Is AMD’s AI push finally proving it can win with CPUs and ecosystem scale, not just by chasing Nvidia in GPUs?

Why Is AMD Gaining While Nvidia Stalls?

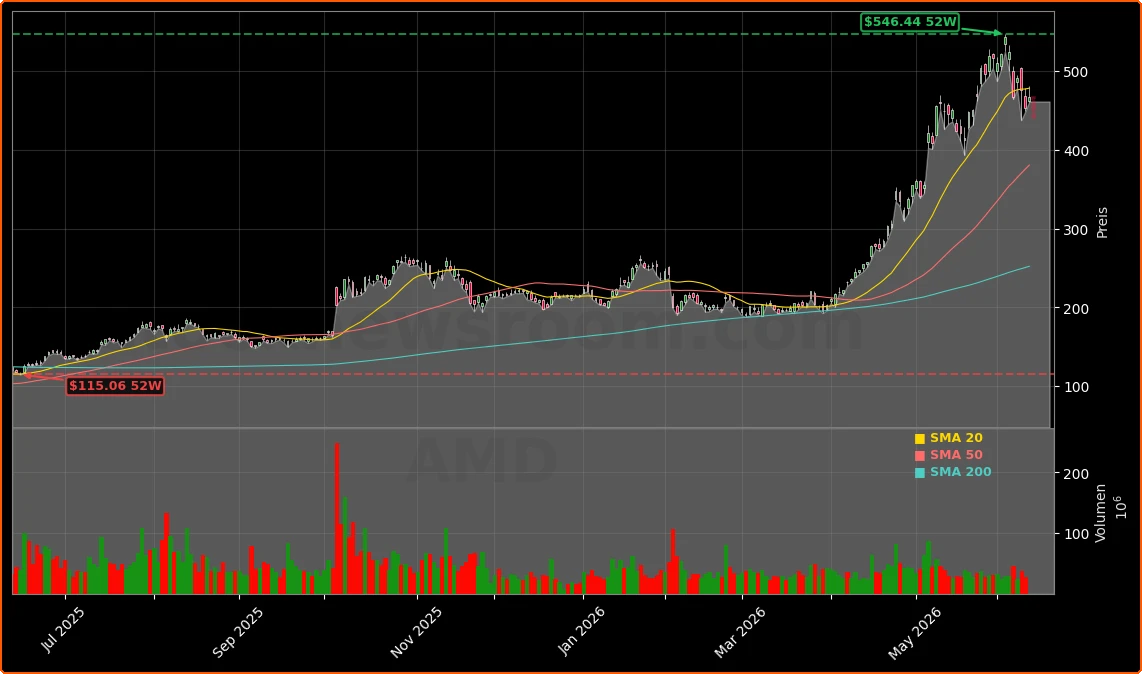

Advanced Micro Devices, Inc. surged 4% to $470 in Thursday premarket trading — recovering from a 5% intraday retreat on Wednesday triggered by broader semiconductor volatility and macro concerns. While NVIDIA shares remain near all-time highs, AMD’s relative outperformance reflects growing investor confidence in its differentiated AMD AI Strategy: not just competing in GPUs, but redefining AI infrastructure around x86 CPU scalability. Unlike Nvidia’s GPU-centric stack, AMD is embedding AI acceleration directly into its EPYC server processors and enabling full-stack deployments via partners like TensorWave — a $350 million-funded startup building exclusively AMD-powered data centers. This approach directly targets hyperscaler pain points around power efficiency, software portability, and total cost of ownership.

How Is AMD’s CPU Push Reshaping the AI Server Market?

AMD captured 33% of the server CPU market in Q1 2026 — up 6 percentage points year over year — driven by the EPYC ‘Venice’ architecture, which AMD claims delivers over 3x the performance of Nvidia’s Vera CPU at identical power draw. With over 36,000 cores per server rack, Venice enables true rack-scale execution for agentic AI workloads — a capability AMD highlighted in its June 10 technical blog as essential for production deployment. This isn’t theoretical: Q1 2026 data center revenue hit $5.78 billion, up 57% year over year and representing 56% of total company revenue. Bank of America noted that AMD’s data center segment now drives earnings growth more than client or embedded divisions — a structural pivot confirming the AMD AI Strategy’s execution.

What Does the TensorWave Deal Reveal About AMD’s Ecosystem Play?

The $350 million Series B funding for TensorWave — announced June 10 — is more than a venture bet. It’s AMD’s answer to Nvidia’s circular financing model, where chipmakers invest in cloud providers to lock in demand. TensorWave exclusively deploys AMD Instinct MI355X GPUs and EPYC CPUs, and commits to co-developing ROCm software enhancements. SiliconANGLE reports the startup plans to expand global data center capacity using this stack — directly challenging Nvidia’s AI cloud monopoly. Unlike Nvidia’s CUDA-only ecosystem, AMD’s open ROCm platform is gaining traction with Meta and OpenAI, though analysts at 24/7 Wall St. note AMD has offered equity warrants to secure those contracts — signaling competitive intensity remains high.

How Do Analysts View AMD’s Valuation and Growth Trajectory?

Bank of America Securities maintained its Buy rating on Advanced Micro Devices, Inc. and raised its price target to $560 from $500, citing ‘massive TAM expansion’ for AI-demand accelerators tied to CPU opportunities. Barclays followed with an Overweight rating and lifted its target to $665, emphasizing AMD’s capital-light model — outsourcing manufacturing to TSMC avoids Intel’s $100+ billion fab investments. Yet valuation remains a watchpoint: AMD trades at a forward P/E of 68x, and its Q2 2026 guidance — $11.2 billion in revenue and 56% gross margin — implies continued acceleration. With a 52-week high of $471, the stock is now just 1.5% below that peak, reinforcing momentum despite near-term volatility.

AMD AI Strategy: What Comes Next for Wall Street?

Advanced Micro Devices, Inc. is now executing the most aggressive and coherent AMD AI Strategy in its history — one that integrates silicon, software, and infrastructure. The next catalyst arrives in late July with Q2 2026 earnings, where investors will scrutinize EPYC adoption rates among Tier-1 cloud providers and MI355X ramp progress. With Intel surging 8% on the same day and the VanEck Semiconductor ETF (SMH) up 146% year-to-date on diversified AI exposure, AMD’s role as a multi-architecture enabler — not just a GPU challenger — is gaining institutional traction. The AMD AI Strategy is no longer aspirational; it’s delivering measurable share gains, revenue reacceleration, and ecosystem leverage.

Related coverage: Can AMD’s TensorWave gamble turn AI infrastructure ambition into durable demand, or is Wall Street right to punish the stock first? AMD TensorWave Funding: Stock Tanks 5% on AI Cloud Bet. Meanwhile, Arm Holdings’ AI story faces headwinds after a sharp after-hours warning — investors are reassessing valuation discipline across the entire AI chip stack. Arm Holdings Forecast: -7.7% After-Hours Warning for Bulls.

We delivered an outstanding first quarter, driven by accelerating demand for AI infrastructure, with Data Center now the primary driver of our revenue and earnings growth.— Lisa Su, CEO of Advanced Micro Devices, Inc.

Advanced Micro Devices, Inc. is executing its AMD AI Strategy with precision and scale — turning CPU leadership into AI infrastructure leverage. For U.S. investors, this means exposure to both the enduring server market and next-generation agentic AI workloads. The next quarterly earnings will confirm whether this momentum sustains through the second half of 2026. For long-term portfolios, AMD remains a core AI infrastructure holding with accelerating earnings power.