Can Microsoft AI Strategy keep winning in the real world even as Wall Street suddenly worries about capex, costs, and the OpenAI relationship?

What drove Microsoft’s -5.7% weekly slide?

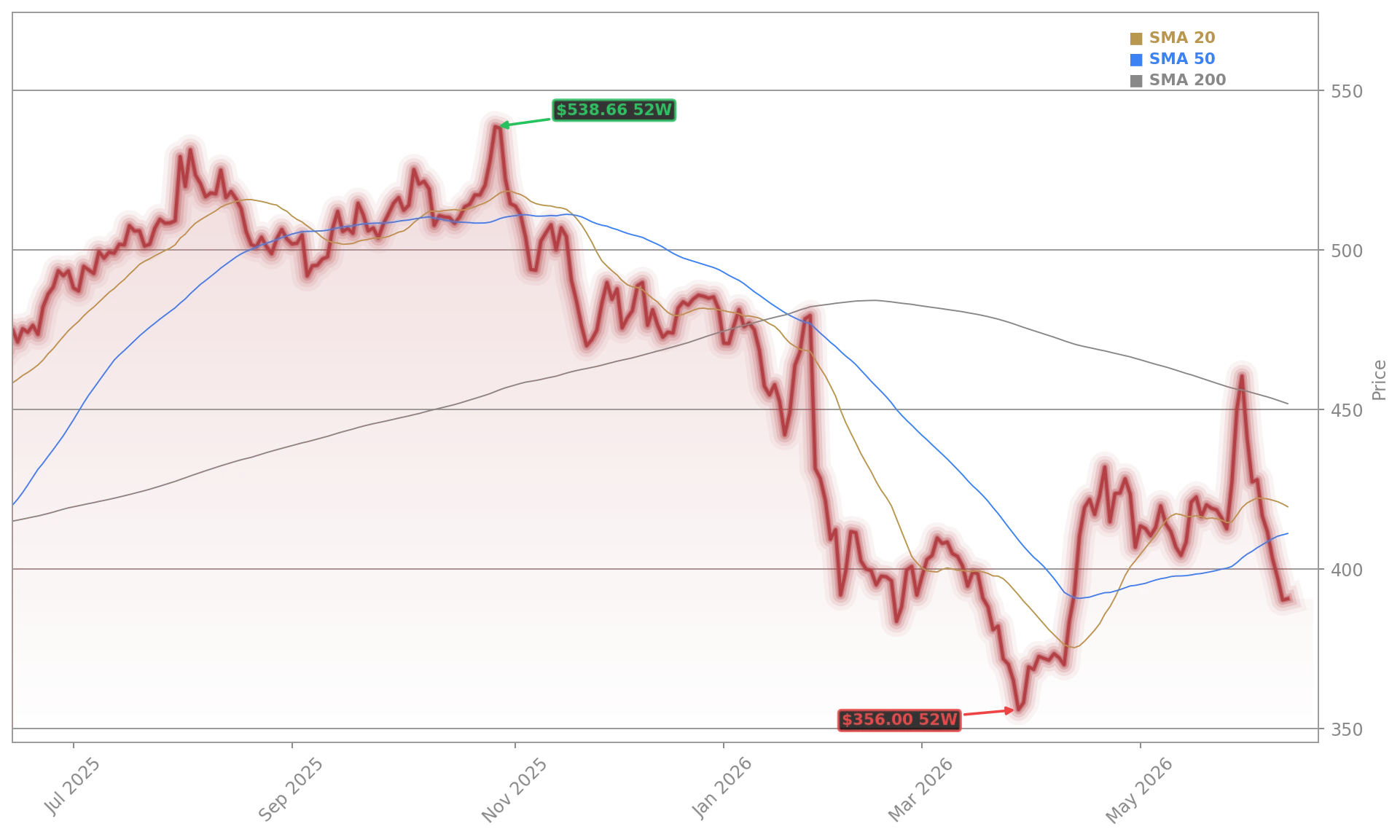

This week, Microsoft closed at $390.74, down -5.7% from Monday’s open of $414.14, with a weekly high of $417.16 and low of $382.27. The decline was steady — no single day saw a move ≥3% — but cumulative pressure built across five consecutive down days, culminating in the worst weekly performance since March 2020. The slide was not driven by earnings or guidance misses, but by a convergence of macro and strategic concerns: hyperscaler capex fears reignited after Oracle announced $70 billion in fiscal-year capex, while OpenAI’s confidential IPO filing — and its evolving, less-exclusive partnership with Microsoft — triggered repricing of the AI revenue synergy premium. Wells Fargo warned that surging AI token costs now pose a ‘death knell’ for hyperscaler stocks like Microsoft, shifting focus from growth to sustainable unit economics.

How did NHS England and Atos validate Microsoft AI Strategy?

Despite the price action, Microsoft AI Strategy gained powerful real-world validation. On Monday, NHS England announced the largest healthcare AI rollout in history: 505,000 clinicians and staff will receive Microsoft 365 Copilot, following a trial that saved users 43 minutes per day on administration. By Friday, Atos Group — the French global system integrator — confirmed a workforce-wide deployment of Copilot to all 56,000 employees across 54 countries, making it the first French GSI to adopt Microsoft 365 E7 and Agent 365 for end-to-end AI agent governance. These deals weren’t pilots — they were production-scale, security-first implementations. As Atos’ CDO stated, this is ‘the most significant technology investment in our people that Atos has made in a generation’ — and it’s built entirely on Microsoft AI Strategy.

Why did analysts maintain bullish price targets despite the pullback?

Analysts held firm on Microsoft’s long-term AI monetization thesis. BNP Paribas reiterated its Outperform rating and $555 price target, citing accelerating Copilot adoption and potential evolution to a higher-value seat-plus-consumption model. Citigroup maintains a Buy rating with a $550 target, while TD Cowen and Cantor Fitzgerald stand by $540 and $502, respectively. The consensus price target remains $560.95, implying ~40% upside from Friday’s close. Their confidence rests on hard metrics: AI annual revenue run rate hit $37 billion (+123% YoY), Azure grew 40% YoY, and commercial remaining performance obligations surged to $627 billion (+99% YoY). As one analyst noted, Microsoft is the ‘cleanest enterprise AI compounder’ — a view reinforced by its 46% operating margin and forward P/E of just 21.

What catalysts should investors watch next week?

Next week brings three critical catalysts. First, the Roundhill MSFT WeeklyPay ETF goes ex-dividend on June 15, distributing $0.08163 per share — a reminder of Microsoft’s cash-generating power. Second, investors will parse management commentary on AI efficiency: CEO Satya Nadella’s recent warning — ‘Don’t use frontier models for non-frontier problems’ — signals a strategic pivot toward cost-conscious AI adoption. Third, the market will monitor reactions to the securities class action lawsuit alleging misleading statements on Copilot and capex — a legal test of Microsoft AI Strategy’s transparency. Also looming: continued scrutiny of data center backlash, as local opposition to AI infrastructure spreads across the U.S., with implications for Microsoft’s Azure growth trajectory.

This week proved that Microsoft AI Strategy delivers tangible, large-scale value — from NHS England’s frontline care to Atos’ global operations. Yet the market punished the stock for the capital intensity underpinning that strategy. The key takeaway is not weakness, but recalibration: investors are no longer buying AI hype, but demanding proof of disciplined execution. With Copilot seat adoption accelerating, AI revenue now materializing, and a deeply discounted valuation, Microsoft remains the most actionable AI platform play for long-term investors. Microsoft AI Strategy isn’t in question — its monetization pace and capital efficiency are now the focus. For those who understand the difference, the current price offers a compelling entry point.

Don’t use frontier models for non-frontier problems.— Satya Nadella, Microsoft CEO

Related coverage: Microsoft’s Xbox division is preparing significant layoffs and budget cuts as CEO Asha Sharma overhauls the gaming business amid declining revenue — a clear signal that AI now commands priority over legacy consoles at Microsoft Xbox Layoffs -2% as AI Pivot Hits Gaming. Meanwhile, Broadcom’s record $22.2 billion in AI revenue sparked a brutal stock selloff, underscoring how hyperscaler capex concerns are spreading across the AI infrastructure stack — a dynamic directly relevant to Broadcom Earnings at $22.2B: Record AI Revenue, Stock Tanks.