Can NVIDIA Earnings still impress a market that now treats blockbuster growth as the bare minimum?

Why do NVIDIA Earnings matter so much?

NVIDIA Corporation has become the market’s clearest proxy for artificial intelligence spending, which is why this week’s NVIDIA Earnings report is being watched far beyond the semiconductor sector. The company reports Wednesday after the close, and the stakes are unusually high because AI-linked gains have driven a large share of the S&P 500 and NASDAQ advance. Reuters noted that investors are looking for another blockbuster update, but also questioning how long NVIDIA can preserve its dominance as inference workloads expand and competition broadens.

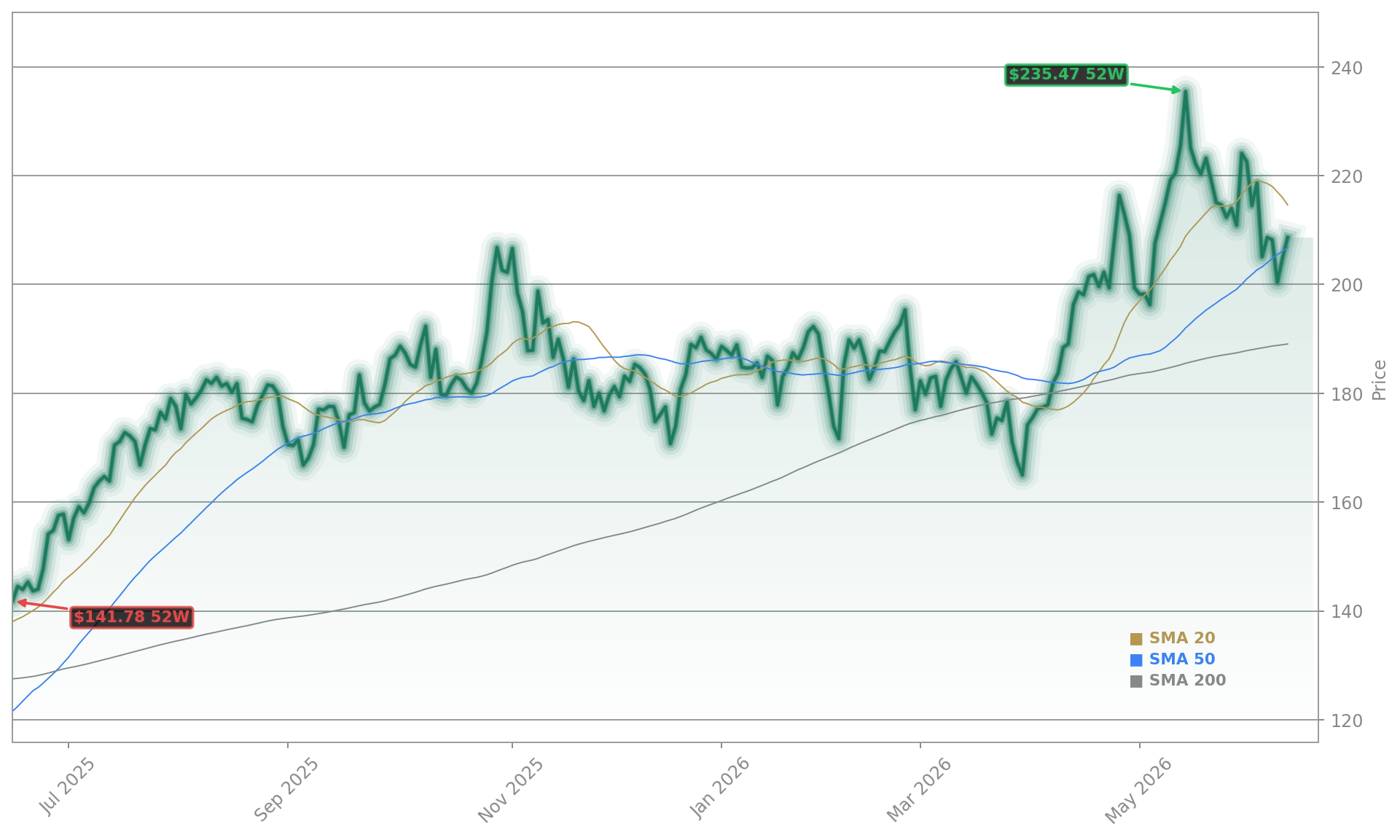

That pressure shows up in the stock’s setup. Even with the shares still near recent highs, traders know that strong results alone may not be enough if the outlook merely matches expectations. NVIDIA has beaten estimates repeatedly in prior quarters, yet the stock has often struggled immediately afterward because the bar kept rising.

Can NVIDIA defend its lead over Alphabet and AMD?

The core bull case remains intact: hyperscalers are still spending aggressively. Alphabet, Amazon, Microsoft, and Meta are expected to pour more than $700 billion into AI infrastructure this year, up sharply from 2025 levels. That spending continues to support demand for GPUs, networking, and full-stack systems tied to Blackwell and, later, Rubin.

Still, the competitive picture is changing. Alphabet is pushing tensor processing units more aggressively, and a reported partnership with Blackstone to build an AI cloud platform underscores the effort to reduce reliance on NVIDIA hardware. AMD and Intel are also targeting inference workloads, where cost and efficiency matter more than pure training performance. That does not mean NVIDIA is losing its lead, but it does mean Wall Street wants proof that its ecosystem advantage remains durable as the AI market broadens.

What are analysts expecting from NVIDIA?

Analyst expectations remain bullish heading into NVIDIA Earnings. RBC Capital kept an Outperform rating and a $250 price target, arguing that AI compute demand still exceeds supply and that results plus guidance could follow the familiar beat-and-raise pattern. TD Cowen lifted its target to $275 from $235 and kept a Buy rating, citing rising AI infrastructure spending and a larger long-term data center silicon opportunity.

UBS also raised its target to $275 and expects roughly $81 billion in April-quarter revenue with July-quarter guidance around $90 billion to $91 billion, helped by Blackwell demand and an eventual Rubin rack ramp. Morgan Stanley moved its target to $285 and continued to call NVIDIA its top semiconductor pick, while HSBC raised its target to $325 and expects another upside report. Not everyone is fully convinced: Seaport’s Jay Goldberg has a sell-equivalent view, arguing that supply limits and extreme expectations could cap upside.

How big is the China risk for NVIDIA?

China remains the main strategic wildcard in NVIDIA Earnings. Chief executive Jensen Huang recently said he believes the Chinese market will eventually reopen to U.S. AI chips, but investors did not treat those comments as a near-term solution. NVIDIA has described China as a potentially large long-term opportunity, yet several investors now model little or no immediate contribution from that market.

The other issue is sentiment. The broader chip group has shown signs of fatigue, memory names have sold off sharply, and concentrated AI positioning means any disappointment could ripple quickly through peers including Apple, Tesla, and the wider megacap complex.

Related Coverage: We recently examined the market’s growing sensitivity to this setup in NVIDIA Earnings -4.4% Plunge: AI Rally at Risk?. That analysis highlighted the same core issue facing investors now: a great quarter may not be enough unless NVIDIA also reinforces confidence in the trillion-dollar AI buildout and the next product cycle.

The demand in China is so incredible. With time, the market will open.— Jensen Huang

For investors, NVIDIA Earnings are about much more than one quarter. They will test whether demand for AI infrastructure, pricing power, and the Blackwell-to-Rubin roadmap can keep justifying NVIDIA’s central place in global portfolios. If management delivers on growth and guidance again, NVIDIA Earnings could reset the narrative higher and keep the AI trade firmly in control.