Can Apple protect its App Store economics in court, or is a bigger hit to Services profits now coming into view?

What Does the Supreme Court’s Move Mean for Apple?

The Supreme Court’s acceptance of Apple’s petition marks the latest legal milestone in a dispute stretching back to 2020. As reported by Reuters, the justices will hear arguments during their October 2026 term on whether Apple violated a 2021 injunction requiring it to allow third-party payment links in iOS apps. After Apple implemented a 27% commission on external purchases made within seven days of clicking such links, U.S. District Judge Yvonne Gonzalez Rogers found the company in civil contempt in 2025 — a ruling upheld by the Ninth Circuit in December. Apple argues the injunction was never intended to bind millions of developers beyond Epic, while regulators globally await the precedent. For Wall Street, this isn’t just about $15 billion in annual App Store revenue — it’s about whether Apple’s 30% commission model remains legally insulated across the EU, UK, and Japan.

How Is the Apple App Store Dispute Reshaping Investor Sentiment?

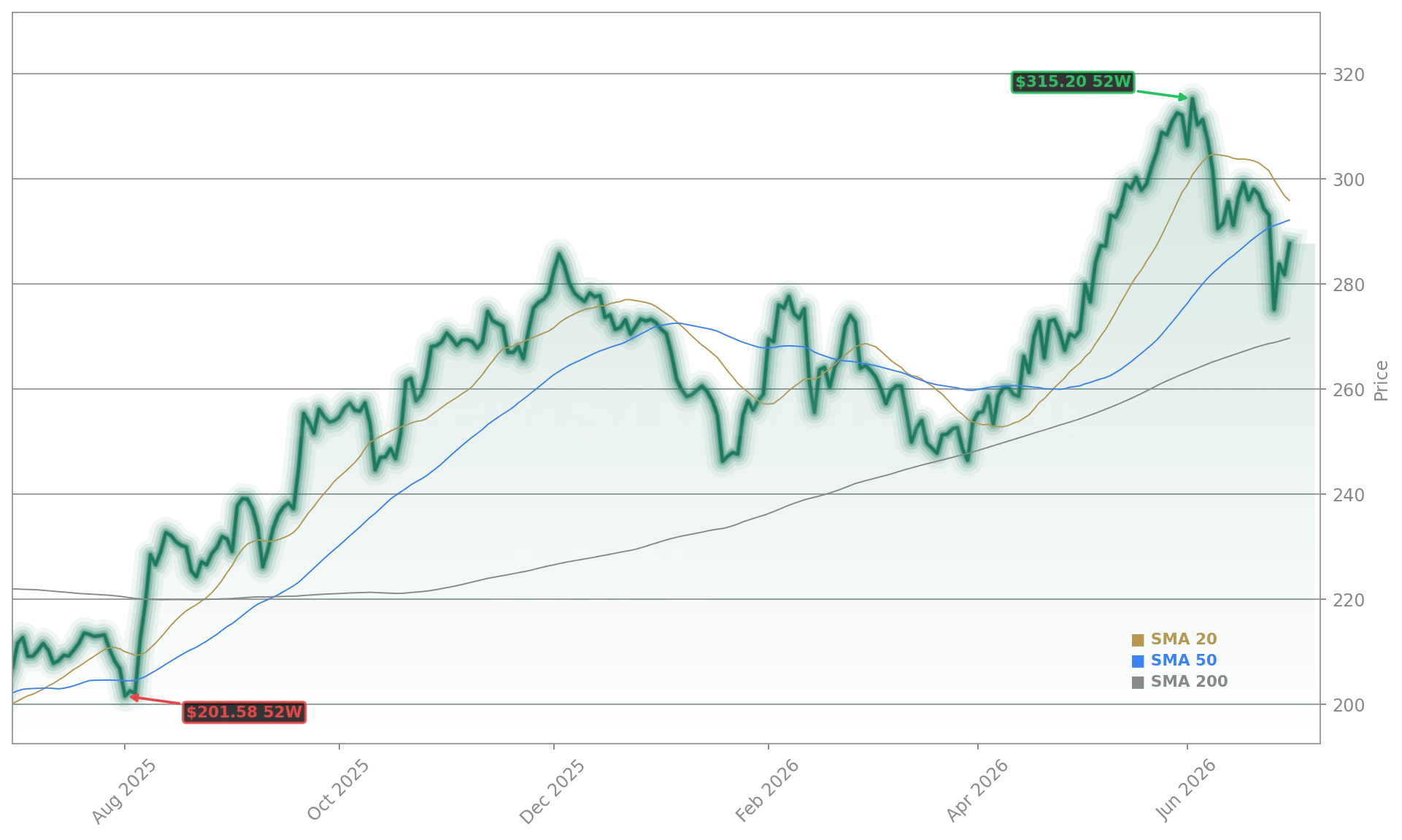

Despite the legal overhang, Apple shares rose 2.1% to $287.50 in after-hours trading — outperforming the broader NASDAQ, which fell 0.8% on the day. The rally suggests investors are discounting near-term legal risk while focusing on fundamentals: Services revenue hit $30.98 billion last quarter, up 16.1% year over year, with margins holding at 32%. That segment now contributes 28% of total revenue and 41% of operating profit — a critical buffer as hardware faces headwinds. Bank of America maintained its $380 price target and Buy rating on June 22, citing ‘meaningful AI integration at WWDC’ and Siri’s upgraded on-device capabilities. Still, the Apple App Store Dispute remains a structural vulnerability — especially as Meta and NVIDIA accelerate AI-driven app ecosystems that bypass traditional storefronts.

Are Rising Chip Costs a Bigger Threat Than Regulation?

Yes — at least for near-term margins. Apple’s recent 10% one-month stock pullback was triggered not by the legal news, but by price hikes on Macs and iPads — some rising by over $300 — to offset surging memory costs. Micron Technology (MU), a key HBM supplier, is benefiting directly from AI infrastructure demand, while Apple’s gross margin dipped to 44.2% in Q1 2026, down from 45.1% a year earlier. The company confirmed shortages will persist, and CEO Tim Cook called it ‘an unprecedented challenge.’ Adding complexity: Apple’s reported effort to source chips from Chinese firm CXMT has drawn sharp rebuke from Senator Tom Cotton, who warned it would ‘put national security and customer privacy at risk.’ With Tesla and Apple both facing supply-chain cost inflation, investors are reassessing whether premium pricing power remains intact.

Where Does Apple Stand Against Its Magnificent Seven Peers?

Regulators around the world are watching this case to determine what commission rate Apple may charge on covered purchases in huge markets outside the United States.— Apple, in its Supreme Court filing

Apple underperformed the Magnificent Seven in June — down ~8% versus the group’s 10% aggregate decline — but its valuation remains the steepest: a forward P/E of 29 versus Microsoft’s 33 and Alphabet’s 26. RBC Capital Markets recently downgraded Apple to ‘Sector Perform,’ citing ‘limited AI differentiation’ and ‘regulatory overhang from the Apple App Store Dispute.’ Meanwhile, Morgan Stanley’s Mike Wilson cautioned against ‘blindly buying tech pullbacks,’ noting the widening gap between chip stocks and mega-cap software platforms. Apple’s 6.99% weight in the SPDR Technology Select Sector ETF (XLK) means any sustained underperformance directly drags on the fund’s returns — and by extension, many 401(k) and IRA portfolios anchored to broad tech exposure.