Can Apple secure cheaper memory from China without triggering a political backlash that reshapes its entire iPhone supply chain?

Why Is Apple Pursuing Apple Memory Chips From China?

Apple Inc. is actively negotiating with Chinese memory manufacturers CXMT and YMTC — both on the U.S. Department of Defense blacklist — to secure LPDDR5X and NAND chips for iPhones sold exclusively in China. The move responds to a ‘100-year flood’ in memory pricing, as Tim Cook described it, driven by AI infrastructure demand siphoning supply from consumer electronics. With only three approved global suppliers — Samsung, SK Hynix, and Micron — Apple is pushing to expand its vendor base to five. Crucially, Apple insists chips sourced from China would not enter U.S.-bound devices, a concession intended to ease national security concerns in Washington. Still, House Foreign Relations Committee leadership has called the proposal a ‘no-go,’ signaling intense regulatory friction ahead.

How Does This Affect Apple’s iPhone 18 Launch?

Despite the memory crunch, Apple Inc. is doubling down on premium hardware — planning at least five new iPhone models for late 2026 and early 2027, including a foldable iPhone targeting 10 million units. Nikkei Asia reports Apple has already reserved components for 80 million iPhone Pro and Pro Max units in H2 2026, with some suppliers forecasting up to 85 million orders. This aggressive rollout contrasts sharply with Xiaomi, Oppo, and Vivo — all slashing production by up to 30% amid the same shortage. Apple’s pricing power lets it absorb cost shocks: it recently raised iPad and Mac prices by $100, and iPhone 18 could jump $150–$200. Analysts at Bank of America Securities maintain a Buy rating and $380 price target, citing services growth, AI monetization, and new product optionality as key upside drivers.

What’s Wall Street’s Reaction to the Memory Strategy?

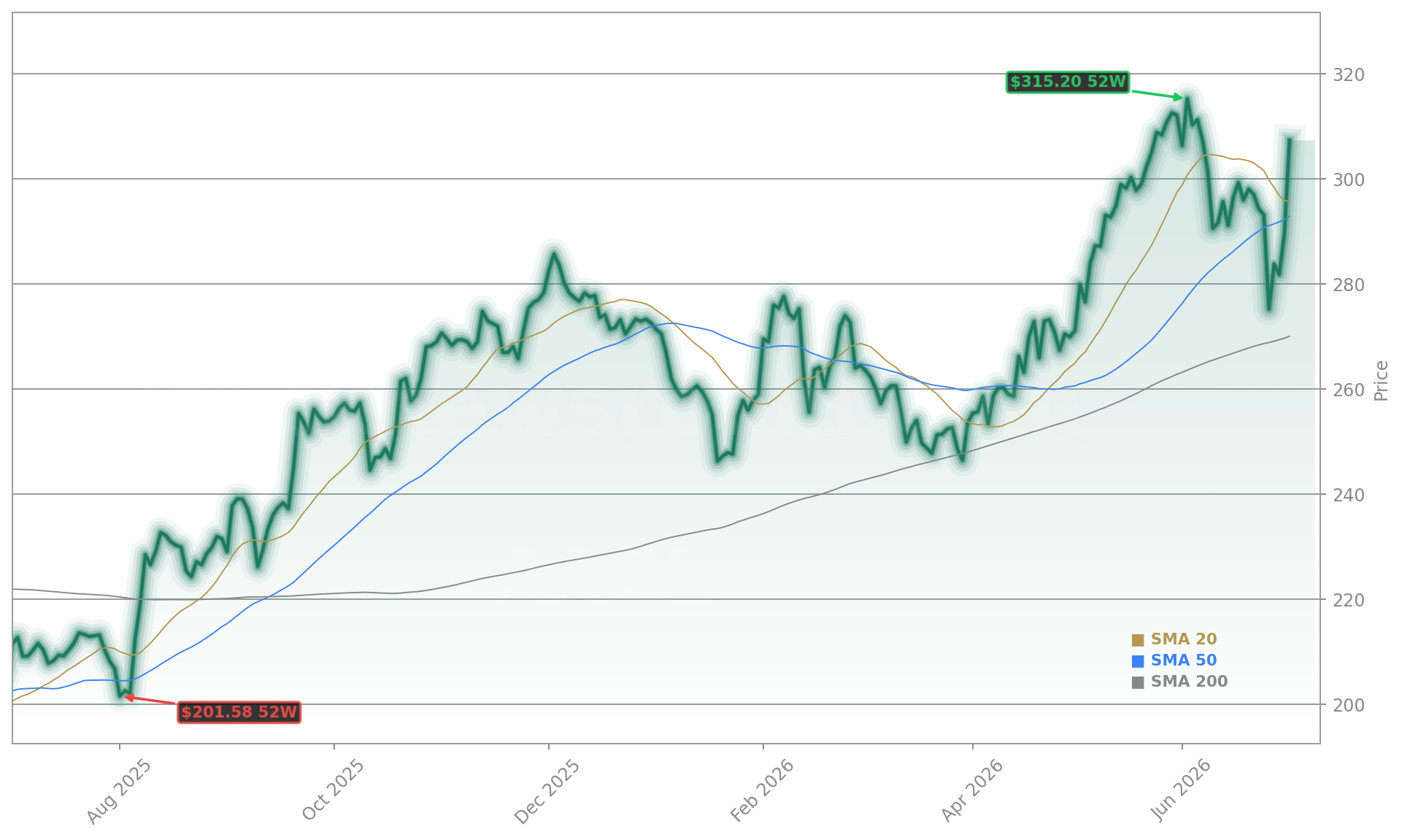

Apple shares surged 4.52% to $307.33 on Thursday — outperforming a sharply weaker Nasdaq (-1.63%) and S&P 500 (-0.27%). The rally marks Apple’s strongest three-day stretch since August 2025 and lifts it 13.3% year-to-date. While the Magnificent Seven collectively underperformed semiconductor stocks in June, Apple bucked the trend — rising 8.5% over four sessions. Citigroup analysts highlight Apple’s ‘structural resilience,’ noting its $30.98 billion Services quarter — an all-time record — insulates it from hardware volatility. Meanwhile, KGI Securities downgraded Apple to Hold with a $315 price target on June 22, citing margin pressure from rising memory costs and App Store litigation risk. Evercore ISI maintains an Outperform rating and $365 target, emphasizing ecosystem stickiness and AI edge deployment.

How Do Competitors Fit Into the Memory Squeeze?

While Apple negotiates with Chinese chipmakers, NVIDIA and Tesla benefit from the same AI-driven memory boom — but in opposite directions. NVIDIA’s data center revenue soared on DRAM and HBM demand, lifting its stock 170% since its DRAM ETF launch. Tesla, however, faces headwinds: its Q2 delivery beat masked a -6.7% YoY delivery decline, prompting investor skepticism about demand sustainability. Meanwhile, Micron — whose $12 billion mobile memory segment is directly threatened by Apple’s CXMT talks — saw shares fall sharply alongside SanDisk and Western Digital as pricing assumptions unraveled. TSMC remains Apple’s linchpin foundry partner, manufacturing A-series and M-series chips, but it does not produce memory — leaving Apple exposed to the very supply chain it now seeks to rewire. The State Street Technology Select Sector SPDR ETF, holding Apple at 11.6%, reflects how tightly Apple’s fate remains tied to semiconductor dynamics — even as it tries to bypass them.

What’s Next for Apple Memory Chips and Investor Strategy?

Apple’s memory strategy is not just tactical — it’s a signal of shifting global tech sovereignty. If approved, sourcing Apple Memory Chips from China would mark the first major U.S. tech firm to integrate blacklisted suppliers into its supply chain under strict geographic partitioning. The Supreme Court’s upcoming App Store ruling adds another layer of uncertainty, with analysts projecting a potential 2–3% gross margin impact if the 27% commission is curtailed. Yet Apple’s $100 billion buyback authorization and 4% dividend hike reinforce its capital return strength. For U.S. portfolios, Apple remains a core S&P 500 and NASDAQ hedge — but one increasingly defined by geopolitical navigation, not just product cycles. The next major catalyst arrives July 30, when Apple reports Q3 FY26 earnings — with Wall Street expecting $108.86 billion in revenue and $1.89 EPS.

Related Coverage: Apple’s legal battle over App Store economics gained new urgency as the Supreme Court agreed to hear its appeal — a case that could reshape Services profitability. Apple App Store Dispute +2.1% as Supreme Court Hears Appeal. Meanwhile, Tesla’s delivery numbers illustrate how headline beats can mask structural weakness — a cautionary parallel for investors weighing Apple’s hardware momentum against margin risks. Tesla Deliveries -6.7% Despite Massive Q2 Delivery Beat.

We’re fighting through what I’d call a ‘100-year flood’ in memory pricing — and we need solutions that protect our customers and our margins.— Tim Cook, CEO of Apple Inc.

Apple Memory Chips represent more than a cost-cutting tactic — they’re a test of Apple’s ability to balance innovation, scale, and sovereignty. For U.S. investors, the stakes extend beyond margins to supply chain control in an era of tech decoupling. The next quarterly earnings will show whether Apple’s dual-track strategy — premium hardware launches and pragmatic memory sourcing — delivers both growth and resilience. For long-term portfolios, Apple remains a critical exposure to both AI adoption and global tech governance.