Can Taiwan Semiconductor keep climbing as Wall Street raises targets and AI chip demand tightens global supply even further?

Why Is Barclays So Bullish on Taiwan Semiconductor Manufacturing Co.?

Barclays analyst Simon Coles reiterated an Overweight rating and raised the price target for Taiwan Semiconductor Manufacturing Co. to $625 from $470—citing accelerating demand for 3nm and 2nm chips powering data centers, generative AI models, and autonomous systems. The move reflects confidence in the company’s unmatched process leadership and its ability to monetize supply constraints. With capital expenditures set to rise from $56 billion in 2026 to $74 billion in 2027, Barclays sees pricing power strengthening—not weakening—as capacity remains effectively sold out through year-end. This Taiwan Semiconductor Forecast upgrade is especially notable against a backdrop of broader tech volatility, where the S&P 500 fell 4.33% in Q1 and the Russell 1000 Growth index dropped 9.78%.

What Does the Institutional Buying Signal?

Institutional activity surged in Q1 2026. Kathmere Capital Management LLC increased its stake by 30.1%, while Collaborative Fund Advisors LLC and Ascentis Independent Advisors initiated new positions totaling over 15,000 shares. DGS Capital Management LLC boosted its holdings by 8.6%, and FUKOKU MUTUAL LIFE INSURANCE Co. raised its stake by 2,549.6%. Even amid selective selling by Hodges Capital Management Inc. and Walter Public Investments Inc., Taiwan Semiconductor Manufacturing Co. remains a top-10 holding across multiple funds. Insider buying—including purchases by VPs Lipen Yuan and Bor-Zen Tien—further reinforces confidence in the Taiwan Semiconductor Forecast trajectory.

How Does TSM Compare to Its AI Infrastructure Peers?

While NVIDIA leads in chip design and Apple drives end-market adoption, Taiwan Semiconductor Manufacturing Co. sits at the irreplaceable nexus of both—fabricating over 90% of the world’s most advanced semiconductors. Unlike pure-play equipment makers such as ASML, TSMC benefits from pricing power, recurring capacity contracts, and deep integration with customers. Its 70% share of the dedicated foundry market dwarfs competitors like Samsung Foundry and GlobalFoundries. With the Philadelphia Semiconductor Index up nearly 3% on July 6—snapping a two-day decline—the AI infrastructure trade remains intact, and Taiwan Semiconductor Manufacturing Co. is its most liquid, high-conviction proxy on Wall Street.

What’s Next Before the Analyst Day?

With its July 16 analyst day approaching, Taiwan Semiconductor Manufacturing Co. is expected to raise long-term revenue guidance and reaffirm 2026 growth targets—reinforcing the bullish Taiwan Semiconductor Forecast narrative. Citigroup has already recommended the stock for purchase ahead of the event, forecasting upward revisions to both top- and bottom-line projections. The January U.S.–Taiwan trade agreement, which secured favorable tariff treatment, adds another layer of near-term support. Meanwhile, options activity shows strong conviction: the $450 put strike carries a 61% probability of expiring worthless, while the $480 covered call yields a 15% boost—evidence that sophisticated investors are positioning for continued upside.

How Does the Taiwan Semiconductor Forecast Impact Broader Portfolios?

TSMC is the global linchpin of advanced semiconductor manufacturing, uniquely positioned to benefit from the secular expansion of AI compute.— RiverPark Large Growth Fund, Q1 2026 Investor Letter

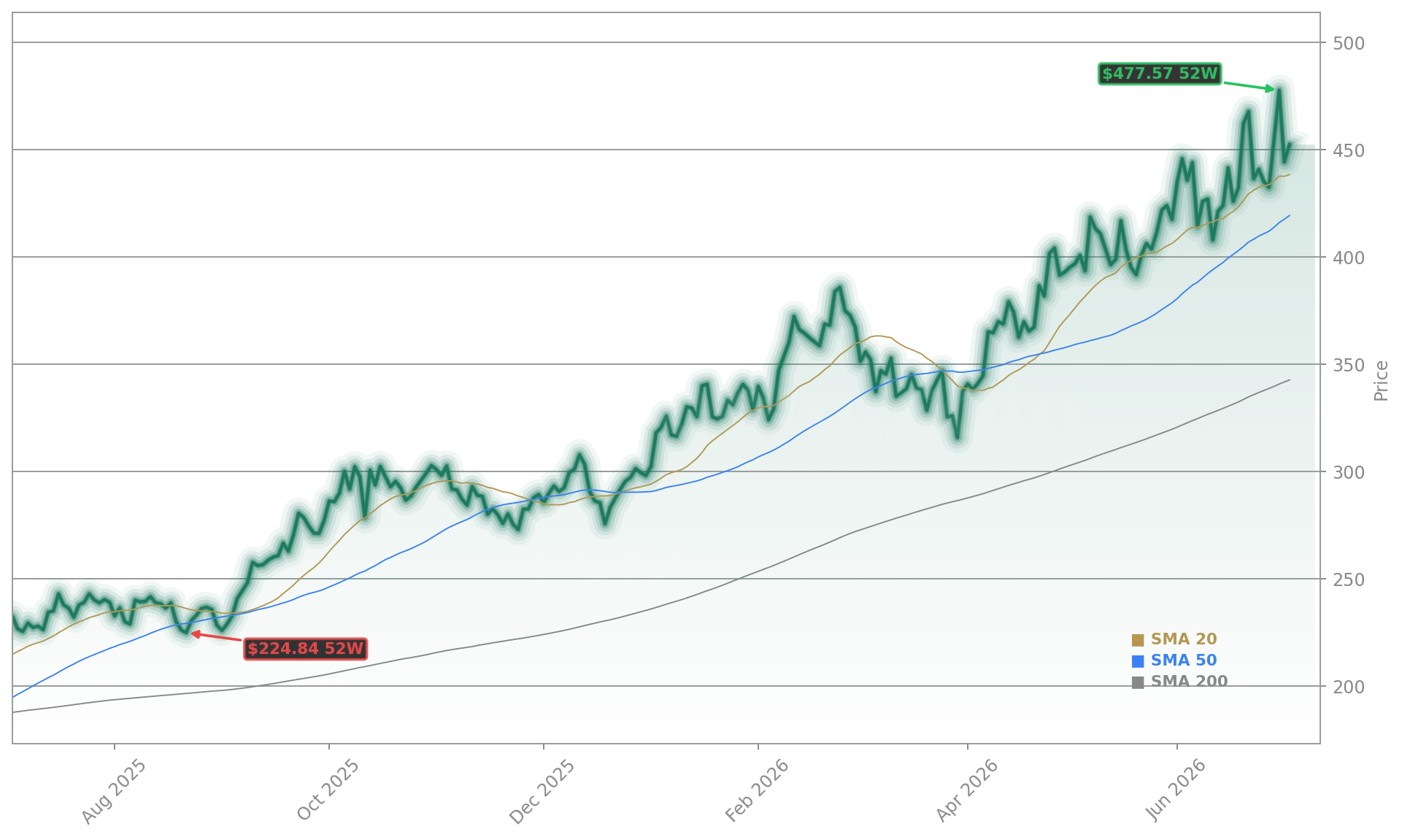

For U.S. investors, Taiwan Semiconductor Manufacturing Co. is increasingly a core holding—not just a satellite chip bet. Its 52-week gain of 93.52%, $2.00 trillion market cap, and 1.1% weighting in the NASDAQ-100 underscore its systemic role. With AI infrastructure spending expected to grow at a 28% CAGR through 2028 (per S&P Global), the Taiwan Semiconductor Forecast is no longer just about wafers—it’s about compute sovereignty, supply chain resilience, and long-term margin expansion. As RiverPark Large Growth Fund noted in its Q1 letter, TSMC’s ‘unmatched technological leadership’ and ‘disciplined capital allocation’ support durable pricing power—making it a rare compounder in today’s high-rate environment.