Consensus forecasts call for $20.98 in adjusted EPS on $34.5 billion in revenue — a 279% year-over-year jump — with gross margins near 81%. But expectations have shifted from ‘will they beat?’ to ‘how much will they raise?’ Bank of America recently lifted its price target to $1,500, citing HBM as ‘the new bottleneck’ in AI data centers. Meanwhile, TradingView analysts raised the 12-month average target to $1,123.28 — still implying modest near-term downside — while maintaining a collective ‘Buy’ rating from 49 analysts. Crucially, Goldman Sachs highlighted long-term agreements (LTAs) with major hyperscalers as a key catalyst, noting that Micron’s 2026 capacity is fully booked and 2027 is nearing full allocation. Yet Citigroup cautioned that ‘pricing power has peaked,’ urging investors to focus on margin sustainability over top-line growth.

How Is Competition Reshaping the Memory Narrative?

Micron Earnings arrive amid growing competitive uncertainty. SK Hynix’s recent pivot toward commodity DRAM — away from AI-optimized HBM4 — has rattled sentiment, raising questions about demand saturation and pricing discipline. That shift, coupled with South Korean leveraged ETF volatility — which triggered $6 billion in forced sales on Tuesday — has investors scrutinizing whether Micron’s dominance is structural or cyclical. While NVIDIA continues to drive demand for AI accelerators, memory suppliers now face divergent paths: Micron leans into premium HBM, Samsung balances AI and mobile DRAM, and SK Hynix appears to be recalibrating. This divergence makes Micron Earnings especially revealing: strong guidance would validate the ‘memory-as-infrastructure’ thesis; soft commentary could accelerate a rotation toward more diversified semiconductor plays like Lam Research, which Citi just upgraded on NAND equipment demand.

What’s at Stake for U.S. Portfolios?

For American investors, Micron Earnings matter beyond one stock. With MU now accounting for over 1.4% of the NASDAQ-100 and nearly 0.7% of the S&P 500, a 10% post-earnings move could swing the index by 3–4 basis points — more than many Mag7 components. Moreover, Micron’s options volume — $4.97 billion traded Monday alone — signals intense positioning, with calls outnumbering puts 4-to-1. That imbalance, however, masks a $25.3 million whale bet against the stock via July $1,000 puts — a rare hedge in a momentum-driven name. If Micron Earnings disappoint, the unwind could spill into U.S. semiconductor ETFs and pressure broader tech valuations, particularly in AI-adjacent names like Tesla and Microsoft — whose 20-year power deal with nuclear providers underscores the infrastructure intensity of modern AI scaling.

Micron Earnings: What’s the Real Risk-Reward?

Historically, Micron has beaten estimates for nine of the past 10 quarters — but traded lower after five of those six beats. That paradox reflects Wall Street’s ‘perfection premium’: with a $1.19 trillion market cap and 104% annualized volatility, the stock is priced for flawless execution. The bar isn’t just growth — it’s sustained margin expansion, multi-year capacity visibility, and credible evidence that memory scarcity extends well beyond 2026. A guidance cut — or even a pause in sequential growth — could trigger a swift re-rating, especially as the 2-year Treasury yield consolidates near 18-month highs. Conversely, confirmation of 2027 HBM sell-out and LTA expansion could catalyze a fresh leg higher, validating Bank of America’s $1,500 target and reinforcing Micron’s status as the central tollgate in the AI supply chain.

Related Coverage: Micron Earnings -10.3%: Anthropic Deal Meets Market Shock examines how a blockbuster partnership with Anthropic collided with Tuesday’s tech rout — revealing the fragility of AI-driven narratives when fundamentals meet momentum. Meanwhile, Microsoft AI Strategy: 20-Year Power Deal Signals Warning explores the infrastructure constraints — from electricity to memory — that could ultimately cap AI’s growth, making Micron Earnings not just a stock event, but a macroeconomic inflection point.

Micron Earnings are the defining moment for AI’s next phase. For U.S. portfolios, the outcome will determine whether memory remains the linchpin of the tech rally — or the first domino in a broader valuation reset. Investors should watch not just the numbers, but the language around capacity, pricing, and customer commitments. The next quarterly earnings will show whether the trend continues — and whether Micron Technology, Inc. can deliver on Wall Street’s $1 trillion bet.