Is Microsoft buying an AI future others may not be able to power?

What Does the Chevron Deal Mean for Microsoft AI Strategy?

Microsoft and Chevron announced a landmark 20-year power purchase agreement to supply 2.67 gigawatts of natural gas–fired electricity for Project Kilby — a massive AI data center campus in West Texas. Slated to begin delivering power in 2028, the facility bypasses the ERCOT grid entirely, operating as a behind-the-meter installation co-located with Microsoft’s infrastructure. This isn’t just about energy — it’s a structural bet on AI’s physical footprint. With $190 billion in 2026 capex guidance (61% higher than 2025), Microsoft is treating power as a first-tier competitive moat — alongside chips and cloud capacity. The deal signals that AI’s next bottleneck isn’t compute or models, but reliable, scalable, and controllable electricity. For investors, it reinforces Microsoft’s commitment to long-term infrastructure ownership — and raises questions about how quickly this capital intensity will convert to margin expansion.

Why Is Nadella Warning About AI Concentration?

In a widely cited Wall Street Journal interview, CEO Satya Nadella issued an uncharacteristically blunt warning: “If all the value is accrued by only a few models, the political economy will simply not tolerate it.” That statement — delivered outside earnings season and on his personal blog — reframes Microsoft AI Strategy as defensive infrastructure, not offensive model-building. Nadella is positioning Microsoft as the neutral orchestration layer: Copilot Cowork, launched globally in June 2026, enables dynamic routing across OpenAI, Anthropic, DeepSeek, and Microsoft’s own low-cost models. This multi-model, cost-optimized approach directly challenges the ‘winner-takes-all’ AI paradigm — and serves as both a hedge against regulatory backlash and a strategic pivot from dependency on any single partner. As The Wall Street Journal noted, this is less about losing the model race and more about owning the rails.

How Does Microsoft Compare to Amazon and Alphabet?

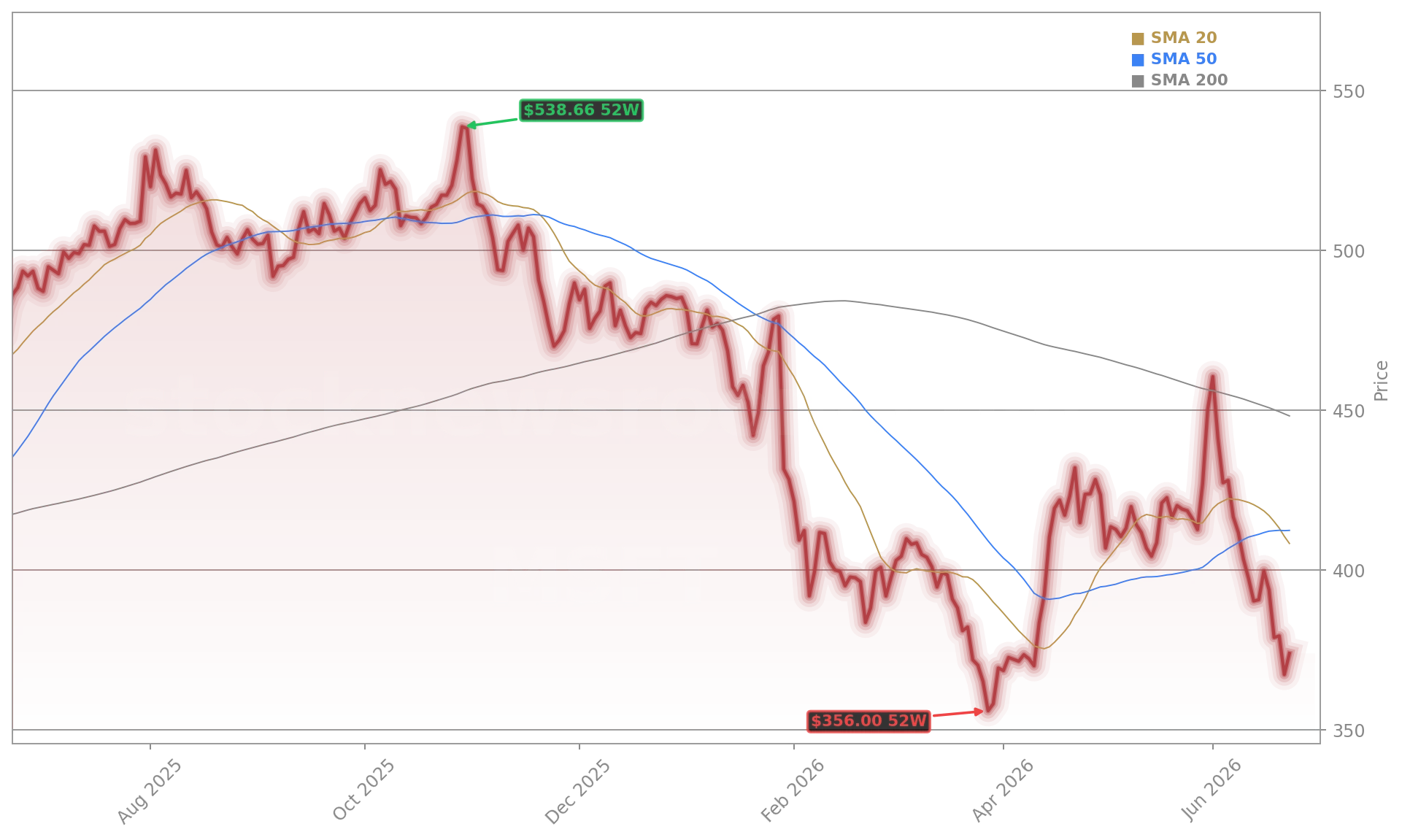

While Amazon and Alphabet report robust cloud growth — AWS and Google Cloud up 63% and 40% respectively — Microsoft stands apart in its explicit focus on AI economics and governance. Amazon continues to lead in cloud operating profit, and Alphabet’s Gemini momentum has driven cloud backlog near $460 billion. But only Microsoft has publicly tied AI scalability to energy contracts, antitrust framing, and enterprise workflow redesign. That divergence is reflected in price action: MSFT is down 21% YTD, while GOOGL is up 16% and AMZN is up 6%. Citigroup recently reaffirmed its Buy rating on Microsoft with a $540 price target, citing “multi-model execution and embedded enterprise distribution” as key differentiators. RBC Capital Markets likewise upgraded Microsoft to ‘Outperform’, highlighting its $627 billion commercial remaining performance obligations as “the deepest moat in cloud infrastructure.”

Is Microsoft AI Strategy Underpriced or Overextended?

At $374.64, Microsoft trades at 21.9x forward earnings — a 5% discount to the S&P 500’s 23.1x multiple — and with a 46.3% operating margin, it remains one of the most profitable companies in the S&P 500. Yet its free cash flow is under pressure: $30.88 billion in capex for Q3 FY2026 alone, up 84% YoY. Analysts are split on sustainability. Morgan Stanley maintains a $565 target and ‘Overweight’ rating, arguing that “Azure’s 40% growth is not capacity-constrained — it’s compute-prioritized,” meaning internal AI workloads are intentionally limiting external availability to fuel long-term stickiness. In contrast, Jefferies warns that “no self-imposed ceiling on capex relative to free cash flow” poses near-term execution risk. The market’s hesitation reflects this duality: extraordinary growth paired with unprecedented capital intensity — and a Microsoft AI Strategy that’s increasingly about control, not just capability.

What’s Next for Microsoft AI Strategy in Q2 2026?

With fiscal year 2026 ending June 30, all eyes turn to Microsoft’s July 27 earnings report — the first full-quarter readout after the Copilot Cowork launch and Chevron deal. Investors will scrutinize Azure’s growth trajectory, commercial RPO conversion rates, and whether AI revenue growth remains on track for the $37 billion annual run rate. The broader market context is shifting: QQQ is down 1.32% on the day, and the NASDAQ has pulled back 5.8% from its May highs. Yet Microsoft’s relative strength — up 1.7% while peers sold off — suggests institutional buyers are accumulating. For long-term investors, the question isn’t whether Microsoft AI Strategy is working, but whether Wall Street has finally priced in both its scale and its strategic patience. As one 24/7 Wall St. analyst put it: “This isn’t a correction — it’s a reallocation into infrastructure leadership.”

If all the value is accrued by only a few models, the political economy will simply not tolerate it.— Satya Nadella, CEO of Microsoft

Related coverage includes Microsoft AI Strategy: $37B Boom Faces Capex Warning, which analyzes the tension between explosive AI revenue growth and escalating infrastructure costs. Also critical is Palantir Zeta Partnership -2.8% as Valuation Fears Grow, offering a sector-wide lens on how investors are reassessing AI monetization models amid rising capex scrutiny.