Could the Intel Apple Deal finally turn Intel’s foundry ambitions from a costly experiment into a credible long-term growth story?

What Does the Intel Apple Deal Mean for Foundry Profitability?

Intel’s foundry segment posted a $2.4 billion operating loss in Q1 2026 despite $5.4 billion in revenue—only $174 million of which came from external customers. An Intel Apple Deal would represent the first major validation of Intel’s 18A-P manufacturing process, which entered initial production in October 2025 and is now slated for testing on Apple’s next-generation M7 processor for Mac and iPad devices. Counterpoint Research analysts noted Apple is likely to use Intel’s 18A-P node for volume trials—but warned that yield rates remain unproven compared to Taiwan Semiconductor Manufacturing’s industry-leading benchmarks. Without meaningful wafer volume commitments, the Intel Apple Deal remains symbolic, not financial. Still, Wedbush analyst Dan Ives called U.S.-based manufacturing for Apple a ‘massive opportunity’ amid Apple’s 3–4 year AI-driven device cycle—potentially unlocking $5 billion+ in annual foundry revenue by 2028 if scaled.

How Is Intel’s New Leadership Structuring the Foundry Push?

Intel’s strategic pivot accelerated over the weekend with the appointment of Seok-Hee Lee as Executive Vice President of Intel Foundry—bringing deep semiconductor leadership from SK Hynix and SK On. Lee now oversees advanced packaging as a dedicated business line, while Naga Chandrasekaran continues leading front-end technology development. The move follows the retirement of Executive Vice President Navid Shahriari and underscores CEO Lip-Bu Tan’s focus on execution over optics. With the U.S. government’s 9.9% stake—acquired for $23.47 per share last summer and now valued at over $60 billion—Intel’s foundry ambitions carry unprecedented political and financial weight. Lee’s appointment signals a deliberate shift toward packaging and integration, areas where Intel aims to compete with ASE Technology and Amkor, not just TSMC.

How Does Intel Compare to Peers Amid the AI Chip Surge?

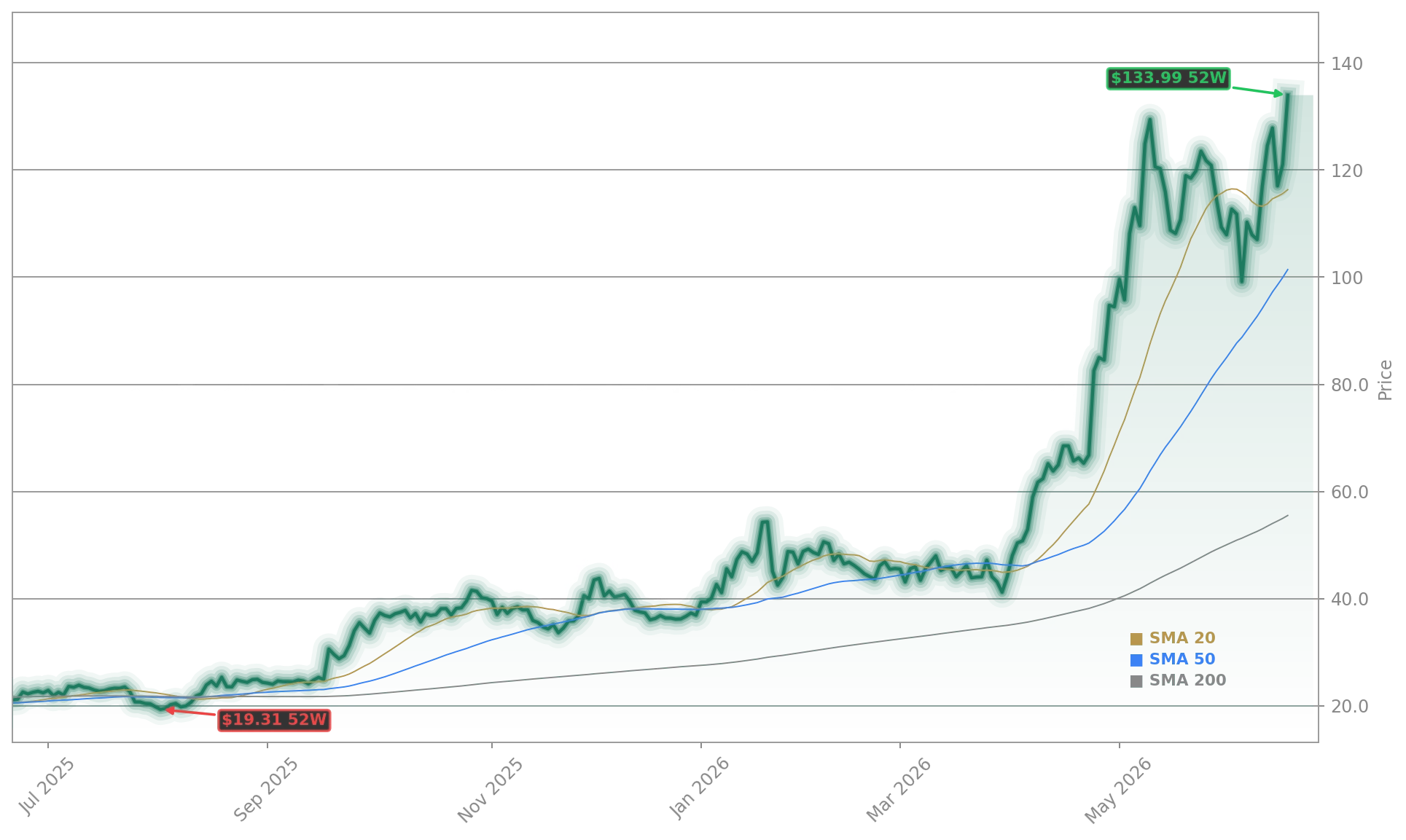

While Intel Apple Deal headlines dominated Thursday’s session, the broader semiconductor complex rallied alongside Intel: the SOX index closed up 6.6%, and NVIDIA rose 3.0% to $210.69, Advanced Micro Devices gained 2.8%, and Qualcomm climbed 6.17%. Yet Intel’s 509.86% gain from its 52-week low dwarfs even NVIDIA’s 215% YTD advance. Still, analysts remain divided. RBC Capital Markets maintains a ‘Sector Perform’ rating, citing execution risk in yield ramp and foundry margin recovery. Goldman Sachs sees upside but notes Intel’s non-GAAP gross margin guidance for Q2—39%—is down from 41% in Q1 and reflects ongoing supply constraints. In contrast, Taiwan Semiconductor Manufacturing reported 54% gross margins in its latest quarter, underscoring the gap Intel must close to sustain investor enthusiasm.

Is Wall Street Buying the Intel Apple Deal Narrative?

Despite the surge, Wall Street remains cautious: 32 analysts hold Intel, 13 rate it a ‘Buy’, and zero assign a ‘Sell’. The average price target implies ~25% downside from current levels, per FactSet data. The disconnect reflects skepticism over whether the Intel Apple Deal translates to material revenue before 2027. As Briefing.com noted, ‘The headline is more sentiment-driven than model-changing until there is clarity on scope, economics, production timing, and wafer volume commitments.’ Still, Jim Cramer called Intel his ‘new favorite stock in this market’ on Mad Money, citing the CPU-to-GPU ratio explosion in agentic AI infrastructure—where Intel’s core strength lies. With Intel now contributing ~7.2% of many tech-heavy portfolios, the stakes for U.S. investors couldn’t be higher.

What’s Next for Intel’s Foundry Roadmap?

Intel’s 18A-P node is just the beginning. The company expects design wins from external customers—including Apple, NVIDIA, and Amazon—in H2 2026, with volume production slated for 2027. Meanwhile, its $20 billion Ohio fab is on track for 2027 ramp, and the $10 billion Terafab project with Elon Musk is expected to begin construction this quarter. For investors, the near-term catalyst isn’t revenue—but confirmation: either from Intel’s Q2 earnings call in late July or Apple’s upcoming WWDC 2026 keynote. Until then, the Intel Apple Deal remains a powerful narrative—and a high-stakes test of whether America’s semiconductor sovereignty can be built on silicon, not just sentiment.

US manufacturing for Apple now represents a massive opportunity for Intel with Apple going into this 3-4 year AI-driven device cycle.— Dan Ives, Wedbush Securities

Related coverage includes Intel Apple Deal +10.2% Drives Record Foundry Surge, which analyzes how the reported partnership could validate Intel’s $150 billion foundry investment—and why Wall Street still demands hard data before upgrading its outlook. That article also explores how the Intel Apple Deal fits into broader U.S. industrial policy, including CHIPS Act disbursements and national security imperatives.