Can AMD AI Strategy turn a sharp pullback into a fresh opportunity as MI450 momentum and big-name partnerships build?

Why is AMD AI Strategy driving attention?

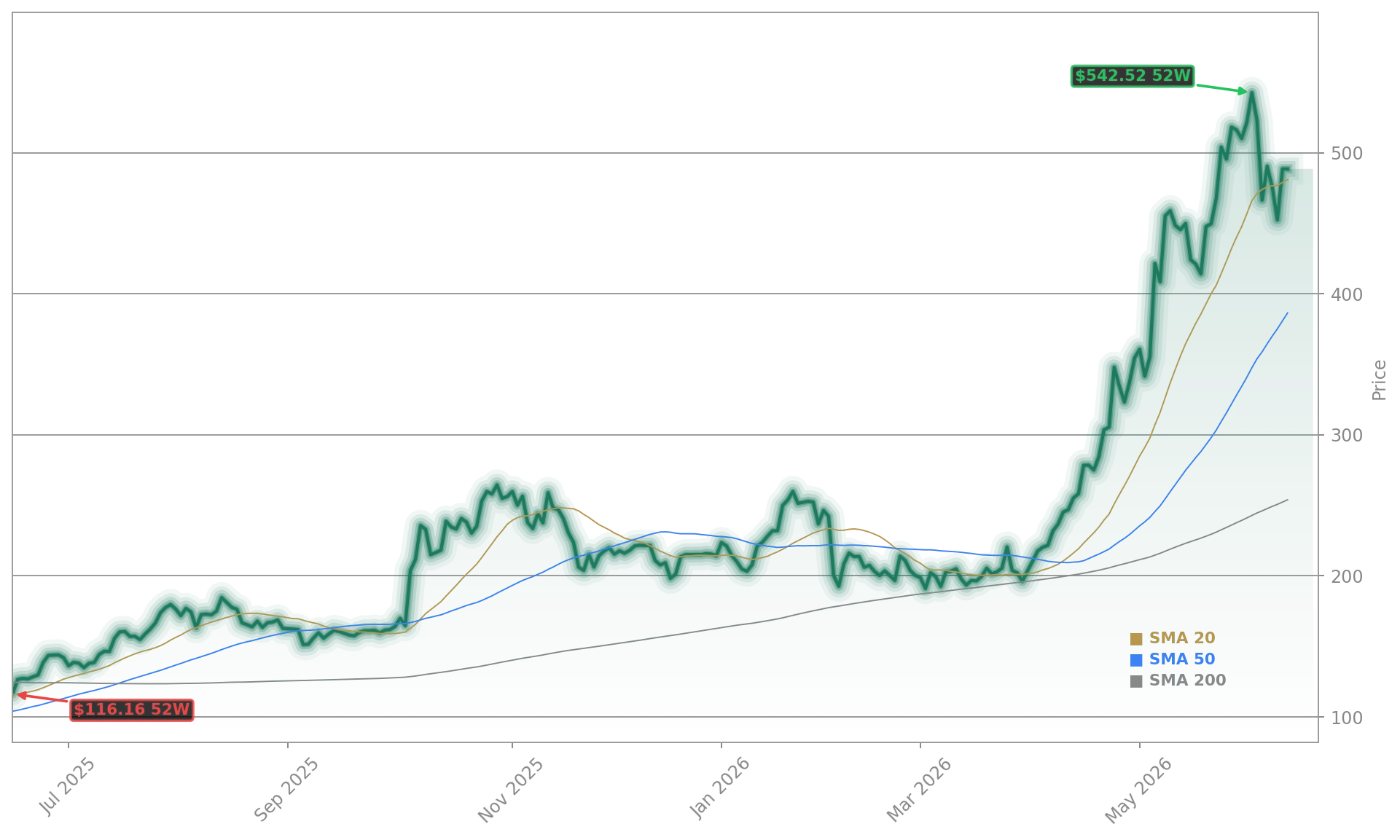

The latest selloff looks more like consolidation than a break in the broader thesis. AMD has been one of 2026’s standout chip names, helped by a blockbuster Q1 report and rising expectations for its MI450 accelerator family. Revenue reached $10.25 billion in Q1 2026, up roughly 38% year over year, while non-GAAP EPS came in at $1.37. Data Center revenue jumped 57% to $5.78 billion, reinforcing the view that AMD is becoming a more relevant AI infrastructure supplier alongside NVIDIA.

The stock is now below recent highs near the upper $450s, so this is not a new high claim. Instead, investors are reassessing valuation after a huge run and a broader cooldown in chip stocks. The Philadelphia Semiconductor Index also fell sharply, showing that AMD’s intraday weakness is part of a wider sector move rather than a company-specific collapse.

Can AMD challenge NVIDIA more directly?

The AMD AI Strategy increasingly rests on MI450. Management said production of MI450 GPUs will ramp in the second half of 2026, using TSMC’s 2-nanometer process technology. Lisa Su also said demand continues to strengthen, with lead customer forecasts running above initial plans and more customers engaging in large-scale deployments. That matters because AMD is trying to narrow the gap with NVIDIA in high-end AI compute, where Nvidia still controls the majority of the accelerator market.

AMD’s opportunity is not just product performance, but supply diversification. Some customers still want alternatives when Nvidia systems are constrained or fully allocated. Seaport’s Jay Goldberg recently argued that MI450 looks fully competitive on paper, a notable shift in sentiment for a market that had long seen AMD as a secondary option. At the same time, competition remains fierce, and hyperscalers are also designing more custom chips internally.

What do partnerships say about AMD?

Partnerships are a major pillar of the AMD AI Strategy. AMD has outlined deployments with OpenAI and Meta beginning in the second half of 2026, including large-scale GPU opportunities that could materially expand data center AI revenue. In enterprise infrastructure, Rackspace and AMD recently unveiled a multiyear framework to build a managed Enterprise AI Cloud for regulated and sovereign workloads, integrating AMD Instinct GPUs and EPYC CPUs into governed AI stacks.

Those announcements broaden AMD’s story beyond raw silicon. They show the company trying to capture more of the enterprise AI stack, especially where security, sovereignty, and managed services matter. AMD is also tied into the broader AI hardware ecosystem through TSMC, whose latest quarterly figures benefited from demand tied to both AMD and NVIDIA. Even Apple and other major silicon players remain part of the same advanced manufacturing pipeline, underscoring how central foundry access has become.

How are analysts and investors reacting?

Wall Street remains constructive, but not universally bullish. Citigroup recently lifted its AMD price target to $460 from $358 while keeping a Neutral rating, citing upside from the emerging AI CPU total addressable market. MarketBeat-listed analyst data still points to a Moderate Buy consensus, with an average target around $404.03. That leaves AMD trading slightly above the broader consensus even after today’s retreat.

Institutional appetite remains solid. New and expanded positions were disclosed by investors including Tredje AP fonden, Capstone Capital Management, and AMF Tjanstepension AB. Still, caution is visible too: ARK funds sold AMD shares on May 18, and some market watchers have warned that semiconductor leaders look technically stretched after outsized gains. Related Coverage: Investors following today’s weakness may also want to read AMD AI Strategy: -5.4% Plunge Tests Big AI Bet, which examines whether the recent selloff changes the long-term AI thesis. That piece adds context on valuation pressure and profit-taking just as AMD’s AI ambitions are accelerating.

Demand for MI450 series GPUs continues to strengthen, with lead customer forecasts now exceeding our initial plans.— Lisa Su

The bottom line is that the AMD AI Strategy remains intact despite intraday volatility. Strong Q1 execution, MI450 momentum, and expanding partnerships keep AMD firmly in the AI race. For investors, the next big test is whether second-half production and customer deployments convert hype into sustained revenue acceleration.