If the Broadcom Google AI Deal is truly locked in through 2031, why is AVGO still sliding?

Is the Broadcom Google AI Deal Really Locked In?

Yes — and JPMorgan says it’s the single strongest catalyst for AVGO’s forward valuation. In a June 22 research note titled ‘Ignore The Noise,’ analysts Harlan Sur and Mayur Ramdhani explicitly refuted reports of delays or cancellations in Broadcom’s collaboration with Google on the TPU v9 2nm chip. Their assessment, based on proprietary primary research, confirms the program is progressing with ‘NO delays; NO cancellations’ and remains on track for a CY28 ramp. Crucially, the firm highlighted a March 2026 agreement that locks in Broadcom’s design win roadmap for four successive TPU generations — v8 through v11 — with annual revenue increases guaranteed through 2031. That contractual certainty transforms AI revenue from a volatile growth story into a high-margin, predictable cash engine — a rare trait in semiconductor equities.

How Does This Compare to NVIDIA and Meta?

While NVIDIA dominates AI training with GPUs, Broadcom Inc. is capturing the inference and interconnect layer — arguably the fastest-growing segment of AI infrastructure. Its custom ASICs power Google, Meta, OpenAI, and Anthropic, with AI chip revenue hitting $10.8 billion in Q2 2026 — up 143% year over year. That’s more than double NVIDIA’s AI inference revenue in the same period, and Broadcom expects Q3 AI chip sales to surge to $16 billion. Unlike pure-play chipmakers, Broadcom integrates silicon, networking, and software — giving it a structural advantage in delivering full-stack AI clusters. Its networking business, described by CEO Hock Tan as ‘taking off like a rocket,’ is now a critical enabler for hyperscalers scaling beyond 100,000-GPU clusters — a domain where Cisco and Arista are playing catch-up.

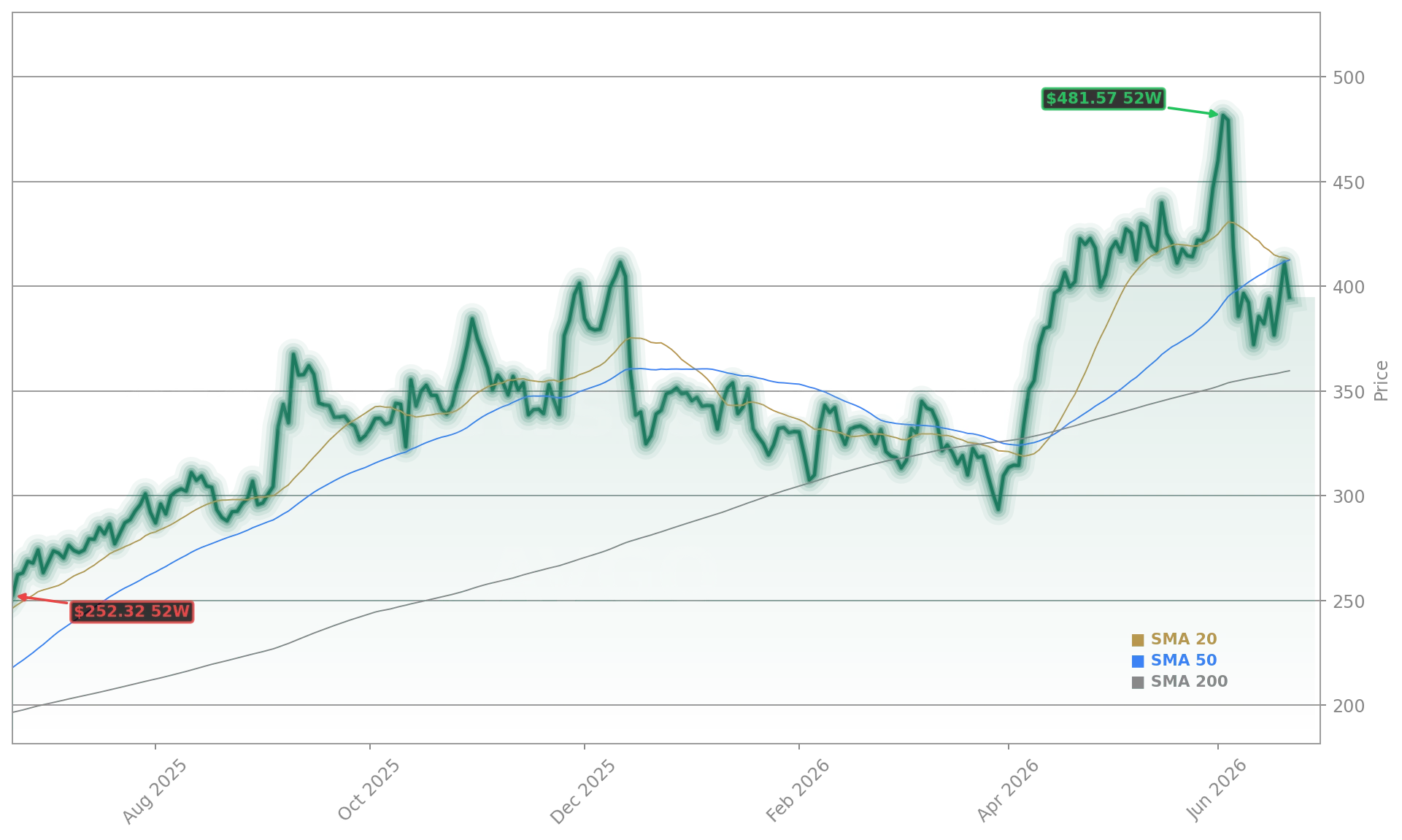

Why Did AVGO Drop Despite Strong Numbers?

Broadcom Inc. reported record Q2 2026 revenue of $22.2 billion (+48% YoY), $15.2 billion in adjusted EBITDA (+52%), and $10.3 billion in free cash flow (+60%). Yet the stock dipped 2.22% over the prior month. The reason? Wall Street’s expectations had outpaced even exceptional execution — a recurring theme across the AI chip sector. As one strategist noted, ‘good might not be good enough’ when investors price in multi-year hypergrowth. That sentiment briefly weighed on the Nasdaq-100, where Broadcom ranks fifth by weight behind Apple, Microsoft, and Amazon. Still, the recent pullback has created a tactical entry point: JPMorgan maintains its ‘Overweight’ rating and raised its December 2026 price target to $580 — implying 40.99% upside from current levels.

What’s the Broader Market Impact?

Contrary to the recent noise… that Broadcom/Google has delayed or canceled its next-gen Google TPU v9 2nm program, we believe, based on our own recent primary research work and past reports… that the team remains on track.— Harlan Sur and Mayur Ramdhani, JPMorgan

Broadcom Inc. is no longer just a semiconductor stock — it’s a core holding in AI-focused ETFs like the QQQ (5.57% weight) and VIG (top-three holding). Its performance now moves indices: a recent earnings release triggered broad tech weakness, underscoring its systemic importance. With AI-related revenue expected to exceed $100 billion by fiscal 2027 — more than double its $75 billion TTM total — Broadcom is scaling faster than most peers. Its 69% EBITDA margin and capital-light, fabless model further insulate it from manufacturing volatility. Competitors like Marvell (MRVL) and AMD are gaining traction, but Broadcom’s Google-aligned roadmap, 70% ASIC market share, and $1.96 trillion market cap cement its role as the infrastructure backbone of the AI supercycle — not just a beneficiary.