If S&P just turned more bullish on TSMC, why did the stock suddenly drop more than 5%?

What Does S&P’s Taiwan Semiconductor Rating Upgrade Mean for U.S. Investors?

S&P Global Ratings revised its outlook on Taiwan Semiconductor Manufacturing Co. to Positive on June 23, 2026, citing accelerating EBITDA growth, widening technology barriers, and a $52–$56 billion capital expenditure budget aimed squarely at AI-driven capacity expansion. The ‘AA-‘ long-term issuer credit rating remains affirmed — a rare distinction for a non-U.S. industrial firm. Crucially, S&P highlighted that TSMC’s revenue share among the top 10 global foundries jumped to 72% in 2025 — up from 54.6% in 2021 — while its scale advantage over its nearest peer grew to 8.7x from 2.9x. For U.S. investors, this isn’t just a credit rating: it’s validation that TSMC’s role as the irreplaceable bottleneck in the AI stack remains structurally intact — and increasingly bankable.

Why Are Insiders Buying While the Stock Pulls Back?

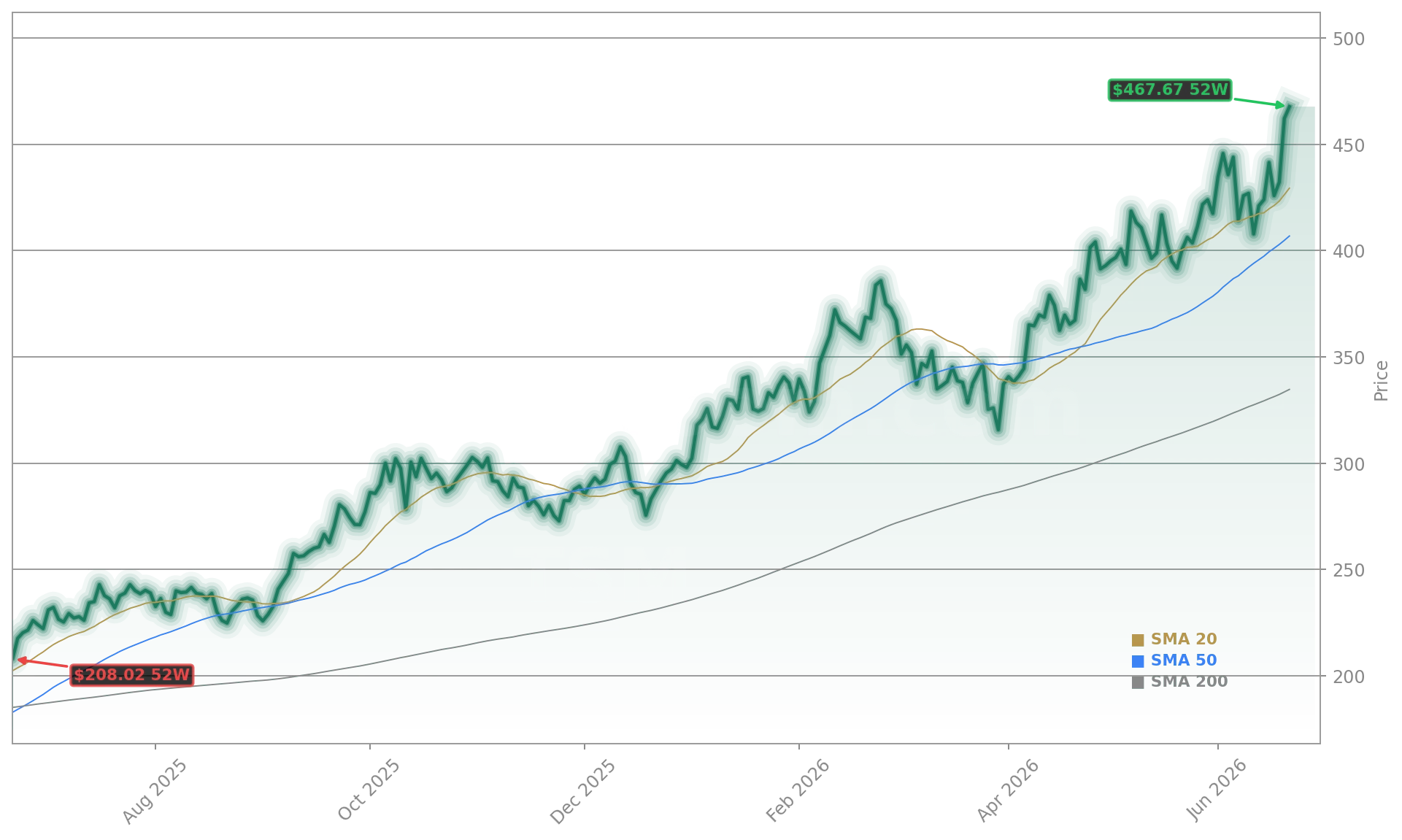

Taiwan Semiconductor Manufacturing Co. saw a wave of insider purchases in mid-June — including Executive Vice President Lipen Yuan, who acquired 200 shares at $395.95 on June 22, and COO Chin Yung-Pei, who bought 14 shares the same day. These transactions follow a string of purchases by VPs Bor-Zen Tien and Tzu-Sou Chuang earlier in May and June. The timing is telling: shares fell 5.06% in premarket trading on Tuesday, June 23, as Nasdaq futures dropped 2.41% in a broad risk-off move. Yet TSM remains 32.4% above its 200-day moving average — a technical signal of enduring institutional demand. The insider activity reflects confidence in the July 16 earnings report, where Wall Street expects $3.69 EPS and $39.76 billion in revenue — up 32% year over year.

How Does Taiwan Semiconductor Rating Compare to Intel and Samsung?

While Intel’s rumored Apple deal sent shares soaring, analysts remain skeptical of near-term impact. Wedbush’s Matt Bryson noted Intel still trades at enterprise-value-to-sales multiples comparable to Taiwan Semiconductor Manufacturing Co. and Advanced Micro Devices — despite lacking their yield performance or foundry scale. Meanwhile, Susquehanna raised its price target on Taiwan Semiconductor Manufacturing Co. to $575 from $500 on June 22, citing multi-year customer supply commitments and a $200 billion+ CapEx roadmap. Barclays and DA Davidson have also recently upgraded — to $470 and $450, respectively. In contrast, Samsung Foundry and Intel Foundry face ecosystem gaps: neither has TSMC’s client depth, packaging integration, or co-development partnerships with NVIDIA, Apple, and Broadcom.

Is the Taiwan Semiconductor Rating Justified at Today’s Valuation?

Taiwan Semiconductor Manufacturing Co. trades at a forward P/E of 27x — lower than NVIDIA’s 23x and far below AMD’s 192x — yet delivers 58.1% operating margins and a 36.2% return on equity. Its price-to-sales ratio remains a fraction of NVIDIA’s 19.55x, even as wafer revenue surged from NT$714 billion to NT$968 billion year over year. Simply Wall Street estimates fair value at $400 — suggesting a 15.5% premium — but that model assumes slower AI infrastructure growth than S&P’s forecast of 30%+ annual revenue growth through 2027. With high-performance computing now 58% of TSMC’s revenue — up from 43% in 2023 — the company is far less cyclical than memory or smartphone-focused peers like Micron.

What’s Next for the Taiwan Semiconductor Rating?

The next catalyst arrives July 16 with Q2 2026 earnings — and analysts expect a full-year guidance lift. TSMC’s CEO C.C. Wei has already stated global chip supply will fall short of demand for years. Meanwhile, U.S. expansion is accelerating: TSMC’s Arizona fab is ramping with yield parity to Taiwan, and its $165 billion U.S. investment includes $6.6 billion in CHIPS Act funding. With the company planning to shift 30% of its 2nm+ capacity offshore by 2030, geopolitical risk is being actively mitigated — not ignored. The Taiwan Semiconductor Rating isn’t just bullish — it’s becoming a benchmark for semiconductor resilience.

Related coverage: Taiwan Semiconductor AI Growth Surges 5.7% on AI Demand analyzes how U.S. fab ramp and co-packaging with NVIDIA are accelerating TSMC’s AI revenue trajectory. Meanwhile, Intel Apple Deal -7.8%: Shock Tests Intel Foundry Hype shows why Wall Street is tempering expectations on Intel’s foundry ambitions — reinforcing TSMC’s irreplaceable role.

Global chip supply would still fall short of demand for years to come.— C.C. Wei, Chairman and CEO of Taiwan Semiconductor Manufacturing Co.

Taiwan Semiconductor Manufacturing Co. remains the structural foundation of the AI revolution — and its upgraded credit outlook, insider buying, and widening technology moat make its Taiwan Semiconductor Rating a critical signal for U.S. portfolios. For investors seeking exposure to AI’s infrastructure layer — not just its application layer — TSMC’s premium reflects durability, not speculation. The next quarterly earnings will confirm whether the $575 price target from Susquehanna is conservative.