Is the Intel Apple Deal a real foundry breakthrough for Intel, or just a politically charged headline the market ran too far with?

Is the Intel Apple Deal Real — or Just Political Theater?

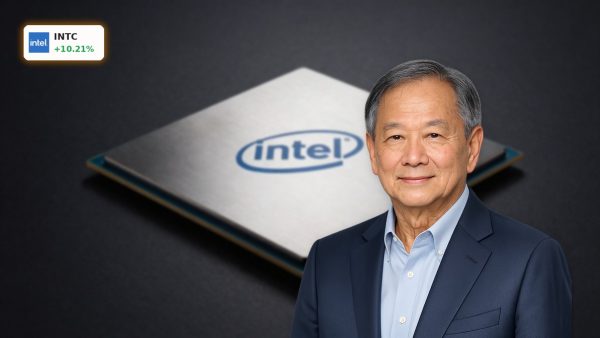

Despite no official confirmation from Apple or Intel Corporation, the market is pricing the Intel Apple Deal as functionally real. President Trump’s June 19 Truth Social announcement — stating Apple agreed to design and manufacture chips in the U.S. with Intel — ignited an immediate 10.2% intraday jump. The Wall Street Journal reported a preliminary agreement last month, and CounterPoint analysts now suggest Apple will test Intel’s 18A-P process for next-generation M7 processors in Mac and iPad devices. Yet yield concerns persist: Intel’s current 18A-P wafer output remains unproven at scale versus TSMC’s industry-leading 92%+ yield rates. Still, the symbolism matters — especially with Washington holding a $60 billion stake in Intel’s success.

How Does the Intel Apple Deal Fit Into the Broader AI Chip Race?

Intel’s foundry ambitions are no longer isolated. The company has secured a multibillion-dollar deal to build custom AI chips for Amazon, partnered with Nvidia on DGX Rubin servers, and joined Elon Musk’s Terafab initiative alongside SpaceX and xAI. This positions Intel not as a standalone competitor to NVIDIA, but as a diversified U.S. anchor in the AI infrastructure stack — from CPUs and chiplets to advanced packaging and domestic wafer supply. Meanwhile, Apple’s strategic calculus centers on supply resilience: with AI-driven memory and storage costs pushing iPhone Pro prices up $270, a second source on mature nodes is low-risk insurance. As Wedbush’s Dan Ives noted, U.S. manufacturing for Apple represents a massive opportunity during Apple’s 3–4 year AI-driven device cycle — one that could eventually shift meaningful volume away from Taiwan.

What Do the Numbers Say About Intel’s Foundry Turnaround?

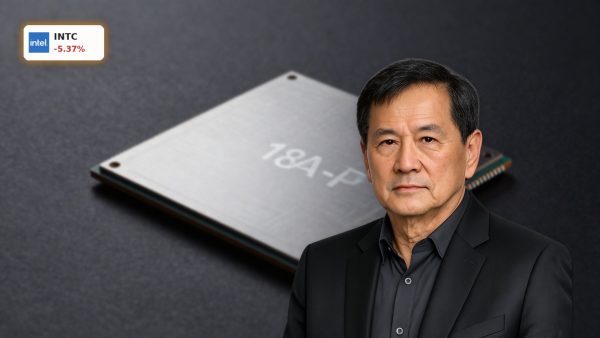

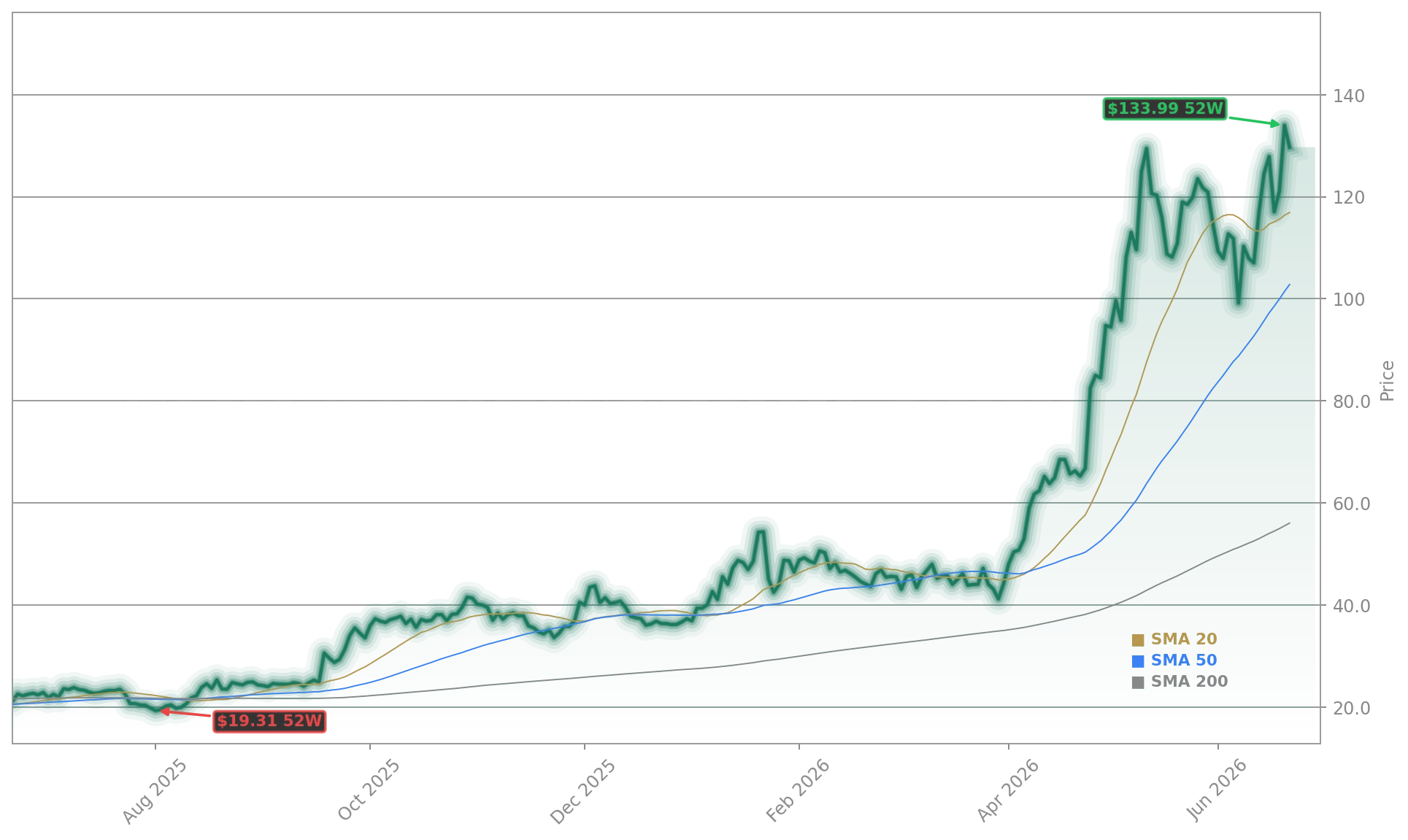

Intel’s Q1 2026 results — released in early May — show accelerating momentum: Intel Foundry revenue rose 16% year over year to $5.42 billion. However, just $174 million came from external customers — the rest was internal. The segment posted a $2.51 billion operating loss, underscoring that profitability remains years away. Still, CEO Lip-Bu Tan confirmed 18A-P has entered risk production, and non-GAAP gross margin expanded to 41%, signaling the ramp is gaining traction. Bank of America’s Vivek Arya recently upgraded Intel to Buy with a $135 price target, modeling foundry revenue surpassing $45 billion by 2030. Yet the Street remains cautious: 32 analysts hold, 13 buy, zero sell — with the average price target at $93.12, implying ~25% downside from current levels.

Intel Apple Deal: What’s at Stake for the S&P 500 and NASDAQ?

Intel at these prices, I mean, you’re betting on foundry success.— Bernstein’s Stacy Rasgon

Intel contributed 4 points of upside to the S&P 500 last week — the largest single-stock lift among tech names. Its 262% YTD gain has helped offset weakness in other semiconductor stocks, including Tesla-linked suppliers and memory players. With a $706 billion market cap — up from $184 billion at year-end — Intel now rivals major indices in weight and influence. Its surge reflects broader investor conviction in reshoring, AI infrastructure diversification, and CPU resurgence amid agentic AI workloads. Jim Cramer called Intel his “new favorite stock in this market,” citing the CPU-to-GPU ratio shift — up to four CPUs per GPU — as a structural tailwind no pure-play GPU vendor can replicate. The Intel Apple Deal, if confirmed, would cement that narrative and accelerate capital flows into U.S. semiconductor manufacturing — a core pillar of the CHIPS Act and 2026 national security strategy.