If Tesla Deliveries crushed expectations, why did the stock still tumble as investors looked past the headline win?

What Do Tesla Deliveries Mean for S&P 500 Tech Exposure?

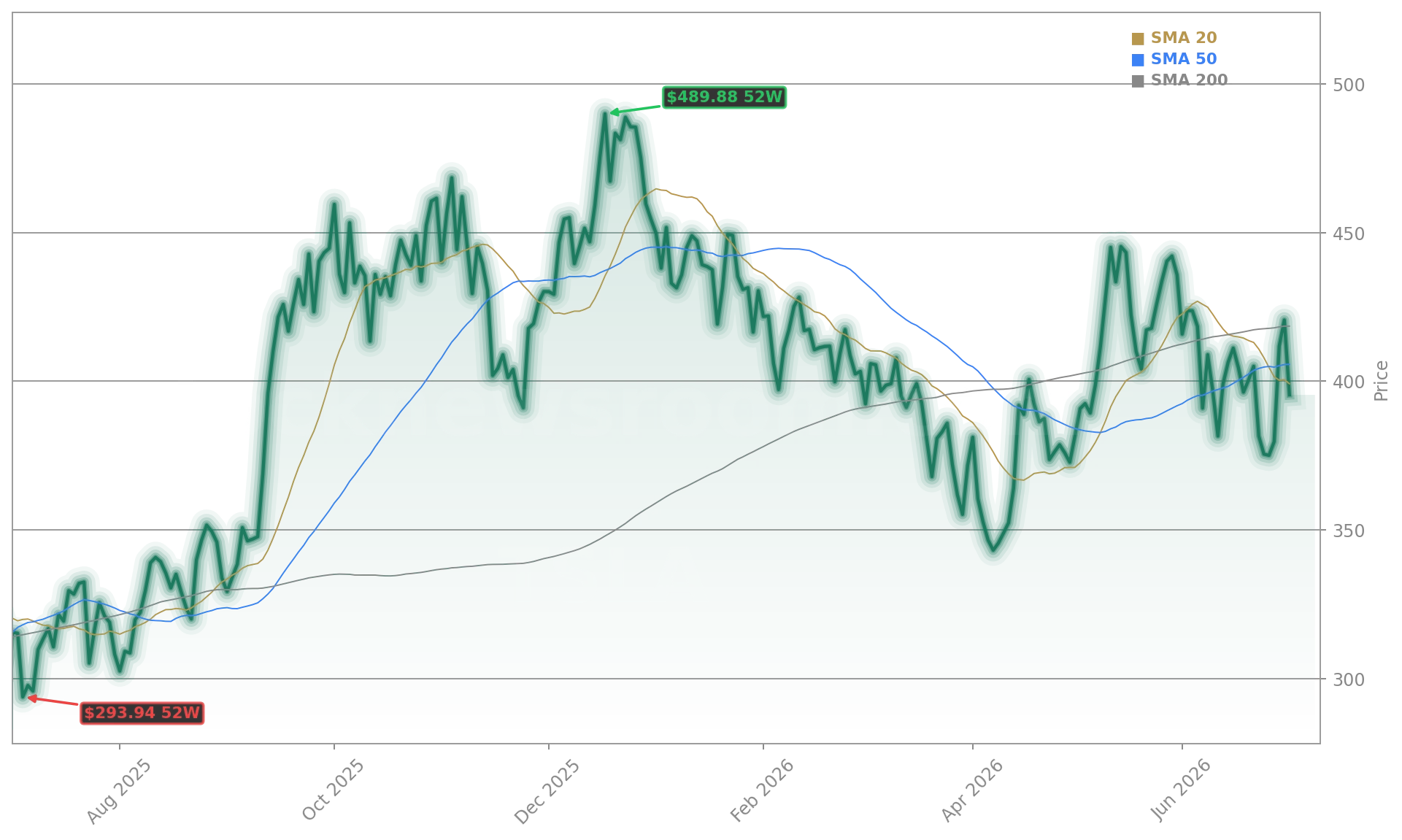

Tesla Deliveries for Q2 2026 landed at 480,126 — shattering Bloomberg’s consensus of 396,466 and FactSet’s 401,000. The 25% YoY gain reverses two straight years of annual delivery declines and marks Tesla’s fourth-best quarter ever. Crucially, deliveries exceeded production (451,758 units) by 28,000, signaling meaningful inventory drawdown — a positive signal for pricing power and channel health. Yet Tesla (TSLA) shares dropped 6.68% to $396.43 — underscoring how deeply Wall Street has decoupled from auto fundamentals. With the Magnificent Seven down double digits from 52-week highs and retail participation at a four-year low (just 6% of trading volume), Tesla Deliveries now serve less as a catalyst and more as a stress test for investor patience. The NASDAQ’s 12% YTD gain contrasts sharply with Tesla’s -5% year-to-date performance — a widening gap that reflects divergent narratives: hardware execution vs. AI monetization.

Why Did Tesla Deliveries Soar in Europe but Stall in the U.S.?

European registrations surged — up 77% in the EU’s first five months — driven by record fuel prices (peaking at $4.56/gallon in May), expanded Full Self-Driving (Supervised) availability in the Netherlands, Estonia, Greece, and Lithuania, and aggressive Model 3/Y pricing. In Germany, registrations jumped 300% in May; France doubled (+105%), Sweden rose 56%, and Denmark climbed 39%. Meanwhile, U.S. demand remains structurally impaired: the $7,500 federal EV tax credit expired in September 2025, and Cox Automotive projects a 20% drop in Tesla’s U.S. sales for 2026. Tesla’s pivot to hybrids — a segment it doesn’t serve — leaves it exposed while rivals like NVIDIA and Apple deepen AI integration in transportation ecosystems. Citigroup recently reiterated its ‘Neutral’ rating on Tesla, citing ‘valuation risk outweighing delivery momentum.’

How Do Tesla Deliveries Compare to BYD and Rivian?

While Tesla delivered 480,126 vehicles, BYD reported 557,090 battery-electric vehicles in Q2 — reclaiming the title of world’s top EV seller. BYD’s exports surged 94.7% YoY, with China sales down 22%, highlighting its global diversification advantage. Rivian, reporting Q2 deliveries alongside Tesla, posted a 14% jump to 22,800 units — buoyed by its new R2 platform — but trades at a fraction of Tesla’s multiple. RBC Capital Markets maintains its ‘Underperform’ rating on Tesla, noting ‘BYD’s cost leadership and Rivian’s product inflection create asymmetric pressure on margins.’ Tesla’s Model 3/Y accounted for 467,762 deliveries, while Cybertruck, Model S, and Model X combined for just 12,364 — a stark reminder that its future hinges on scaling new platforms, not legacy volume.

What’s Next for Tesla Deliveries Amid Robotaxis and Optimus?

Tesla’s delivery beat is operationally impressive, but investors are pricing in AI monetization — not auto volume. The stock’s sell-off confirms that narrative has shifted.— Al Root, Barron’s

Tesla’s delivery beat arrives as it shifts capital and attention toward AI infrastructure. The company confirmed mass production of its Cybercab and Optimus humanoid robots — with Musk sharing a group photo of the Fremont Optimus line going live. SpaceX’s $86 billion IPO war chest and the joint Terafab AI chip project with Intel signal a strategic pivot. Yet Wall Street remains skeptical: Wedbush’s Dan Ives recently noted Tesla’s ‘robotaxi narrative lacks scale — with only dozens operating in Texas — while NVIDIA’s data center GPUs power real AI revenue.’ Tesla’s energy business deployed 13.5 GWh of storage — up 40.6% YoY — and is now its fastest-growing segment. Still, vehicle sales represent ~75% of 2025 revenue. The next catalyst? Full financial results on July 22 — where gross margin, FSD revenue recognition, and Cybercab pre-orders will matter more than Tesla Deliveries alone.