Can Novo Nordisk Wegovy regain momentum fast enough to challenge Eli Lilly before the next wave of obesity drugs resets the market?

Can Novo Nordisk Wegovy close the gap with Zepbound?

Yes — and it’s already happening. While Eli Lilly’s Zepbound dominates headlines with unmatched efficacy in late-stage trials, Novo Nordisk has quietly built a layered offensive: oral Wegovy launched in January 2026, months ahead of rival Foundayo’s similar offering, and has already generated over 2 million prescriptions in the U.S. alone. That’s not just adoption — it’s rapid patient and prescriber trust in a more convenient delivery format. Meanwhile, the newly approved high-dose Wegovy 7.2 mg pen, endorsed by the European Medicines Agency’s CHMP, demonstrated >20% mean weight loss in Phase 3 trials — narrowing the efficacy gap with Zepbound while offering differentiated dosing simplicity. For U.S. investors watching the NASDAQ biotech index, this isn’t incremental progress — it’s a structural repositioning in a sector where convenience, compliance, and dosing flexibility increasingly drive market share.

What’s next in Novo Nordisk’s obesity pipeline?

Beyond formulations, Novo Nordisk is advancing three high-potential assets that could redefine competitive dynamics by 2027. Its dual agonist amycretin — targeting both GLP-1 and amylin receptors — is now in Phase 3 trials across oral and subcutaneous routes. CagriSema, a GLP-1/GIP dual agonist, is on track for U.S. FDA approval before year-end. And UBT251 — a triple agonist (GLP-1/GIP/glucagon) — represents the company’s most ambitious next-generation candidate, with early data suggesting superior weight loss and metabolic benefits versus current standards. These aren’t speculative bets: all three are backed by robust clinical signals and align with investor demand for durable, multi-year growth beyond single-drug cycles. Compare that to Apple’s hardware refresh cadence or NVIDIA’s AI chip roadmap — Novo Nordisk is treating obesity like a platform, not a product.

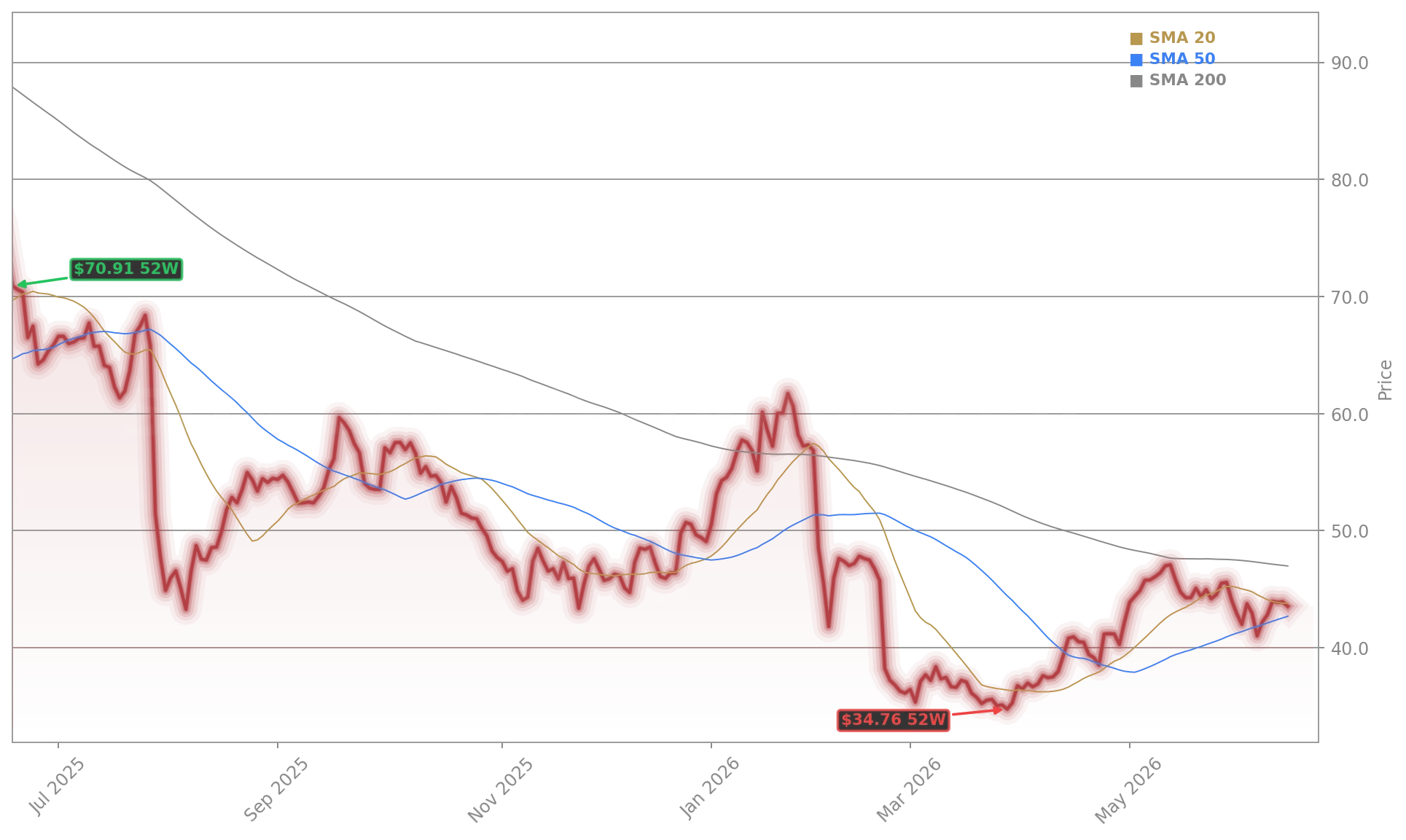

How does Novo Nordisk’s valuation compare to peers?

At $43.54 in after-hours trading, Novo Nordisk trades at a forward P/E of 13 — well below Eli Lilly’s 31.3 and the broader healthcare sector average of 17.4. That discount reflects recent underperformance, not fundamentals. Citigroup recently reaffirmed its $45.00 price target on NVO, citing ‘strong prescription momentum and underappreciated pipeline optionality.’ RBC Capital Markets upgraded Novo Nordisk to ‘Outperform,’ highlighting ‘oral Wegovy’s rapid uptake and the high-dose pen’s commercial readiness.’ The contrast with Eli Lilly is stark: LLY’s premium valuation assumes flawless execution across multiple indications, while NVO’s lower multiple offers margin for error — and upside if CagriSema or amycretin hits key milestones. For S&P 500 investors seeking healthcare exposure with asymmetric risk-reward, Novo Nordisk is re-emerging as a core holding.

Are cyber concerns a material risk to Novo Nordisk Wegovy?

A recent unauthorized data access incident involving clinical trial data — disclosed on June 12 — raised eyebrows but poses no near-term commercial threat to Novo Nordisk Wegovy. The company confirmed that no personally identifiable information was compromised, and the breach did not impact manufacturing, supply chain, or regulatory submissions for Wegovy formulations. External cybersecurity specialists are engaged, and authorities notified — standard protocol, not a red flag. Investors focused on Wall Street’s obesity trade should weigh this against the far larger risk: missing the inflection point in oral GLP-1 adoption. With over $15 billion in authorized share repurchases already 28% deployed (DKK 4.17 billion as of May 13), Novo Nordisk is signaling confidence in its cash flow and long-term growth trajectory — not retreating from the fight.

How are U.S. investors positioning for the next phase?

U.S. institutional investors are increasing exposure to Novo Nordisk ahead of Q2 earnings, betting on Wegovy’s expanding label and geographic rollout. The oral formulation is now covered by 82% of major U.S. commercial plans, and EU launch is expected in Q3 — a direct catalyst for international revenue acceleration. Meanwhile, Eli Lilly’s recent acquisition in pain therapeutics signals diversification beyond GLP-1, underscoring how competitive intensity is rising across the entire metabolic space. For portfolios tracking the NASDAQ Biotechnology Index, Novo Nordisk Wegovy is no longer just a weight-loss play — it’s a barometer for platform execution in chronic disease. With Phase 3 data for amycretin expected by late Q3 and CagriSema’s FDA decision due in December, the next 90 days will define Novo Nordisk’s 2026 narrative.

Oral Wegovy isn’t just a formulation change — it’s a commercial inflection point that reshapes patient access, adherence, and long-term market share.— RBC Capital Markets Analyst

Related coverage: Novo Nordisk Wegovy Falls 4.5% on Pipeline Warning examined investor skepticism ahead of clinical readouts, while Eli Lilly Acquisition Signals Pain Drug Boom Beyond GLP-1 highlights how the obesity leadership battle is expanding into adjacent therapeutic areas — raising the stakes for Novo Nordisk’s pipeline execution.