Could the Intel Apple Deal finally prove that Intel’s foundry comeback is more than just another market fantasy?

What triggered Intel’s record-breaking week?

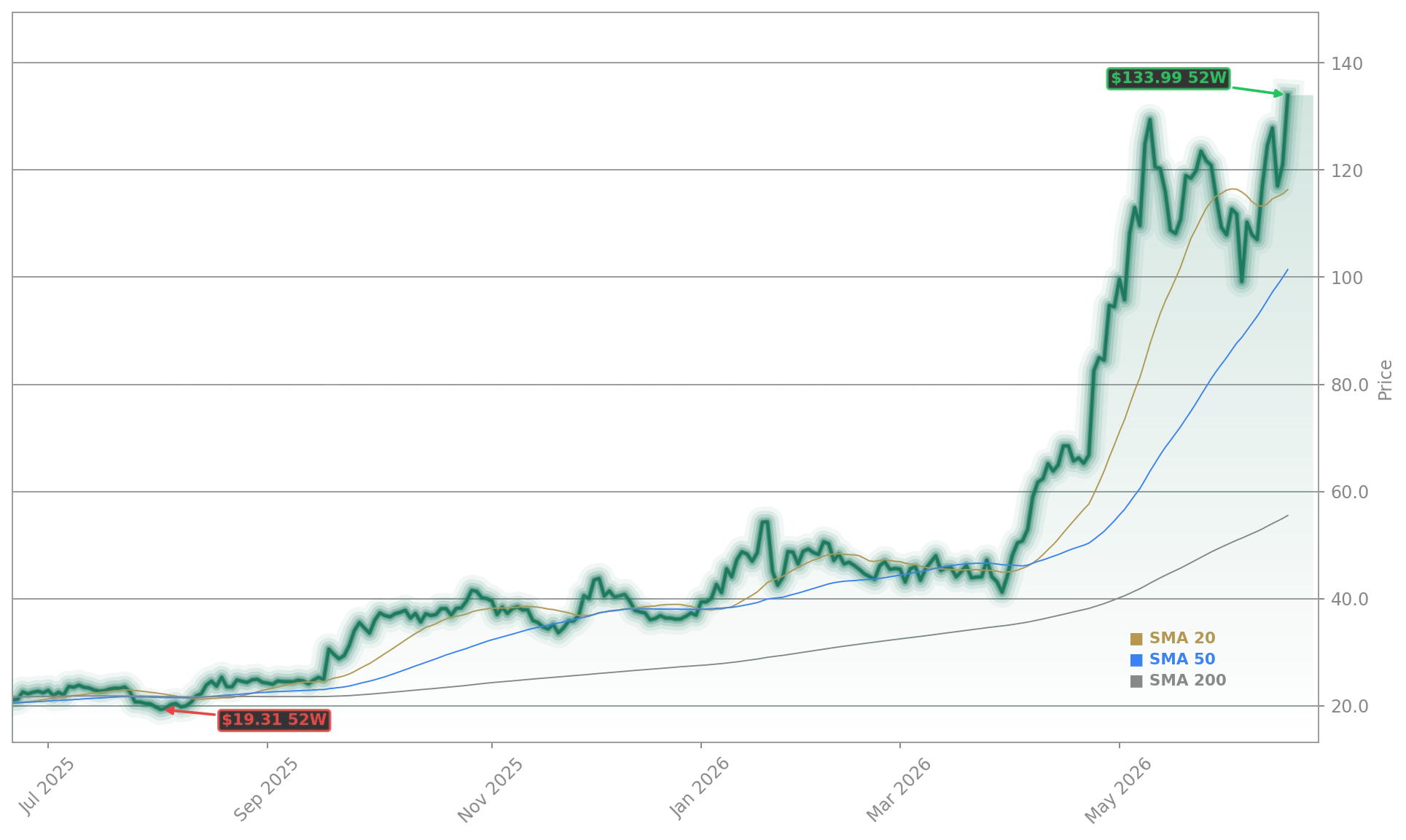

This week, Intel Corporation delivered its strongest weekly performance in over a year, surging +14.1% from Monday’s open at $117.42 to Friday’s close at $133.99. The weekly high of $135.48 marked a new all-time intraday high, while the low of $115.33 reflected early volatility before the catalyst cascade unfolded. The standout outlier was Thursday’s +10.6% surge—the largest single-day gain of the week—directly tied to President Donald Trump’s Truth Social announcement confirming the Intel Apple Deal. That post ignited a broad semiconductor rally, lifting the SOX index by 6.6% and propelling Intel to its first record close since May 11. While Tuesday’s –8.5% dip reflected broader tech selloffs and Fed hawkishness, the week’s trajectory was decisively upward, anchored by tangible technical progress—not just sentiment.

How did the Intel Apple Deal reshape investor expectations?

The Intel Apple Deal became the dominant narrative—not as a confirmed commercial contract, but as a powerful strategic signal. Though neither Apple nor Intel issued formal confirmation, The Wall Street Journal had reported a preliminary agreement last month, and analysts at Wedbush’s Dan Ives called U.S. manufacturing for Apple “a massive opportunity” amid Apple’s 3–4 year AI-driven device cycle. Counterpoint Research added specificity, suggesting Apple will test Intel’s 18A-P node for its next-generation M7 processor—targeting Mac and iPad devices. Crucially, this isn’t just about volume; it’s about validation. As Briefing.com noted, the Intel Apple Deal assigns “more value to INTC’s potential role as a strategic domestic manufacturing partner, not just its near-term earnings recovery.” The deal directly addresses Wall Street’s core skepticism: can Intel Foundry attract marquee external customers? With Apple joining Nvidia and Tesla as anchor partners—and the U.S. government holding a 9.9% stake now valued at over $60 billion—the answer shifted from “maybe” to “plausible.”

What technical milestones backed the rally?

Intel’s credibility wasn’t built on tweets alone. At the 2026 VLSI Symposium, Intel confirmed its 18A-P process node entered risk production—on schedule and with meaningful specs: 9% higher performance at isometric power or 18% lower power at isometric performance versus standard 18A. Engineers unveiled thermal resistance improvements of 20–40%, Power Boost transistors, and a 10X reduction in dynamic voltage droop. This wasn’t theoretical—it was executable. Simultaneously, Intel named Seok-Hee Lee, former CEO of SK Hynix, as Executive Vice President of Intel Foundry—bolstering advanced packaging expertise and signaling deep commitment to packaging as a standalone business. The appointment, alongside Navid Shahriari’s retirement, underscored a leadership pivot focused squarely on foundry execution.

How are analysts weighing in on Intel’s new trajectory?

Wall Street remains divided but increasingly engaged. Wedbush maintained its Outperform rating and highlighted the Intel Apple Deal as “genuine endorsement for Intel Foundry,” while cautioning that “yield and execution remain the swing factor.” Morgan Stanley upgraded Intel to Overweight, citing “accelerated foundry monetization potential” and raising its price target to $155. In contrast, Citigroup reiterated a Hold, emphasizing “persistent gross margin pressure” and the “multi-year path to foundry profitability.” The consensus remains cautious: 32 Hold ratings, 13 Buy ratings, and zero Sells—yet the average price target implies ~25% downside, revealing lingering skepticism despite the week’s momentum.

What catalysts dominate next week’s agenda?

Investors now await confirmation—direct from Apple or Intel—of technical scope, volume commitments, and node-specific timelines for the Intel Apple Deal. The 18A-P yield data, expected in late June, will be scrutinized for early signs of production readiness. Additionally, the U.S. government’s formal CHIPS Act disbursement schedule, Intel’s Q2 earnings preview (due June 25), and Fed commentary on inflation and rates will set the macro tone. With Intel now trading at a 52-week high and its 20-day moving average stabilizing after recent pullbacks, technical follow-through hinges on sustained institutional buying—and tangible proof that the Intel Apple Deal moves beyond announcement into execution.

Intel Apple Deal +8.2%: 18A-P Breakthrough Lifts Shares dissects how the 18A-P node’s technical specs align with Apple’s M7 roadmap and evaluates whether Intel’s foundry can realistically challenge Taiwan Semiconductor Manufacturing on yield and scale. The analysis weighs the $60 billion U.S. government stake not as passive support—but as active leverage to accelerate domestic capacity.

We’re going to need a ton of CPUs. CPUs are Intel’s bread and butter. As the demand for agentic AI explodes, it’s all about the ratio… it can go to as many as four CPUs for one GPU.— Jim Cramer, CNBC

Fazit folgt.