Can NVIDIA Earnings keep justifying sky-high AI expectations, or is even record growth no longer enough for Wall Street?

Why are NVIDIA Earnings moving the stock?

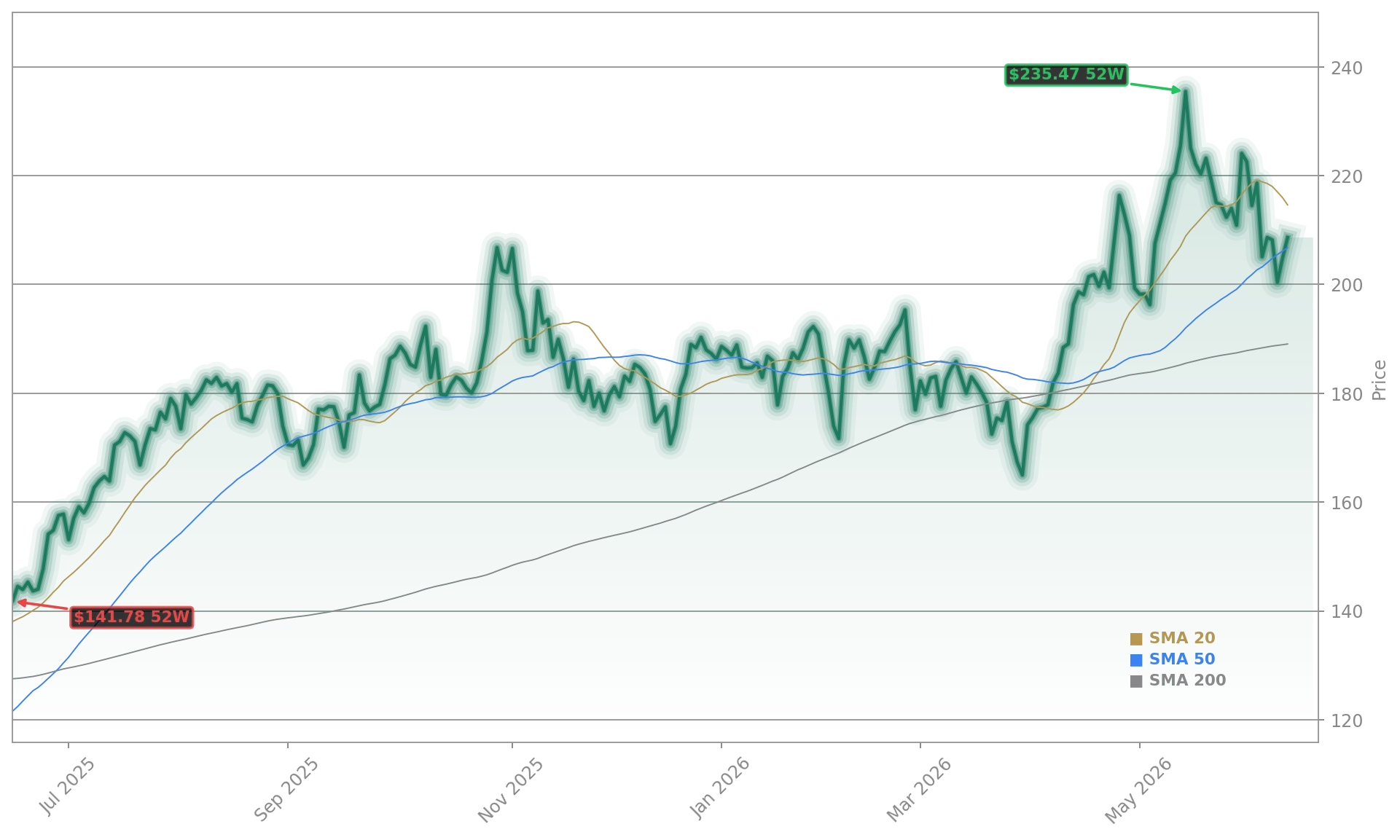

NVIDIA Earnings again underscored why NVIDIA remains the defining AI infrastructure name for US investors. The company reported quarterly revenue of $81.6 billion, up 85% year over year, while data center revenue reached $75.2 billion, up 92%. Adjusted earnings per share came in at $1.87, ahead of expectations, and management guided for roughly $91 billion in revenue for the current quarter.

Even so, the market reaction was muted. NVDA was down 1.70% from the prior close at the time of writing, suggesting investors wanted an even larger beat after the stock’s sharp run into the report. That pattern has become more common for mega-cap AI leaders as expectations keep climbing faster than fundamentals can comfortably clear them.

NVIDIA also approved an additional $80 billion share repurchase authorization and sharply increased its dividend, reinforcing the message that cash generation is now becoming part of the investment story alongside hypergrowth.

Can NVIDIA hold its AI lead?

The central debate after NVIDIA Earnings is no longer whether demand is strong. It is whether the company can preserve its dominance as hyperscalers build custom silicon and rivals push alternatives in networking and inference. NVIDIA still controls an estimated 80% to 85% of the AI chip market, supported by its CUDA software ecosystem, which keeps customers deeply tied to its hardware stack.

That moat matters. Alphabet, Amazon, Microsoft, and Meta are all spending aggressively on AI infrastructure, but several are also developing in-house chips to lower dependence on NVIDIA. At the same time, Broadcom is pressing its case in custom silicon and Ethernet networking, while Google’s TPUs are increasingly viewed as credible competition for certain workloads.

Still, NVIDIA is broadening the fight. Management continues to push complete AI factories, networking, optical connectivity, and future platforms such as Vera Rubin. That helps explain why many investors still see the company as more than a GPU story, even if pricing pressure and market-share questions are likely to stay front and center through 2026.

What are analysts saying on NVIDIA?

Analyst sentiment remains broadly constructive. Craig-Hallum reiterated a Buy rating on NVIDIA, and broader Wall Street consensus remains firmly bullish. That tone has been echoed across the AI ecosystem, where suppliers and infrastructure partners also rallied on the strength of NVIDIA’s outlook.

Dell, for example, jumped sharply on Friday as investors embraced its AI Factory strategy with NVIDIA. StocksToTrade highlighted fresh optimism around enterprise AI servers and noted bullish target increases from Mizuho, JPMorgan, and Citigroup. Elsewhere, MarketBeat pointed to continued institutional interest in NVIDIA after the company’s earnings beat, buyback expansion, and dividend increase.

There are also new use cases expanding beyond cloud data centers. Seeking Alpha reported that Kawasaki Heavy Industries is teaming up with NVIDIA, Microsoft, and others on physical AI applications, extending the company’s reach into robotics and industrial deployment. That wider adoption story is one reason investors continue to tolerate a premium valuation despite competitive concerns.

What should investors watch next?

The next major test is whether demand keeps outrunning expectations. NVIDIA’s commentary suggests AI spending is still accelerating globally, and the company is now selling full-stack systems into enterprises, sovereign AI projects, and industrial customers, not just hyperscalers. If that customer base broadens as management expects, the current growth cycle may have more room to run than skeptics assume.

Investors should also watch export-control risk after a report from Focus Taiwan on alleged smuggling of NVIDIA AI servers to Hong Kong, a reminder that China-related demand remains sensitive and difficult to model. Networking competition, custom chip adoption, and the pace of enterprise AI monetization will also shape how Wall Street values the stock from here.

Related Coverage: Investors looking for a deeper breakdown of the market’s mixed reaction can also read this analysis of NVIDIA Earnings, the record quarter, and the $80 billion buyback test. That piece explores why blockbuster numbers did not automatically translate into a bigger stock move and why China demand remains a closely watched swing factor.

NVIDIA Earnings confirmed that the company is still setting the pace in AI infrastructure, even as the stock cools after hours. For investors, the key question is no longer growth versus no growth, but whether NVIDIA can keep turning exceptional demand into upside that beats an already demanding valuation. If management’s $91 billion revenue outlook holds, the next quarter could quickly reset the debate in the bulls’ favor.

Fazit folgt.