Is the AMD AI Strategy strong enough to justify a soaring valuation just as the stock suddenly drops and profit-taking accelerates?

Is Wall Street chasing AMD too far, too fast?

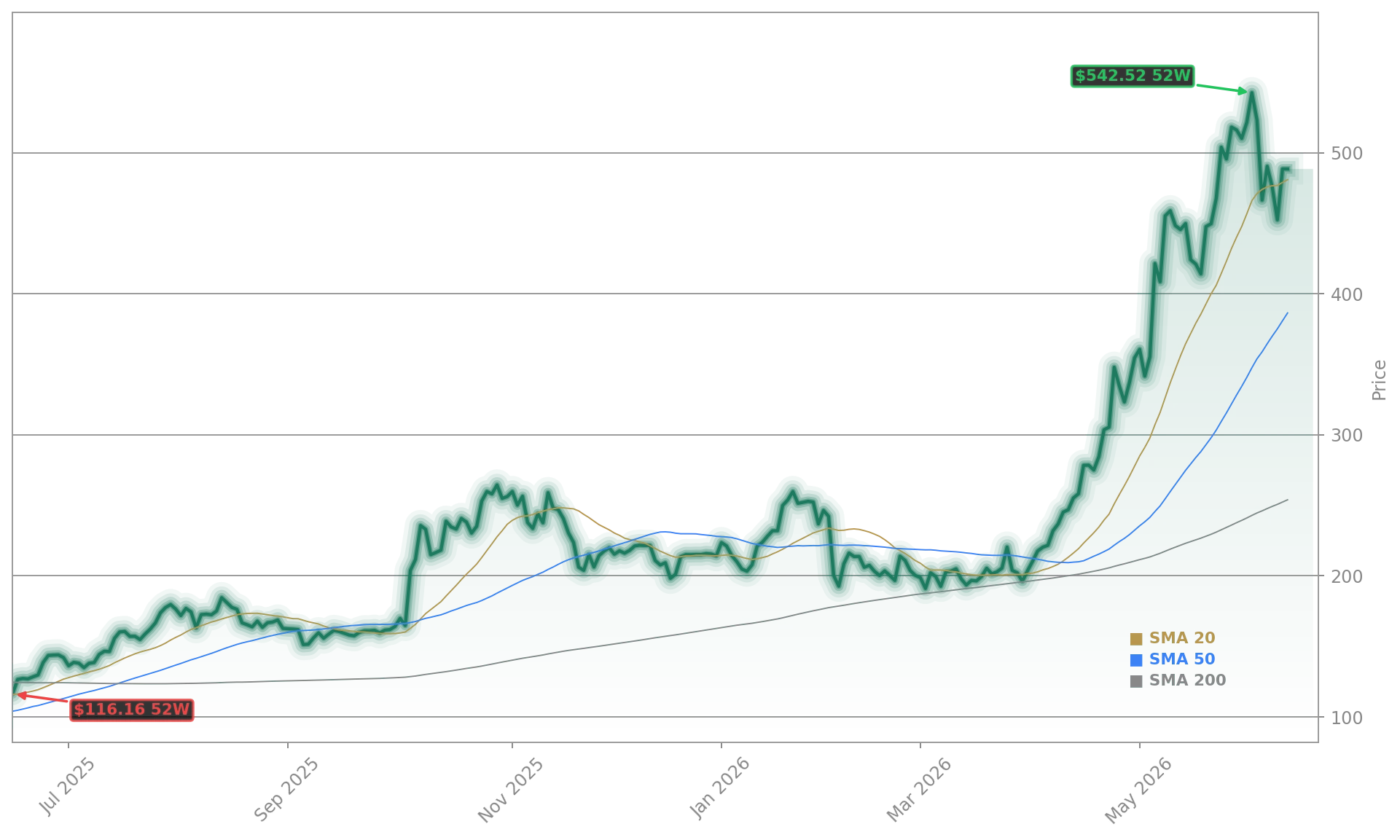

After a spectacular 12‑month run that saw AMD nearly triple and hit a 52‑week high of $469.22, today’s intraday drop highlights how sensitive AI leaders have become to profit‑taking. Semiconductor names from Intel and Qualcomm to AMD are pulling back more than 3% alongside the PHLX Semiconductor Index, as investors react to sticky inflation data and warnings from some strategists that AI chip stocks look technically overextended.

At roughly $398, AMD still sits well above the average Wall Street target near $404 cited in recent institutional ownership reports, leaving valuation front and center. The stock trades on rich earnings and EV/EBITDA multiples that assume AMD’s AI accelerator and server CPU businesses will keep scaling rapidly through the decade. Any stumble in execution around its AMD AI Strategy, especially in data center, could invite a deeper derating.

Some active managers are already locking in gains. ARK Invest’s Cathie Wood sold over $16 million of AMD across several ETFs on May 18, rotating capital toward defense contractor L3Harris and Amazon. At the same time, a wave of pension funds and asset managers has been adding to positions, suggesting a hand‑off from fast money to longer‑term holders rather than a full‑blown exodus from the name.

How central are MI450 GPUs to AMD AI Strategy?

The core of AMD AI Strategy is the MI450 accelerator platform aimed squarely at NVIDIA’s data center dominance. Built on Taiwan Semiconductor Manufacturing’s cutting‑edge 2‑nanometer process, MI450 is designed for large language models and generative AI workloads that currently favor NVIDIA’s H100 and B100 lines. AMD plans to ramp MI450 production in the second half of 2026, timing that lines up with the next big capital‑spending wave from cloud hyperscalers.

On its latest earnings call, CEO Lisa Su highlighted that demand for MI450 series GPUs is strengthening, with lead customer forecasts already surpassing initial production plans. AMD is now working on large‑scale deployments with OpenAI and Meta Platforms, both tied to multi‑gigawatt AI infrastructure commitments that could translate into tens of billions of dollars in annual data center AI revenue by 2027 if execution holds. Su also sees the overall server CPU total addressable market growing more than 35% annually through 2030, reinforcing a thesis that AMD’s data center segment can outgrow the broader PC and gaming markets for years.

Even so, AMD’s current accelerator share is still estimated around 10%, with NVIDIA controlling roughly 80% of the AI GPU market. Hyperscalers from Apple and Google to Amazon are also designing more custom silicon, adding another layer of competitive pressure. That makes MI450’s real‑world performance, ecosystem maturity, and software support critical tests for the credibility of AMD AI Strategy.

What does the Rackspace partnership change for AMD?

Beyond pure silicon, AMD AI Strategy is expanding into managed infrastructure through a multiyear framework with Rackspace Technology. The two companies plan to build an “Enterprise AI Cloud” aimed at regulated industries and sovereign workloads, integrating AMD Instinct GPUs and EPYC CPUs into a fully governed stack administered by Rackspace.

The goal is to offer enterprises a turnkey AI platform that spans bare‑metal compute, inference tooling, runtime governance, and compliance‑calibrated service‑level agreements – particularly attractive for financial services, healthcare, and public‑sector customers with strict data residency rules. BMO Capital Markets responded positively, lifting its price target on Rackspace from $2 to $5 and pointing to the AMD alliance as a cornerstone of Rackspace’s pivot toward higher‑value AI infrastructure services.

For AMD, the partnership provides an additional distribution channel beyond hyperscalers and on‑premises data centers, potentially smoothing demand and deepening its presence in sticky enterprise workloads. It also broadens the narrative from “chip vendor” to an enabling platform player in AI, a nuance that could matter for valuation if the strategy gains traction.

How strong is AMD’s financial and investor backing?

Fundamentally, AMD enters this next AI investment cycle from a position of growing strength. Q1 2026 revenue climbed to $10.25 billion, up nearly 38% year over year, with non‑GAAP EPS of $1.37 and data center revenue surging 57% to $5.78 billion. Gross margins have expanded toward the 70% zone, reflecting the higher mix of AI and server products and putting AMD more in line with premium peers such as NVIDIA and TSMC.

Institutional confidence remains robust. Swedish fund Tredje AP fonden boosted its AMD stake by more than 60% in Q4 to roughly $37.8 million, while AMF Tjanstepension AB and Capstone Capital Management both initiated new positions. In parallel, AMD has secured a new $5 billion unsecured revolving credit facility and expanded its commercial paper program to $5.5 billion, giving it ample liquidity for working capital, capex, or opportunistic M&A tied to its AMD AI Strategy.

On the market‑structure side, AMD’s inclusion in Tuttle Capital’s planned “Magnificent 10” ETF underscores its status as a core AI hardware play for thematic portfolios. The fund aims to broaden the original “Magnificent 7” concept by adding AMD, Broadcom, and Palantir, cementing AMD’s role in options‑driven income strategies and structured products linked to large‑cap AI winners.

Related Coverage

Investors looking for a deeper dive into data center dynamics can read AMD AI Infrastructure Boom Tests Data Center Valuation, which examines whether AMD’s explosive AI infrastructure growth can justify its premium multiple versus rivals like NVIDIA and Intel. That piece complements the current focus on AMD AI Strategy by analyzing how hyperscale commitments and accelerator share might translate into long‑term earnings power and stock performance.

In summary, AMD AI Strategy is shifting into a higher gear with MI450 accelerators, a targeted Rackspace enterprise cloud, and multi‑gigawatt commitments from marquee AI customers, even as the stock endures a valuation‑driven shakeout. For U.S. investors, today’s pullback reflects short‑term technical exhaustion rather than a change in the multiyear AI infrastructure thesis anchored in data center growth and robust institutional support. The next few quarters of MI450 progress, enterprise traction, and margin execution will determine whether AMD AI Strategy can turn volatility into an opportunity and keep the stock on a path toward its most bullish long‑term targets.