Is this AMD Upgrade the moment Wall Street finally starts valuing AMD as an AI GPU contender instead of just a CPU company?

What triggered the AMD Upgrade?

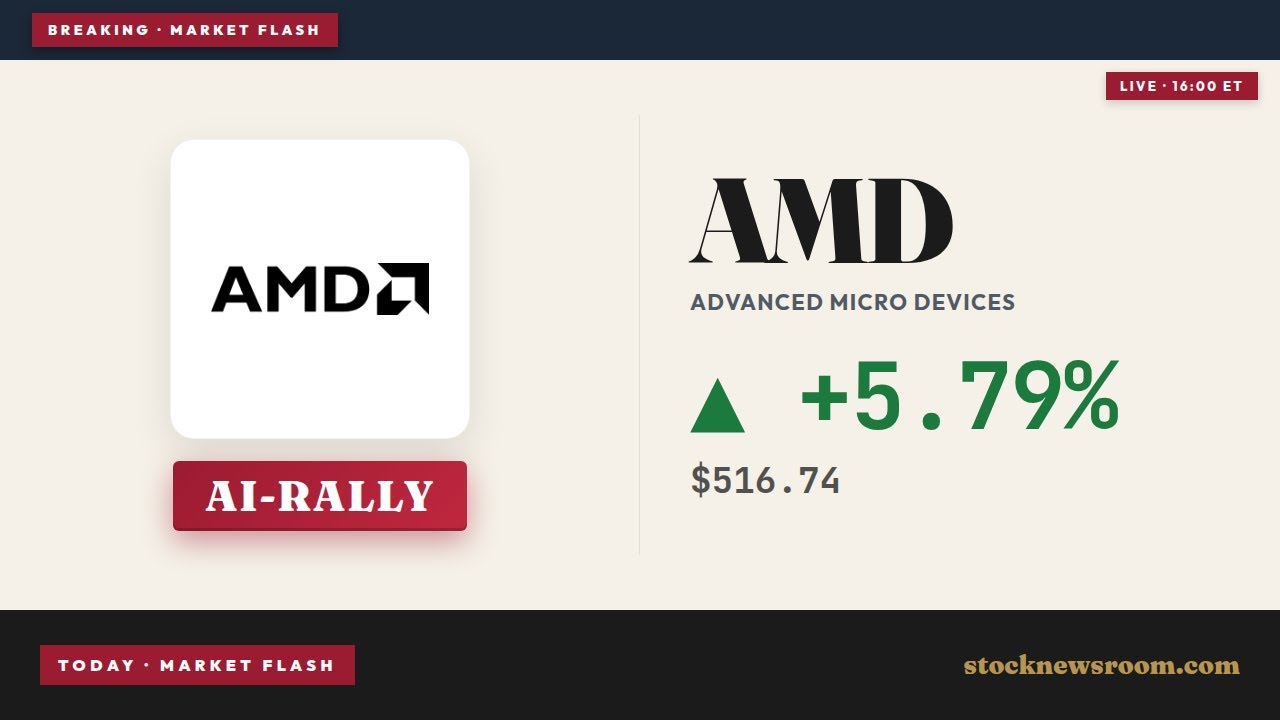

Citigroup analyst Atif Malik upgraded Advanced Micro Devices, Inc. to Buy from Neutral on June 12, 2026, lifting the price target to $575 from $460. The move follows a confluence of catalysts: AMD’s custom MI450 GPU design winning a six-gigawatt, four-year deal with Meta Platforms — including a 160 million-share warrant — and accelerating traction in AI infrastructure beyond CPUs. Malik emphasized that the market still prices AMD as a CPU-centric company, overlooking its rapidly scaling GPU business. That misperception, he noted, creates meaningful upside: ‘AMD is poised to win lion’s share at Meta,’ with custom chips delivering lower total cost of ownership than merchant alternatives from NVIDIA.’

How does AMD compare to NVIDIA and Intel?

While NVIDIA remains Wall Street’s undisputed AI leader — and Citigroup’s top semiconductor pick — the AMD Upgrade reflects growing confidence in AMD’s ability to capture meaningful GPU share. Bank of America reinforced this view, raising its own target to $560 and highlighting the server CPU market’s expansion to $136.7 billion by 2030 (up from $125 billion), driven by agentic AI and energy-intensive workloads. Intel, meanwhile, faces mounting pressure: Reuters reported delivery timelines stretching to six months for Chinese customers, underscoring supply constraints AMD is actively exploiting. AMD’s forward P/E of 54x remains well below ARM’s 152x, suggesting relative valuation discipline amid growth acceleration.

Is the AI revenue forecast realistic?

Citigroup’s revised AI revenue forecast for AMD is aggressive — $33 billion in 2027 and $50.8 billion in 2028 — representing 137% and 54% annual growth, respectively. These numbers assume rapid ramp of Meta’s first one-gigawatt tranche in H2 2026 and broader adoption of AMD’s Instinct MI400-series across hyperscalers. Barclays and TD Cowen have also lifted targets — to $665 and $600 — signaling consensus building around AMD’s dual-CPU-and-GPU AI playbook. Still, valuation remains stretched: at 162.8x trailing P/E, AMD trades at a premium reflective of high expectations — a dynamic shared with peers like Tesla and Apple in their respective growth phases.

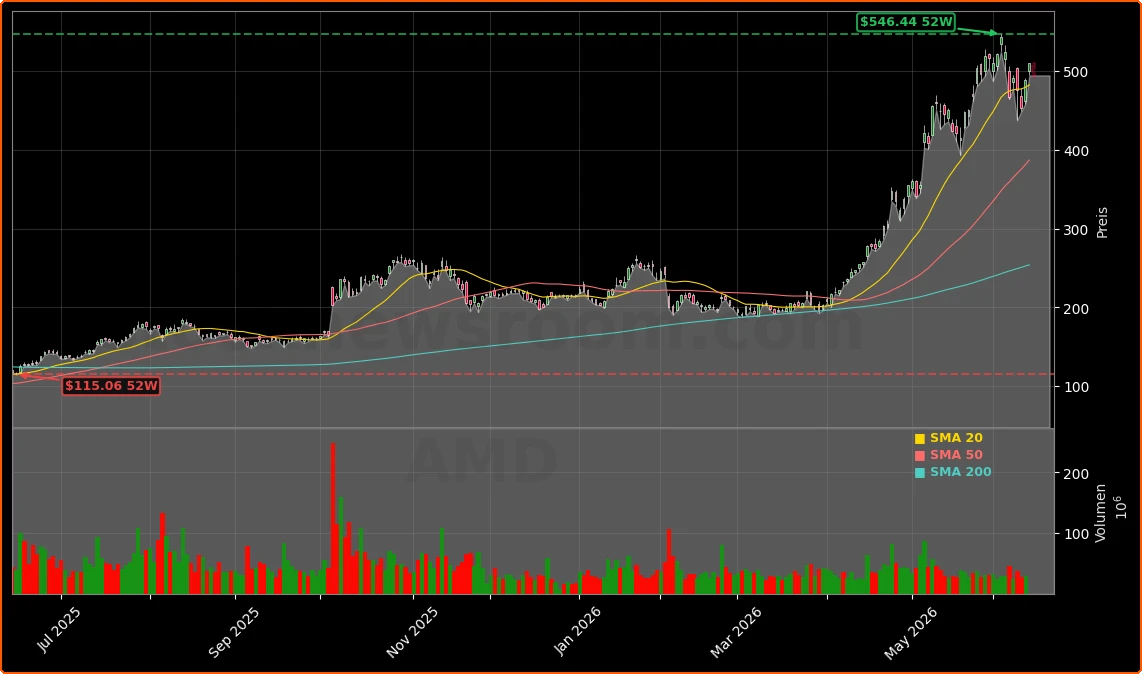

What does the technical picture say?

Technically, AMD is in a strong uptrend: trading 2.8% above its 20-day moving average ($478.88) and comfortably above all major moving averages. However, momentum indicators are cooling — the MACD remains below its signal line — and the stock approaches $546.50, its 52-week high resistance zone. A decisive breakout could open a path toward $575 and beyond; failure may trigger consolidation ahead of the August 4 earnings report. Wall Street expects $1.55 EPS and $11.28 billion in revenue — up 223% year-over-year — underscoring how much of the rally is forward-looking and AI-dependent.

AMD Upgrade: What’s next for Wall Street?

This AMD Upgrade isn’t isolated — it’s part of a broader semiconductor rebound. The iShares Semiconductor ETF (SOXX) surged over 8% on Thursday, and AMD joined NVIDIA, Micron, and Marvell in gains of up to 11.7%. With S&P 500 futures up 0.19% early Friday and Polymarket assigning an 83% probability to a higher open, investor sentiment is shifting from geopolitical risk to AI execution. The upcoming Nasdaq debut of SpaceX — a $1.77 trillion IPO — further validates institutional appetite for high-growth tech infrastructure. For U.S. portfolios, AMD’s upgrade signals a maturing competitive landscape in AI chips — one where diversification beyond NVIDIA is no longer theoretical, but contractually secured.

We believe Meta will be a significantly larger customer of AMD’s AI products, especially GPUs, than the street is expecting. We believe the use of custom MI450 GPUs is likely to provide Meta lower TCO vs merchant GPU products.— Atif Malik, Citigroup

Related Coverage: For deeper analysis of AMD’s dual-path AI strategy — combining CPU leadership with emerging GPU scale — see AMD AI Strategy +3.3% as CPU Surge Lifts Wall Street View. Investors tracking broader AI infrastructure momentum should also review Marvell S&P 500 Inclusion -2.3% as AI Momentum Builds, which explores how index inclusion is reshaping institutional allocations in the semiconductor space.