Can Novo Nordisk Competition derail the obesity leader’s comeback before oral Wegovy and Medicare access have a chance to matter?

Is Novo Nordisk Competition Reshaping Obesity Market Leadership?

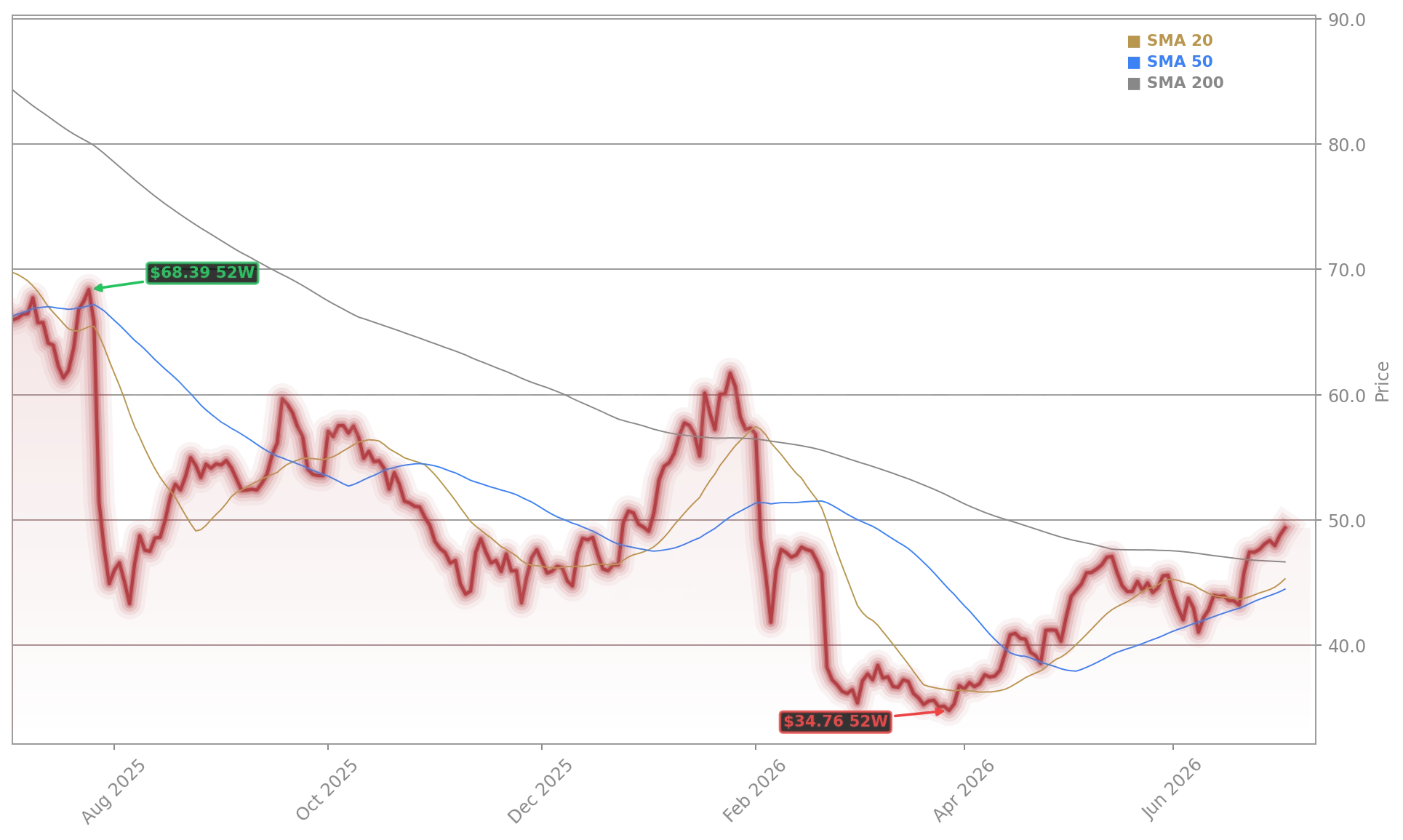

Novo Nordisk A/S slid 2.28% to $49.28 on Monday, July 6, 2026, extending a two-day decline and widening the gap to its July 2025 52-week high of $150.32 (converted from DKK464.60). While the stock remains up 14% year-to-date, the recent pullback reflects deeper structural concerns: Eli Lilly (LLY) now commands over 42% of new GLP-1 prescriptions in the U.S., per IQVIA data, up from 31% in Q4 2025 — a gain directly tied to Mounjaro’s broader label expansion and aggressive payer negotiations. Meanwhile, Teva’s FDA-approved generic version of liraglutide (marketed as Saxenda) is already appearing in formularies for commercial plans with $10–$25 co-pays, pressuring Novo Nordisk A/S’s pricing power in the lower-tier obesity segment. This intensifying Novo Nordisk Competition is no longer theoretical — it’s showing up in quarterly script trends, Medicare Part D access metrics, and Wall Street’s revised 2026 earnings estimates.

Why Is Novo Nordisk A/S Cutting Supplier Costs Now?

Seeking Alpha reports that Novo Nordisk A/S is actively seeking discounts from raw material and packaging suppliers — a clear signal of margin pressure amid rising competition. The move comes as the company’s gross margin dipped to 82.1% in Q2 2026, down 110 basis points year-over-year, per internal financial disclosures. Unlike Apple or NVIDIA, whose pricing power is reinforced by hardware-software ecosystems, Novo Nordisk A/S operates in a rapidly commoditizing biologics space where payer leverage and biosimilar threats are accelerating. Citigroup analysts noted in a July 3 report that ‘Novo Nordisk A/S’s cost discipline is necessary but insufficient without differentiated clinical outcomes — especially as Lilly’s tirzepatide data shows superior weight loss in head-to-head trials.’ This supplier push underscores how Novo Nordisk Competition is forcing operational recalibration, not just marketing shifts.

Does the $15 Billion Buyback Signal Confidence — or Concern?

Despite the volatility, Novo Nordisk A/S continues executing its DKK 15 billion share repurchase program — having acquired over 23 million B shares since February 4, 2026, lifting treasury holdings to 0.9% of total share capital. TipRanks’ Spark AI Analyst maintains an ‘Outperform’ rating, citing ‘strong financial quality and supportive valuation’ — but adds that ‘near-term headwinds from pricing pressure and regulatory scrutiny remain material.’ The buyback, while bullish in intent, coincides with unusually high put option volume (Barchart.com), particularly for July 17 expirations — suggesting some institutional investors are hedging against further downside. For U.S. portfolios holding Novo Nordisk A/S as a healthcare diversifier, this isn’t just a liquidity play — it’s a strategic signal that management views current valuations as compelling *despite* Novo Nordisk Competition.

Can Oral Wegovy and Medicare Access Reverse the Momentum?

Seeking Alpha’s July 4 bullish thesis hinges on oral Wegovy’s U.S. launch and pending Medicare Part D expansion — both expected to drive 2026 revenue guidance upward by 5–7%. The oral formulation unlocks ~18 million U.S. patients previously excluded due to injection anxiety or access barriers. Yet RBC Capital Markets cautions that ‘Medicare’s final 2026 formulary decisions — due August 15 — will determine whether Novo Nordisk A/S regains prescription share or cedes further ground to Lilly’s dual-GLP-1/GIP agent. The window is narrow.’ Meanwhile, Tesla and Meta aren’t relevant here — but the parallel is instructive: just as AI chip demand reshaped NVIDIA’s valuation, GLP-1 adoption curves are now rewiring pharma’s entire growth calculus. Novo Nordisk Competition isn’t just about molecules — it’s about speed to market, payer influence, and digital health integration (e.g., Hims & Hers, highlighted as a ‘voluminous’ telehealth partner).

Is Novo Nordisk A/S Trading Below Fair Value?

Novo Nordisk A/S’s cost discipline is necessary but insufficient without differentiated clinical outcomes — especially as Lilly’s tirzepatide data shows superior weight loss in head-to-head trials.— Citigroup analysts, July 3, 2026

Simply Wall Street’s analysis concludes NVO is trading below intrinsic value — a 36% discount to fair value per DCF and P/E comparisons — but notes that ‘the discount likely prices in real Novo Nordisk Competition risk.’ With Eli Lilly’s pipeline advancing toward once-weekly oral tirzepatide and Akero Therapeutics’ non-GLP-1 NASH assets now under Novo Nordisk A/S’s umbrella, the competitive moat is evolving. Goldman Sachs maintains a $68 price target, citing ‘long-term obesity market expansion outweighing near-term share volatility.’ Still, investors must weigh whether current valuations adequately compensate for execution risk in a market where no single player holds a durable monopoly.