Can Microsoft AI Models turn heavy AI spending into a stronger lead in coding, cloud, and enterprise software?

Why are Microsoft AI Models driving shares?

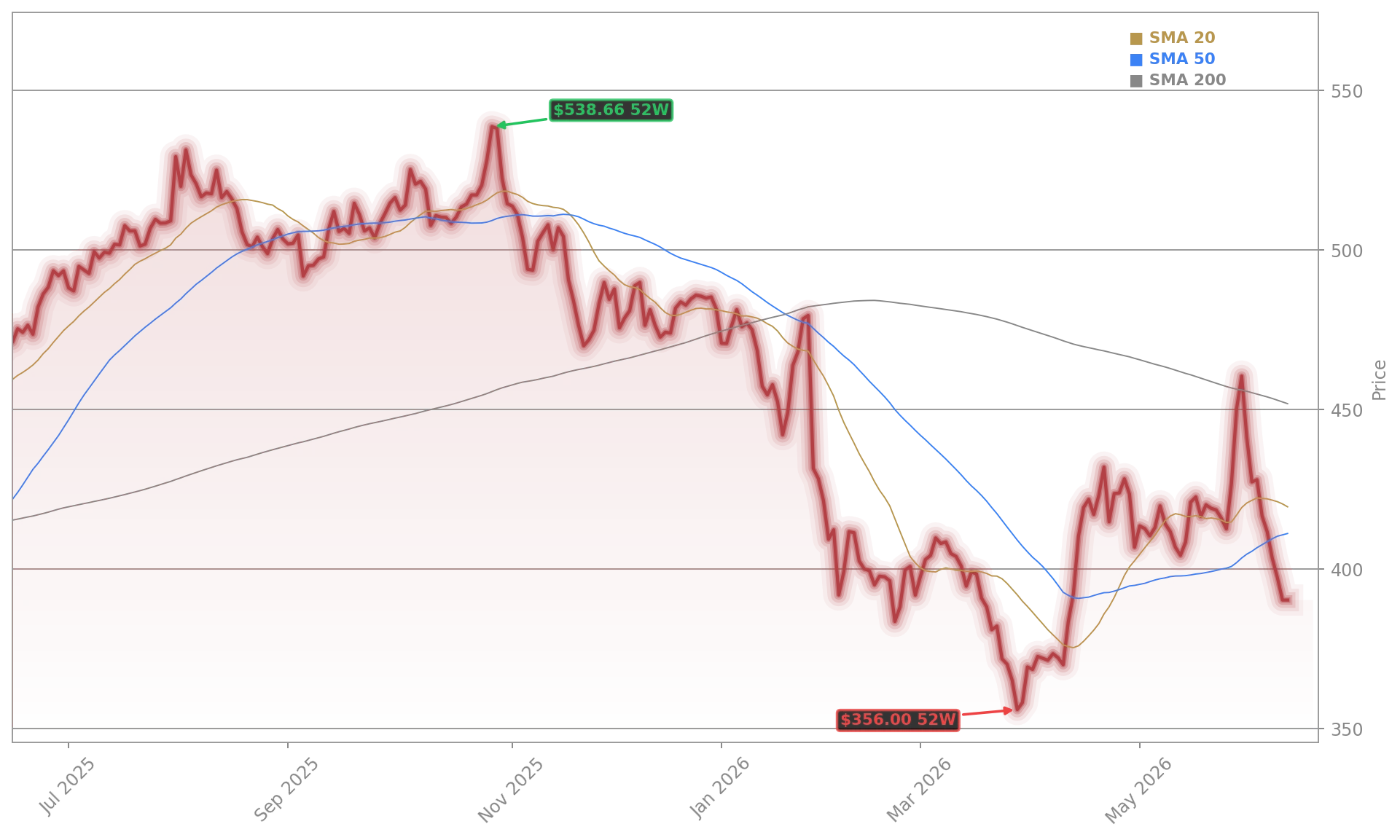

Microsoft was one of the stronger large-cap technology names on Thursday, climbing to $426.20 from a previous close of $414.58. The move followed fresh details on a broader product rollout that includes a coding model for GitHub Copilot as well as models focused on transcription, speech, images, and reasoning. For investors, the significance goes beyond one event. The launch suggests Microsoft is accelerating efforts to build more of its own stack instead of leaning as heavily on OpenAI, while also responding to fast-moving competition from Anthropic and Google.

That matters because Copilot remains one of Microsoft’s most visible AI monetization products. Early adoption was encouraging, but rivals have become more aggressive in AI-assisted coding. A stronger in-house model lineup could improve margins, product differentiation, and customer retention across software development workflows. Wall Street has also been watching unusual call activity in Microsoft shares, a sign that some traders were positioned for a positive catalyst.

Can Microsoft defend AI leadership?

Microsoft still sits at the center of the AI infrastructure build-out, alongside Amazon, Meta, and Alphabet. Spending on data centers, chips, networking gear, and cloud capacity remains enormous, and Microsoft’s capital expenditure plans continue to be viewed as relatively insensitive to interest-rate pressure. That helps explain why suppliers tied to memory, servers, and storage have also benefited from the hyperscaler race.

At the same time, investors want proof that spending is translating into durable returns. Azure growth is a key watch item, especially after signs of some moderation in earlier updates. Microsoft has said its AI business reached an annual run rate of $37 billion, up 123% year over year, showing that demand remains substantial. Still, questions persist about pricing, customer usage, and whether enterprises will absorb higher AI-related costs after some products shifted from fixed pricing toward usage-based models.

Competition is getting tighter as well. Apple remains a software ecosystem giant, while NVIDIA continues to anchor the hardware side of the AI trade. Meta is pushing deeper into AI infrastructure, and management there has even floated the possibility of building a cloud business around excess capacity, a direct challenge to Microsoft Azure, Amazon Web Services, and Google Cloud.

What else should investors watch at Microsoft?

Beyond products, investors are balancing several crosscurrents. Microsoft is reportedly exploring AI startup acquisitions to deepen talent and model capabilities. The company is also offering early retirement packages to about 7,000 employees, a reminder that even AI leaders are managing costs carefully while spending aggressively on compute.

Elsewhere, Microsoft’s government business remains a support factor. The Pentagon recently awarded Dell Federal Systems a five-year $9.7 billion contract to consolidate Microsoft software licensing across military branches and related agencies, reinforcing the company’s entrenched role in public-sector IT. On the security side, Microsoft is expanding Defender features that automatically isolate infected PCs, although cyber risks remain elevated after new warnings tied to attacks on Microsoft 365 users.

No fresh analyst rating changes from firms such as Citigroup or RBC Capital Markets were disclosed in the available reports Thursday, but the market reaction showed that investors are willing to reward visible execution in AI. With the stock still below prior peak levels, sentiment appears sensitive to any sign that Microsoft AI Models can convert heavy infrastructure spending into stronger product adoption and cloud growth.

Related Coverage: Investors tracking Microsoft’s AI investment cycle may also want to read this analysis of Microsoft’s $17.5 billion India expansion, which examined whether rising infrastructure commitments can produce enough Azure and Copilot demand to justify the spending. That earlier coverage complements today’s focus on Microsoft AI Models by showing how regional capacity build-outs and product launches are increasingly part of the same monetization story.

Microsoft AI Models are now a central test for the stock’s next leg higher. If Build delivers better Copilot performance, clearer product differentiation, and signs that Azure can keep converting AI demand into revenue, Wall Street may become more constructive on Microsoft again. For investors, the next catalyst is straightforward: execution.