Why is the TSMC Forecast getting stronger just as the stock suffers a sharp sell-off?

Why Did TSMC Drop While Targets Rose?

Taiwan Semiconductor Manufacturing Co. fell to $445.95 — down 6.32% from its prior close — as the Nasdaq slid 0.87% and the technology sector declined 1.7%, its worst-performing S&P 500 group. The sell-off wasn’t company-specific: Intel dropped 7%, Advanced Micro Devices slid 5%, and the broader chip sector retreated on Bank of America’s warning of ‘bubble risk’ in the AI trade. Yet in the same 48-hour window, Barclays and UBS collectively raised their TSMC Forecast by $155 — a move rivaling the market cap of mid-cap industrial firms. This paradox reflects Wall Street’s dual narrative: unmatched execution on advanced node ramp (3nm, 2nm) versus growing unease over valuation (41.5x forward P/E) and concentration risk in AI-driven demand.

What Does the TSMC Forecast Say About AI Supply Chain Risk?

The TSMC Forecast isn’t just about margins — it’s a proxy for AI infrastructure resilience. With 92% of sub-5nm chips manufactured by Taiwan Semiconductor Manufacturing Co., its capacity utilization, lead times, and pricing power directly impact NVIDIA’s Blackwell rollout, Apple’s next-gen AI silicon, and cloud capex cycles. Bank of America Securities’ $590 target — up from $520 — assumes continued share gains in AI accelerators and data center SoCs, while Susquehanna’s $575 call hinges on 2nm yield ramp accelerating ahead of schedule. Still, the TSMC Forecast faces headwinds: geopolitical exposure remains acute, and U.S. export controls continue to constrain China-bound shipments — now 12% of revenue, down from 18% in Q2 2025.

How Does TSMC Compare to U.S. Chipmakers?

Unlike Intel or AMD, Taiwan Semiconductor Manufacturing Co. doesn’t design chips — it manufactures them. That foundry model delivers superior gross margins (56.2% in Q2 2026) but less pricing control. Intel’s foundry division remains unprofitable, AMD’s exposure is limited to fabless design, and neither commands the scale or yield leadership of Taiwan Semiconductor Manufacturing Co. Still, the TSMC Forecast must be weighed against U.S. policy shifts: the CHIPS Act subsidies are accelerating domestic capacity, and TSMC’s Arizona fab is now shipping 4nm wafers — though volume remains under 5% of global output. For U.S. portfolios, this means TSMC offers pure-play exposure to AI hardware demand without the execution risk of chip design — but with outsized sensitivity to U.S.-China tech decoupling.

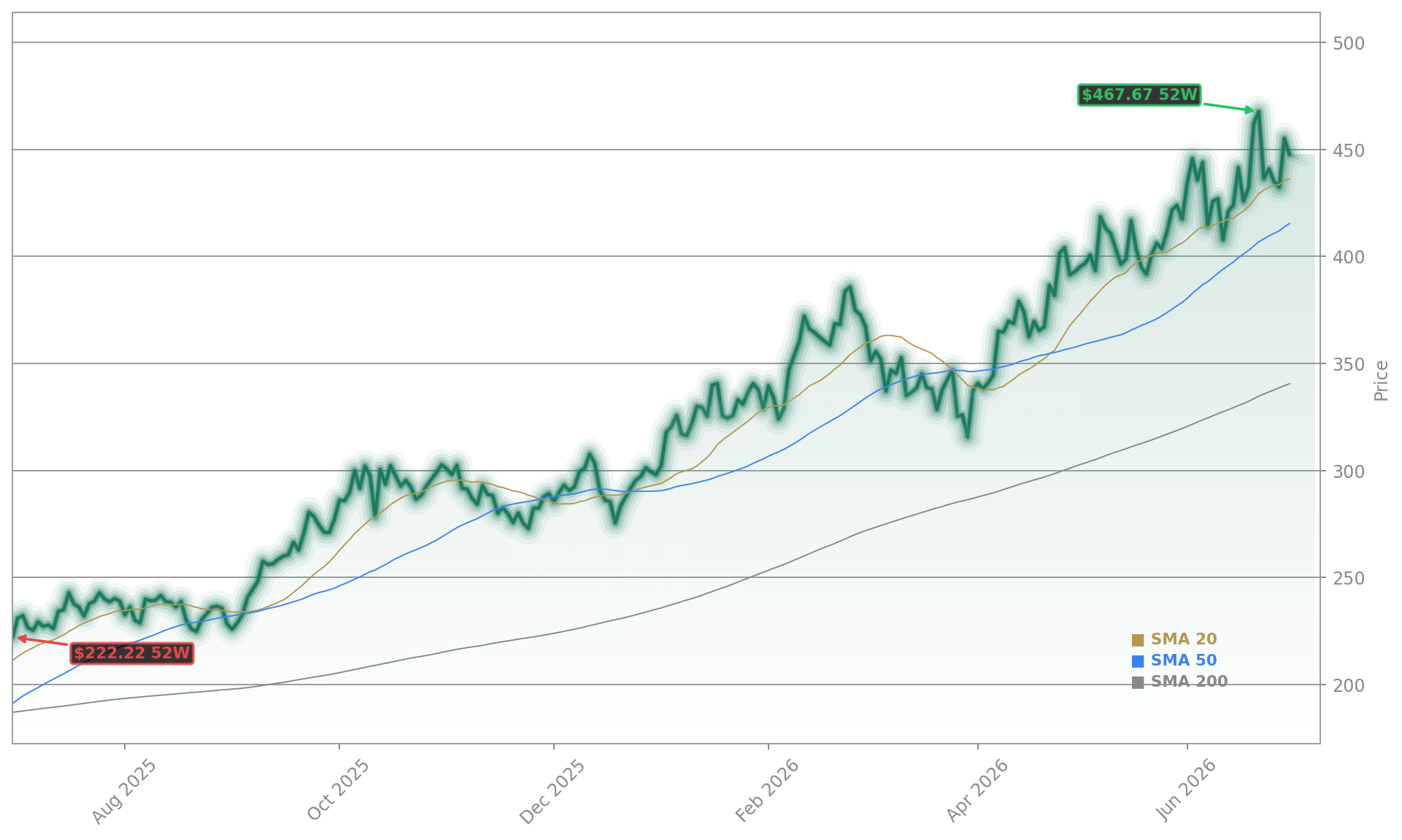

What Do Technicals Say About the Pullback?

Despite Wednesday’s decline, Taiwan Semiconductor Manufacturing Co. remains in a structurally bullish technical posture: trading 30.8% above its 200-day simple moving average ($343.18), with the 20-day SMA above the 50-day and 50-day above the 200-day — a ‘golden cross’ configuration. Momentum indicators are neutral (RSI: 54.34), and the stock recently hit a 52-week high in June — suggesting this is profit-taking, not trend reversal. Key support sits at $405.50, while resistance looms at $450 — just above current levels. Heavy ETF ownership (up to 9.98% in Pacific NoS Global EM Equity Active ETF) means inflows/outflows can amplify moves, adding volatility ahead of earnings.

What’s Next for the TSMC Forecast?

The July 16 earnings report is the next catalyst — with Wall Street expecting $3.77 EPS on $39.76 billion in revenue, up 32% year-over-year. The TSMC Forecast will pivot on three metrics: 2nm ramp timing, AI-related wafer demand growth (now 41% of total), and gross margin trajectory amid rising capex. Analysts at Citigroup and Morgan Stanley have not yet updated targets post-UBS/Barclays, but consensus remains a Buy with a $489.17 average price forecast. For investors, the TSMC Forecast signals resilience — but also warns that valuation premiums demand flawless execution.

TSMC remains the irreplaceable engine of AI hardware — but its premium valuation means every earnings miss will echo across the entire semiconductor supply chain.— RBC Capital Markets Analyst

Related Coverage: The TSMC AI Strategy continues gaining traction, with record margins fueling expansion into AI-optimized foundry services — TSMC AI Strategy +1.9% as Record Margins Fuel Expansion. Meanwhile, Meta’s cloud infrastructure push is accelerating AI monetization, reinforcing demand for TSMC’s most advanced nodes — Meta Cloud +10.9%: Meta Soars as AI Push Expands.