Are Riot Platforms insider moves a quiet warning sign, or just tax-driven noise before the company’s AI data center bet scales up?

What Do Recent Riot Platforms Insider Transactions Signal?

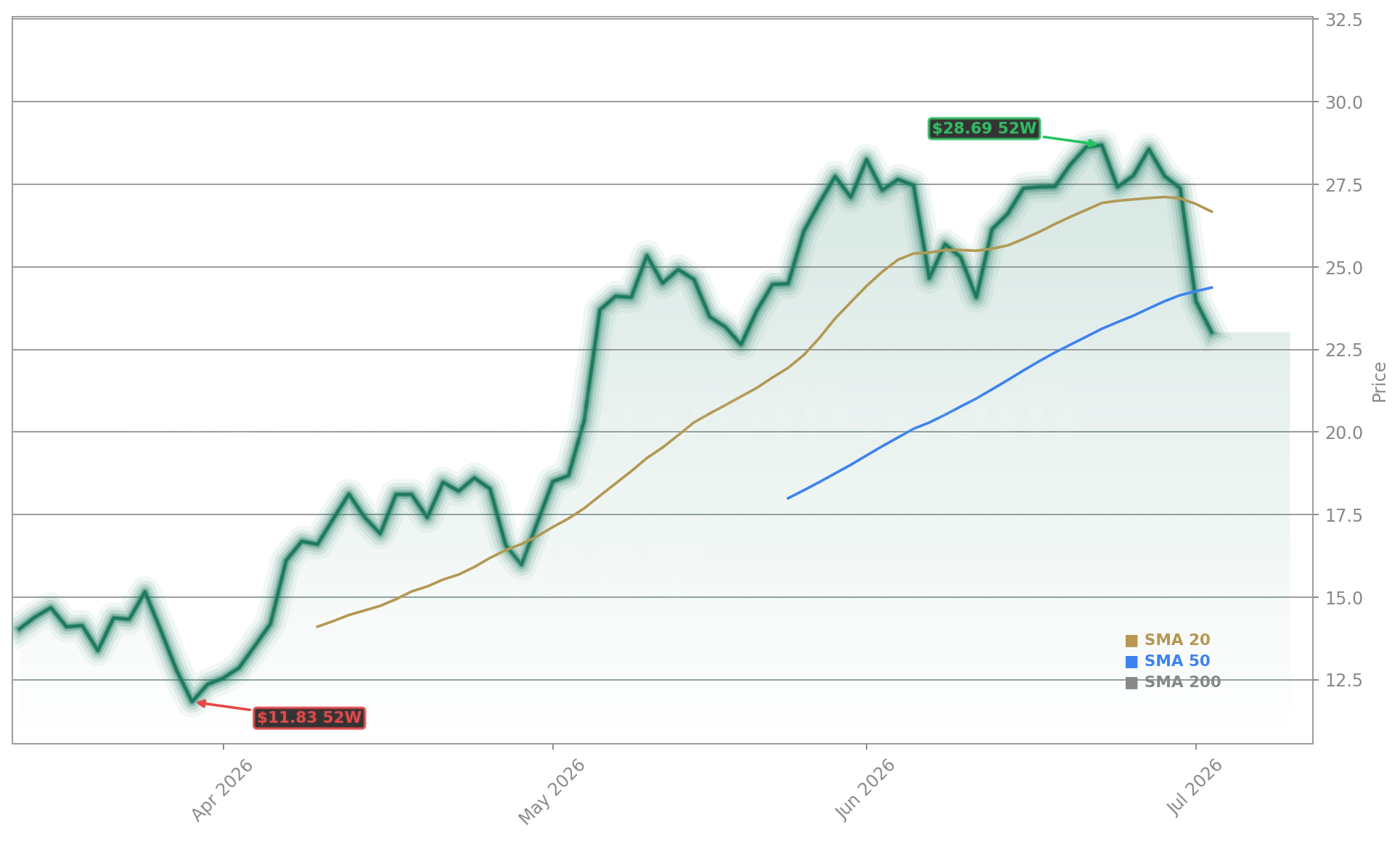

Riot Platforms Insider Transactions surged last week as top executives surrendered shares to cover tax liabilities tied to equity vesting — not open-market sales. CEO Les Jason surrendered 101,015 shares valued at $2.42 million, COO Stephen Howell Jr. surrendered 21,966 shares ($526,305), and VP Werner Ryan D surrendered 13,869 shares ($332,301), all at $23.96 per share. Unlike recent Rule 10b5-1 sales — including Jason’s $1.8M sell on June 22 — these were non-market, tax-related surrenders reported via SEC Form 4. The moves underscore ongoing executive alignment with Riot Platforms, Inc.’s capital-intensive transformation, not a retreat from its AI data center roadmap.

How Does Riot Platforms Compare to Hut 8 and Marathon Digital?

Riot Platforms, Inc. stands apart from peers like Hut 8 Corp and Marathon Digital Holdings (MARA) through vertical integration and its 10-year, 50 MW data center agreement with Advanced Micro Devices. While Hut 8 trades at a forward P/E of 84.8x and Marathon Digital leans heavily on Bitcoin price exposure, Riot Platforms trades at just 20.9x forward P/E — 21% below the sector benchmark — and a P/S ratio of 11.7x versus Hut 8’s 36.7x. Its $900 million Bitcoin treasury remains a strategic liquidity source, but unlike Hut 8, Riot Platforms does not consolidate a separately traded Bitcoin subsidiary — simplifying its financial narrative for NASDAQ investors. That clarity helped drive its recent inclusion in the Russell 2500 Growth Benchmark.

Is the AI Pivot Generating Real Revenue Yet?

Yes — but selectively. Riot Platforms, Inc. reported $167.22 million in Q1 2026 revenue (ended March 31), with its first material AI infrastructure revenue recognized under the AMD agreement. Though GAAP net loss totaled $500.48 million for the quarter — driven by $774.3 million in negative free cash flow from data center buildout — Bernstein reaffirmed its Buy rating with a $30.00 price target, citing ‘de-risked execution’ on the Rockdale campus. BTIG echoed that view, assigning a $40.00 target and highlighting Riot Platforms’ proximity to baseload nuclear power via its Terrestrial Energy collaboration — a key advantage over competitors like Tesla and Apple in energy-cost-sensitive HPC deployments.

What Are the Key Risks for U.S. Portfolio Managers?

Riot Platforms is no longer a Bitcoin miner with data centers — it’s a digital infrastructure company with strategic Bitcoin reserves.— Gautam Chhugani, Bernstein Analyst

Three structural risks stand out: first, ongoing litigation with Green Revolution Cooling over proprietary immersion cooling tech could delay data center deployments; second, ERCOT regulatory curtailment risk remains acute in Texas, where Riot Platforms operates 70% of its capacity; and third, Bitcoin price volatility still accounts for ~65% of quarterly GAAP earnings variance. Yet, with a conservative 0.3x debt-to-equity ratio and $900 million in Bitcoin-backed liquidity, Riot Platforms, Inc. maintains stronger balance sheet flexibility than Hut 8 or Marathon Digital. For S&P 500 and NASDAQ investors seeking AI infrastructure exposure with embedded crypto optionality, Riot Platforms Insider Transactions are not red flags — they’re tax-efficient milestones in a $500M+ infrastructure transition.