Is Tesla’s latest FSD probe just another headline scare, or the start of a deeper regulatory problem for TSLA?

What’s Driving Tesla’s 5% Intrady Drop?

Tesla (TSLA) fell sharply during intraday trading — not with the broader tech selloff, but in isolation. While the Nasdaq declined 1.3% and peers like Lucid (+1%) and Rivian (−1%) held steady, Tesla dropped over 5%, underscoring its unique sensitivity to regulatory and narrative risk. The catalyst: The Wall Street Journal confirmed NHTSA launched a special crash investigation into a June 19 fatal incident in Katy, Texas, where a Model 3 struck a home at high speed, killing 76-year-old Martha Avila. Harris County authorities stated the driver claimed he was using an automated driving assistance system — triggering immediate scrutiny of Tesla’s Full Self-Driving (Supervised) software. This Tesla FSD Probe comes as NHTSA’s engineering analysis into 3.2 million vehicles over FSD software has escalated to a pre-recall stage.

How Is Tesla Responding to the FSD Probe?

CEO Elon Musk and AI chief Ashok Elluswamy swiftly denied FSD involvement on X, citing a ‘high-speed crash’ inconsistent with FSD’s neighborhood-speed operation. Elluswamy added the driver manually pressed the accelerator to 100%, reaching 73 mph — a detail confirmed by vehicle telemetry. Nevertheless, the probe adds urgency to Tesla’s European regulatory challenges: while the Netherlands, Belgium, and Estonia recently approved FSD (Supervised), Sweden is now blocking continent-wide rollout unless Tesla modifies its driver-monitoring protocols. The Tesla FSD Probe thus isn’t just U.S.-focused — it’s a global compliance inflection point for a $1.5 trillion market cap company trading at a 371x P/E.

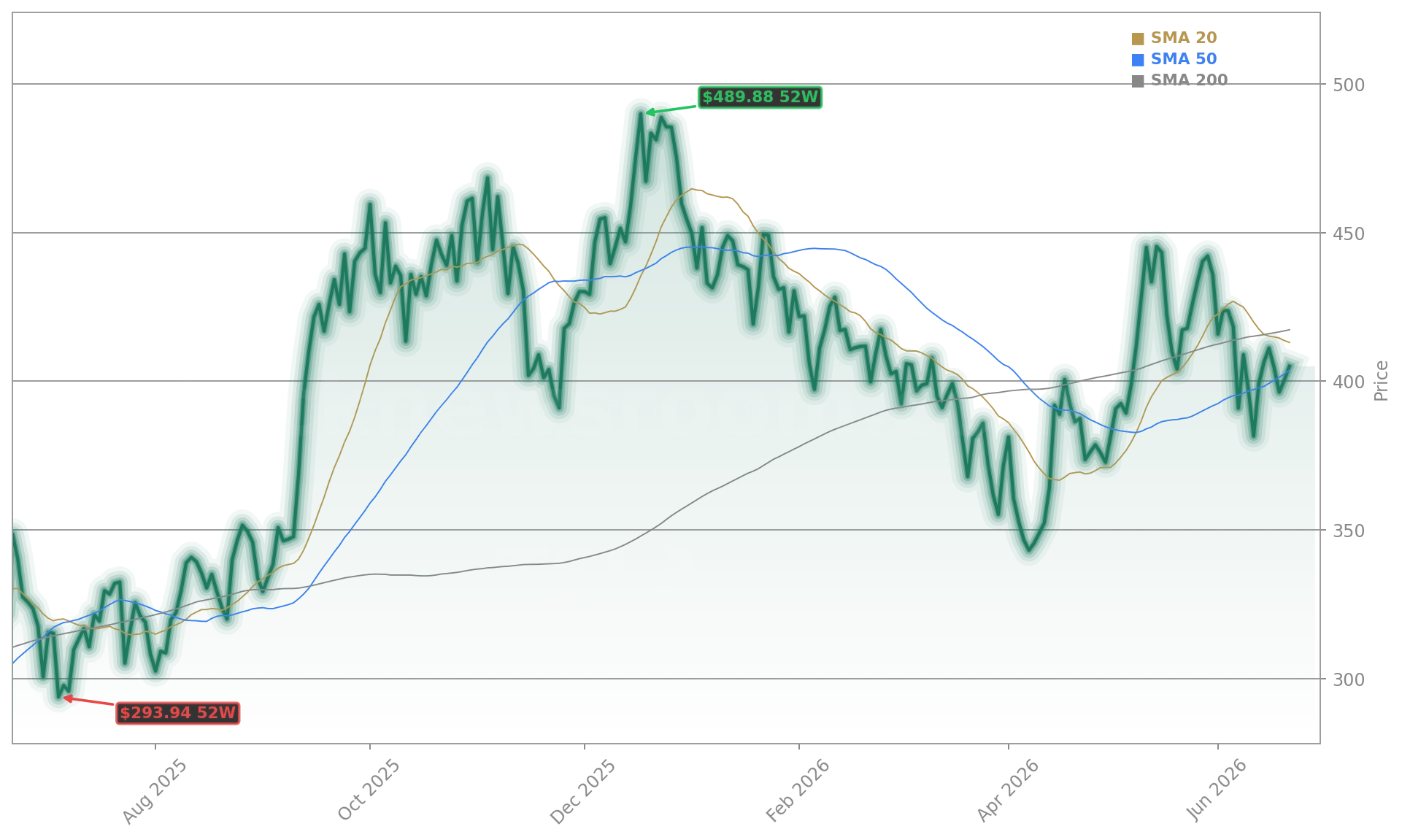

Why Did Tesla Jump 27% Last Month — Then Reverse?

Just weeks ago, Tesla surged 27% on robust Q1 delivery data (358,023 units, +6% YoY) and rising FSD subscriptions (1.28 million, +51% YoY). But momentum stalled as Wall Street digested reality: automotive gross margin remains at 21.1%, yet operating expenses rose 37% on AI and robotics R&D. CFO Vaibhav Taneja confirmed over $25 billion in 2026 CapEx — $3 billion of it earmarked for a new semiconductor research fab. Jefferies raised its price target to $375 but maintained a ‘Hold’ rating, citing ‘irrelevant traditional metrics’ and warning Tesla may increasingly trade as a ‘SpaceX proxy’ rather than an auto stock. Meanwhile, Goldman Sachs lifted its Q2 delivery forecast to 420,000 units — a 5% YoY gain — while Piper Sandler set a $500 target. The analyst price range remains the widest among megacaps: $25 to $500.

Is the NatPower Deal a Real Catalyst — or Just Noise?

Yes — and it’s strategically vital. Tesla and NatPower announced a $5 billion, multi-year European energy storage initiative — the first phase covering 25 GWh across Italy and the UK using Megapack systems and Autobidder trading software. Five initial projects will be owned and operated by NatPower, with a long-term goal of >100 GWh and projected $15 billion in revenue over 20 years. This directly supports Andy Lubershein’s ‘electro-industrial tech stack’ thesis — positioning Tesla not as an auto company, but as the keystone enabler of grid-scale power electronics. Critically, energy revenue — down 12% in Q1 — may reverse course. The deal validates Tesla’s pivot beyond vehicles, especially as rival BYD and Geely expand EV output across Europe. Unlike the Cybertruck or Optimus, this revenue stream is near-term, capital-light, and contract-backed.

Is a Tesla-SpaceX Merger Now Inevitable?

Not yet — but the structural alignment is accelerating. Musk exercised 304 million options, lifting his voting stake to 19.9% — a deliberate move to secure control ahead of AI-driven transformation. SpaceX’s $2.4 trillion IPO gives it both scale and liquidity for a stock-for-stock deal. Wedbush analyst Dan Ives assigns an 80% probability to a merger in H1 2027, while former Tesla board member Steve Wesley sees 50-50 odds. The synergy case is strong: shared AI infrastructure, Starlink-edge computing, battery and chip supply chains, and xAI integration. But investor caution remains: Oppenheimer’s Colin Rusch projects $29.4 billion in 2026 CapEx — up from $26.4 billion — warning that robotics and robotaxi initiatives will remain ‘loss centers’ through 2027. For U.S. portfolios, this means Tesla’s weight in the S&P 500 and NASDAQ is increasingly tied to physical AI execution — not just software promises.

This blatantly irresponsible reporting does more harm to people than they realize. Using Tesla self-driving is far safer than manual driving, and this was measured over 10B miles.— Ashok Elluswamy, Tesla VP of AI and Software

Tesla remains a core holding in the Magnificent Seven, but its role is shifting. While NVIDIA dominates chip-based AI and Apple leads in consumer AI integration, Tesla now targets the convergence of robotics, energy, and autonomous mobility. That ambition is why its stock reacts to NHTSA probes, European energy contracts, and SpaceX headlines — all at once.