If Broadcom posted record AI revenue, why did Broadcom Earnings still spark a brutal market backlash?

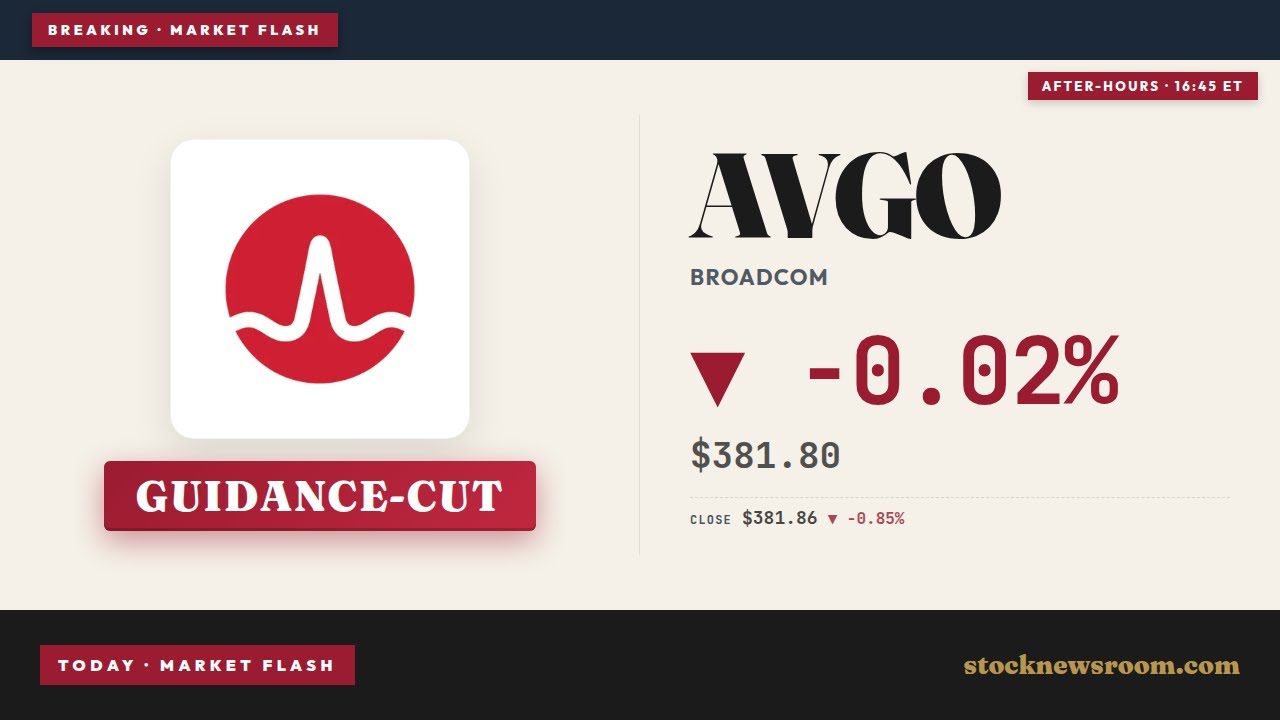

Why did Broadcom Earnings trigger a 14% selloff?

Despite delivering $22.2 billion in quarterly revenue — up 48% year over year — and reporting AI chip revenue more than doubling to $10.8 billion, Broadcom Inc. shares dropped sharply in after-hours trading. The selloff was the steepest for chip stocks since early 2025 and dragged down peers including NVIDIA and AMD. Wall Street had priced in aggressive upward guidance, particularly for AI semiconductors, where consensus expected $17.2 billion for Q3. Instead, management reaffirmed its $100 billion full-year AI target and forecast $16 billion for the next quarter — a 12.5% shortfall versus expectations. That gap, combined with a $70 million revenue miss versus the $22.27 billion analyst consensus, triggered immediate repricing.

Is Broadcom Inc. still the AI ASIC leader?

Yes — and its structural advantages remain intact. Broadcom Inc. dominates the custom AI chip space with multi-year partnerships locked in through 2029 with Meta and through 2031 with Google. Its application-specific integrated circuits (ASICs) power Alphabet’s TPUs, Anthropic’s $21 billion TPU order, and OpenAI’s 10GW inference engine. The company’s AI order book now stands at $73 billion, with total corporate backlog approaching $162 billion. Its 70% semiconductor gross margins and 67% operating margin guidance for Q3 further validate its pricing power. Yet investors are increasingly weighing whether that leadership justifies a non-GAAP P/E of 61x — nearly double that of NVIDIA (36x) and well above Micron (44x).

What do analysts say about Broadcom Earnings?

Citigroup recently lowered its price target on Broadcom Inc. to $410 from $445, citing ‘guidance conservatism and valuation compression risk.’ RBC Capital Markets maintained its ‘Outperform’ rating but noted ‘the stock is now priced for flawless execution across a $100 billion AI roadmap — leaving little margin for error.’ Meanwhile, Morgan Stanley highlighted Broadcom’s networking and co-packaged optics (CPO) leadership as a ‘critical, underappreciated tailwind,’ pointing to energy savings of up to 65% versus pluggable optics — a key factor for hyperscalers optimizing AI data center capex. The firm raised its 2027 revenue estimate by 3.2% but held its target at $425, emphasizing execution risk over fundamentals.

How does Broadcom Inc. fit in the AI capex boom?

Broadcom’s earnings were not good. And my Trust lost a huge amount of money, and I feel really badly about it. It can make a comeback. I hope there’s some insider buying. They did miss the numbers.— Jim Cramer, CNBC

With global AI infrastructure capex projected at $725 billion in 2026 — exceeding the GDP of over 170 countries — Broadcom Inc. sits at the center of two converging mega-trends: custom silicon and optical interconnect. While NVIDIA leads GPU training, Broadcom Inc. owns the inference and networking stack. Its Ethernet and CPO solutions are essential for moving data between custom chips — a bottleneck that grows more acute as AI models scale. That dual leverage explains why Harvard University’s 2026 stock portfolio ranks Broadcom Inc. #6, holding $146.7 million in shares. Yet the valuation challenge persists: even with 47.2% projected two-year revenue growth, the stock’s forward P/E drops only to 15x by 2028 — assuming flawless delivery. That’s not a discount for skeptics — it’s a test of conviction.