Can Microsoft AI Strategy keep its profit edge as AI demand explodes but infrastructure costs rise even faster?

Is Microsoft AI Strategy shifting to cheaper models?

Microsoft is actively testing DeepSeek’s open-weight large language models for integration into Copilot Cowork, according to Axios. The move signals a strategic pivot toward usage-based pricing — away from the Pro-Seat model — and reflects intensifying pressure to contain soaring AI compute costs. While Microsoft remains deeply committed to its partnerships with OpenAI and Anthropic, rising token expenses and infrastructure capex have accelerated cost-optimization efforts. DeepSeek’s model, hosted within Microsoft’s own cloud infrastructure, could offer enterprise clients lower latency and tighter data governance than third-party APIs — without exposing sensitive workloads to external vendors. This aligns with broader hyperscaler trends: Alphabet, Amazon, and Meta are all building proprietary models to reduce reliance on external inference providers. For U.S. investors, the implication is clear — Microsoft AI Strategy is no longer just about scaling, but about sustainable unit economics.

How does capex pressure impact Wall Street sentiment?

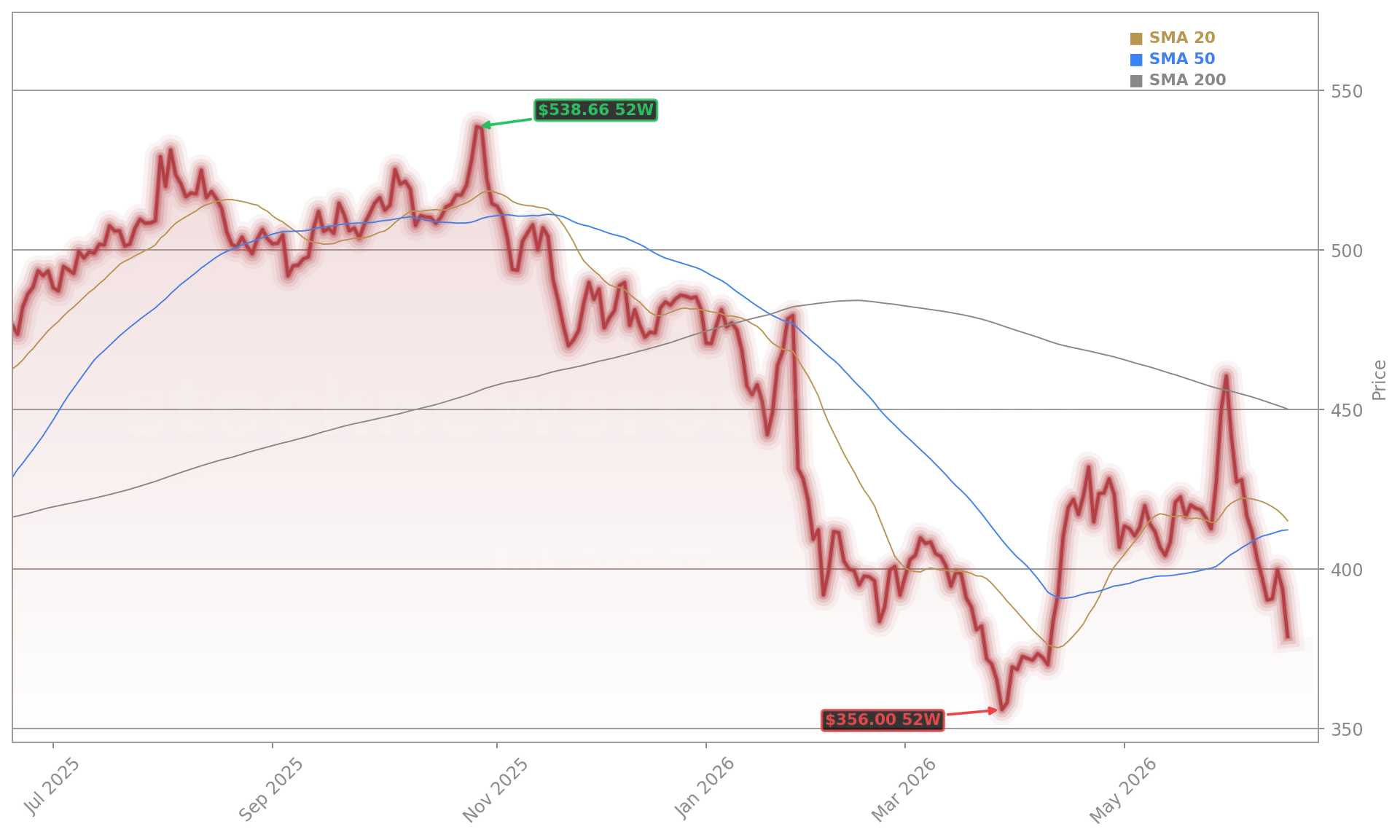

Microsoft’s Q3 FY2026 capex totaled $30.88 billion — up 84% year-over-year — and now accounts for nearly 90% of operating cash flow across the Big Four hyperscalers. That intensity has triggered concern despite stellar fundamentals: Azure grew 40%, Intelligent Cloud revenue hit $34.68 billion, and commercial remaining performance obligations (RPO) surged to $627 billion. Citigroup recently reaffirmed its ‘Buy’ rating on Microsoft but trimmed its 12-month price target to $545 from $565, citing ‘capex visibility risks’ and ‘uncertainty around AI infrastructure ROI.’ Meanwhile, RBC Capital Markets maintains its ‘Outperform’ rating, emphasizing Microsoft’s unmatched enterprise distribution and the $15 million paid Copilot seats already generating 10x year-over-year growth in daily active users. The divergence in analyst views reflects the core tension: explosive AI demand versus the balance sheet strain of building the world’s largest AI infrastructure stack.

What do options and insider trades reveal?

Bullish options activity surged ahead of Microsoft’s July 17 options expiration: a $450 call sweep traded 28 contracts for $32,300 — signaling strong conviction in a near-term rebound. Yet insider activity leans cautious. Illinois Representative Jonathan Jackson sold $15,001–$50,000 worth of Microsoft shares on May 12, 2026 — part of a broader pattern where congressional sellers have outnumbered buyers in the tech sector this quarter. Separately, Microsoft Commercial CEO Judson Althoff sold 15,500 shares at $460.99 on June 1. These moves don’t imply a fundamental breakdown — Microsoft has never suffered a 50% drawdown since 2000 — but they reinforce investor wariness amid rising infrastructure leverage. Notably, Microsoft created a $100 billion off-balance-sheet AI Infrastructure Partnership in late 2024, with $70 billion in fund-level debt. That structure insulates the balance sheet but adds long-term contractual obligations that could pressure margins if AI monetization lags.

How does Microsoft AI Strategy compare to peers?

While NVIDIA powers the AI stack and Apple prepares its on-device Siri AI rollout this fall, Microsoft is the only megacap with a fully integrated AI productivity layer across Microsoft 365, GitHub, and Windows. Its $37 billion AI run rate dwarfs Meta’s nascent ad-supported AI efforts and exceeds Amazon’s AI services revenue — though AWS remains the cloud leader in total scale. Crucially, Microsoft’s AI monetization is enterprise-first and contract-backed, unlike the consumer-facing models of Tesla or OpenAI-backed startups. That gives it superior revenue visibility — but also raises the stakes for delivering ROI on its $30B+ quarterly infrastructure spend. As 24/7 Wall St. notes, Microsoft’s forward P/E has compressed to 21x despite accelerating top-line growth — a valuation discount that only narrows if Azure growth holds above 30% and capex begins converting meaningfully into margin expansion.

What’s next for Microsoft AI Strategy?

The next catalyst arrives in late July, when Microsoft is expected to announce commercial availability of agentic Copilot workflows — enabling autonomous task execution across Outlook, Teams, and ERP systems. That capability could unlock $10B+ in incremental annual revenue by FY2027, per Goldman Sachs estimates. Meanwhile, DeepSeek integration could go live as early as Q4, offering a lower-cost tier for mid-market customers. With the S&P 500 up 10% year-to-date while Microsoft lags, the stock remains a key barometer for Wall Street’s AI confidence. If monetization accelerates and capex growth moderates, the path to $500 — and beyond — remains intact.

Our AI business surpassed an annual revenue run rate of $37 billion, up 123% year-over-year.— Satya Nadella, CEO of Microsoft

Related coverage: Can Microsoft AI Strategy keep winning in the real world even as Wall Street suddenly worries about capex, costs, and the OpenAI relationship? Microsoft AI Strategy: $37B AI Boom Meets Stock Warning. Has Wall Street finally underestimated how much agentic AI could expand AMD’s server opportunity? AMD Forecast: $170B Server AI Boom Lifts Wall Street Targets.