Is Broadcom’s latest AI momentum strong enough to justify JPMorgan’s aggressive call and a much higher target from here?

Why did JPMorgan call for aggressive buying?

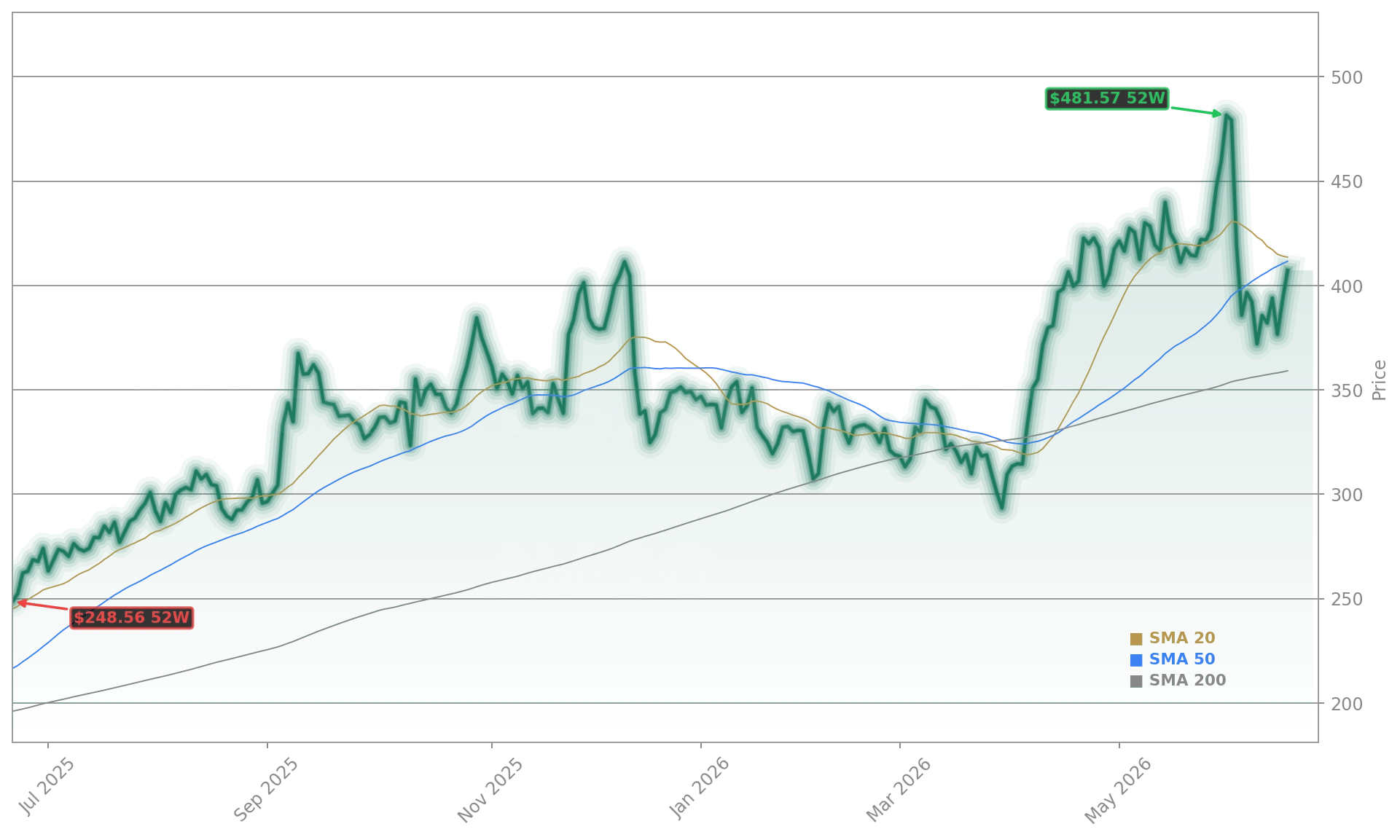

JPMorgan analysts reaffirmed their ‘Overweight’ rating and $580 price target for Broadcom Inc.—a 38% upside from its current $407.79 share price—citing resolution of near-term uncertainty around the Google co-developed Tensor Processing Unit v9. The firm dismissed recent supply chain concerns as ‘overblown’ and emphasized that TPU-v9 development remains on schedule in advanced 2-nanometer fabrication. This clarity helped reverse a 20% pullback from recent highs and triggered a 4.3% intraday rally on Wednesday, followed by continued strength in after-hours trading. JPMorgan highlighted three structural advantages: leadership in advanced chip packaging, unmatched IP portfolio depth, and rapid time-to-market for next-gen AI accelerators—factors that underpin the long-term Broadcom Forecast of $100 billion in AI-related revenue.

What does the 8-K reveal about debt strategy?

Broadcom Inc. filed a Form 8-K on June 18, 2026, disclosing the successful upsize and expiration of its cash tender offers for outstanding debt securities. The company increased its debt buyback program from $2.5 billion to $3 billion—reflecting strong cash flow generation and disciplined capital allocation amid record AI infrastructure spending. Unlike peers facing margin pressure from R&D inflation, Broadcom’s gross margin held at 75.2% in Q2—its highest in five quarters—bolstering confidence in its ability to fund both organic growth and strategic M&A. The move also signals management’s commitment to optimizing capital structure ahead of potential rate stabilization later this year, a nuance Wall Street analysts say strengthens the credibility of its Broadcom Forecast for sustained double-digit EPS growth.

How does Broadcom compare to AI semiconductor peers?

While NVIDIA remains the dominant force in AI training silicon, Broadcom Inc. is the undisputed leader in AI networking and custom ASICs for inference—key enablers for hyperscalers like Alphabet and Microsoft. Its Q2 AI revenue of $16.0 billion—up 143% YoY—outpaced Marvell (up 89%) and matched AMD’s AI acceleration growth, though AMD’s exposure remains more GPU-centric. Notably, Broadcom trades at just 24x forward P/E versus Marvell’s 47x, despite comparable 3-year CAGR expectations of ~28%. Citigroup recently noted that ‘Broadcom’s execution consistency and lower multiple make it the most asymmetric AI infrastructure bet in semis.’ RBC Capital Markets added that ‘the TPU-v9 validation removes the single largest overhang for institutional buyers.’ This valuation gap—and the growing role of Broadcom Inc. in AI stack integration—makes the Broadcom Forecast especially compelling for S&P 500 and NASDAQ investors seeking exposure beyond the Magnificent Seven.

What’s driving the broader semiconductor rally?

Broadcom Inc. added 8 points to the S&P 500 on Thursday—its largest single-day contribution in 2026—fueling a sector-wide surge that lifted the Philadelphia Semiconductor Index (SOX) 2.9%. The rally reflects tightening conviction that AI capex is not peaking but evolving: from GPU-heavy training to distributed inference, optical interconnects, and custom silicon like TPU-v9. With hyperscalers committing over $119 billion in AI-related supply agreements—per NVIDIA disclosures—Broadcom Inc. stands to benefit from both near-term networking upgrades and long-term chiplet and packaging demand. Analysts at Morgan Stanley point out that ‘Broadcom’s infrastructure moat is wider than ever—not just in silicon, but in system-level integration.’ That structural advantage is central to every credible Broadcom Forecast for 2026–2027.

Broadcom’s execution consistency and lower multiple make it the most asymmetric AI infrastructure bet in semis.— Citigroup

Related Coverage: Broadcom’s explosive Q2 AI revenue growth is detailed in Broadcom AI Earnings +3.3% as Q2 AI Revenue Soars, while investors weighing broader semiconductor exposure should review Micron Forecast +3.5%: Targets Rise Before June 24 Earnings, which examines memory demand dynamics across the AI stack.