Can Apple AI Strategy turn privacy-first AI and a foldable iPhone into the next major earnings engine for investors?

What Does Apple AI Strategy Mean for S&P 500 Investors?

Apple’s AI strategy isn’t about chasing benchmarks—it’s about embedding intelligence invisibly across its ecosystem while preserving privacy as a defensible moat. Unlike NVIDIA-driven server-side AI or Microsoft’s Copilot-first cloud monetization, Apple’s hybrid model processes sensitive tasks on-device and offloads complex inference to secure cloud nodes. Citigroup analysts Asiya Merchant and Atif Malik call this a ‘foundational step’—not a catch-up move. That distinction matters for U.S. portfolios: Apple’s 38.6% weighting in the technology sector of the S&P 500 means its execution on AI directly impacts index performance. With Apple’s Q2 2026 revenue growth at 16.6%—still below the industry’s 104.96% average but far ahead of peers like Hewlett Packard Enterprise and NetApp—the company’s AI strategy is less about top-line acceleration and more about margin resilience and services monetization.

How Does Apple AI Strategy Compare to Microsoft and Meta?

While Microsoft integrates OpenAI across Office and Azure, and Meta leans into open-weight models and AI-powered ad targeting, Apple’s AI strategy is uniquely constrained—and uniquely valuable. It avoids third-party model dependencies beyond its Gemini partnership, prioritizing on-device latency, battery life, and regulatory compliance. That gives Apple leverage in Europe and emerging markets where data sovereignty is non-negotiable. Citigroup notes Apple could layer AI value into iCloud+, Apple Music, and Apple Fitness+ via tiered subscriptions—mirroring Google One’s AI premium tiers. Meanwhile, Meta (META) has yet to monetize its AI investments meaningfully, and Microsoft’s $20B+ annual AI infrastructure spend remains a cost center until Copilot+ adoption broadens. For U.S. investors, Apple AI Strategy represents a lower-risk, higher-margin path to AI monetization—especially as App Store commissions on AI-enhanced apps could generate $2.1B+ annually by 2027, per Citigroup estimates.

Is the Foldable iPhone a Catalyst for Apple’s Hardware Roadmap?

Yes—and timing couldn’t be sharper. IDC forecasts foldable smartphone shipments will surge 30% in 2026, with Apple poised to capture 22% of that market by year-end. Leaks embedded in iOS 27 beta code, Bloomberg reporting, and analyst consensus from Ming-Chi Kuo all point to a September 2026 launch. Priced at $1,999, the foldable iPhone targets high-margin adoption—not volume. That’s critical: Apple’s hardware gross margin sits at 44.3%, dwarfing competitors like Samsung and Western Digital. With iPhone 17 shipments up 4.4% year-over-year amid a 2.9% global smartphone decline, Apple’s brand strength gives it pricing power where others cut costs. Citigroup expects the foldable to contribute $8.2B in incremental revenue in its first full year—enough to lift Apple’s fiscal 2026 EPS by $0.38.

Why Is Apple AI Strategy Critical for NASDAQ Mega-Cap Exposure?

Because Apple is the second-largest holding in QQQ (7.10%), VUG (12.32%), and VOO (7.05%). Its performance doesn’t just move tech—it moves the entire index. While NVIDIA dominates AI infrastructure headlines, Apple’s AI strategy delivers the user-facing layer that drives engagement, retention, and repeat purchases. That’s why Apple’s ROE of 30.39%—12.03 percentage points above its industry peers—and $39.32B in EBITDA signal durable cash flow, not just hype. With Apple’s debt-to-equity ratio at 0.8—lower than Seagate, Western Digital, and Hewlett Packard Enterprise—it’s also the safest mega-cap lever for AI exposure. For investors watching the Nasdaq-100’s 45% concentration in the top 10 names, Apple AI Strategy isn’t optional—it’s foundational.

Apple AI Strategy: What’s Next for Wall Street?

WWDC marked a ‘foundational step’ in Apple’s AI strategy.— Asiya Merchant and Atif Malik, Citigroup

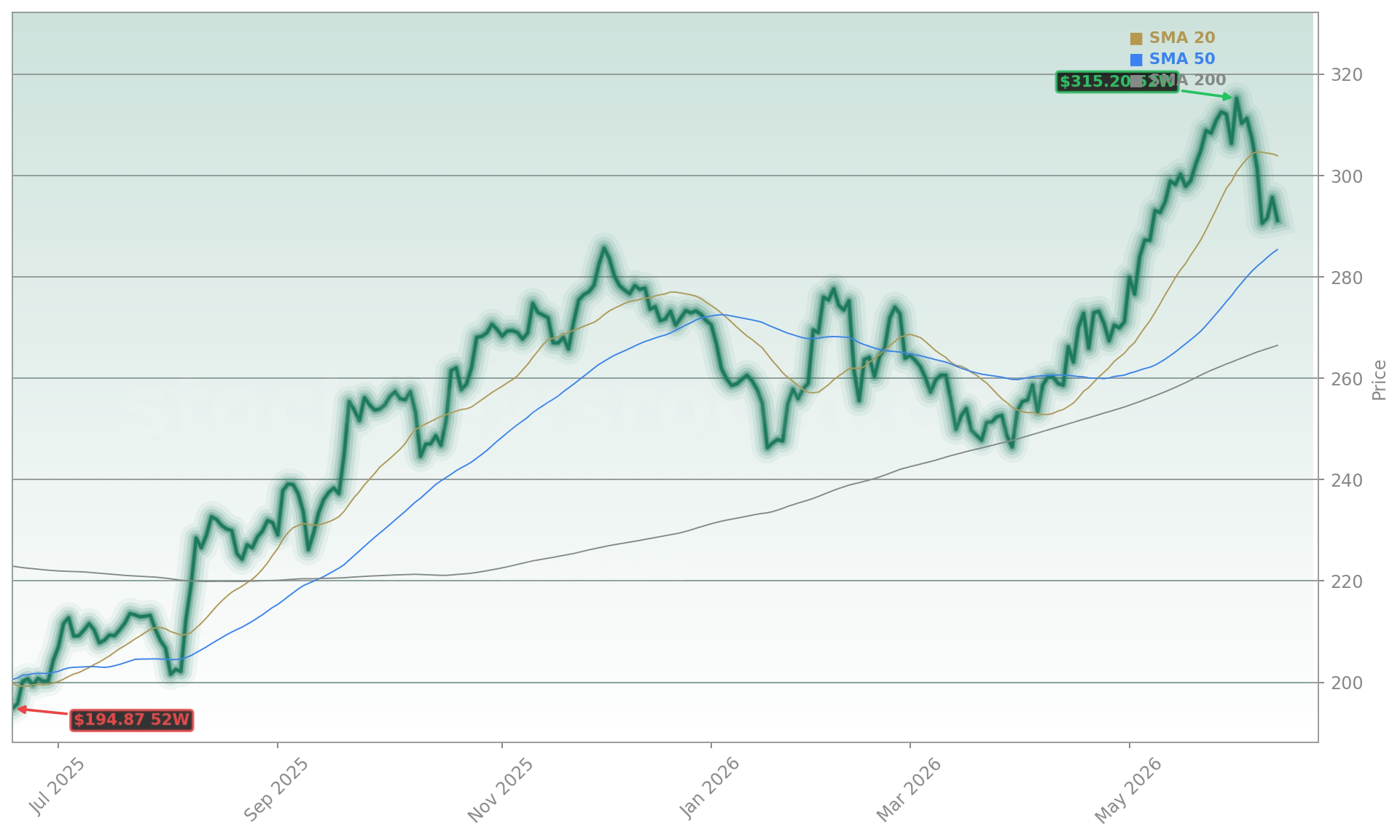

The next catalyst arrives in early July, when Apple is expected to release its first developer preview of Apple Intelligence APIs—giving third-party developers early access to on-device Siri enhancements and multimodal capabilities. Citigroup expects this to trigger a wave of AI app submissions ahead of the iOS 27 public release in September. With Apple’s stock up 9% year-to-date but down 3% since WWDC, the market is pricing in skepticism. Yet the $315 price target implies 6% upside—and that’s before foldable revenue, AI-driven services growth, and potential Vision Pro synergies. For U.S. investors, Apple AI Strategy isn’t just about smarter devices. It’s about owning the most profitable, defensible, and scalable AI interface in consumer tech.