Can NVIDIA keep its AI dominance intact as export controls, Senate scrutiny, and a sharp stock drop collide at once?

Why is NVIDIA Export Controls in the Senate spotlight?

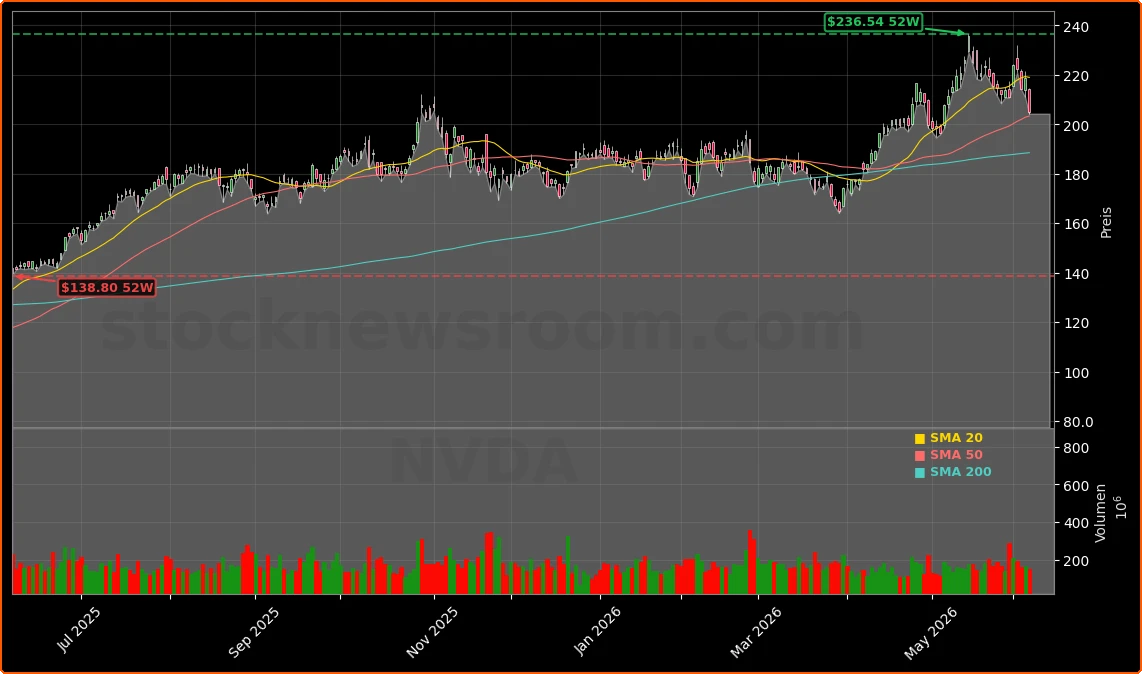

Senator Elizabeth Warren has formally invited NVIDIA CEO Jensen Huang to testify before the Senate Banking Committee on June 11, demanding clarity on the company’s China business and compliance with U.S. export controls. The subpoena follows Bloomberg reporting that Chinese entities—including Alibaba—may have exploited jurisdictional loopholes to acquire restricted Blackwell AI chips via servers purchased in Malaysia and Singapore. This regulatory uncertainty arrives just as NVIDIA’s Q1 FY2027 revenue surged to $81.61 billion (+85.2% YoY), yet China Data Center compute contributed zero dollars—down from $4.6 billion a year earlier. With no H20 shipments in Q1 and Q2 guidance explicitly excluding Chinese DC revenue, NVIDIA Export Controls are now directly constraining top-line growth and investor confidence.

How are HBM4 suppliers reshaping NVIDIA’s supply chain?

NVIDIA has certified Samsung, SK Hynix, and Micron to supply HBM4 memory for its next-generation Vera Rubin AI platform—marking a strategic pivot toward multi-vendor resilience. All three are now in volume production, enabling NVIDIA to scale Vera Rubin shipments in Q3 despite U.S. restrictions limiting China-bound hardware. This move reassures hyperscalers like Meta and OpenAI, which have committed $119 billion in multi-gigawatt Rubin deployments. Yet investor enthusiasm has faded: Micron (MU) dropped 10% in pre-market trading despite the certification, signaling that supply chain validation is now priced in—while macro risks dominate. Morgan Stanley analyst Joseph Moore maintains an Overweight rating and $288 price target, noting NVIDIA’s ‘king of diversity’ positioning across AI compute, networking, and CPUs—but warns sentiment won’t shift overnight amid rising yields and regulatory noise.

What’s driving the broader tech sell-off?

A confluence of macro forces is pressuring NVIDIA and the NASDAQ: the May nonfarm payroll report showed 172,000 jobs—nearly double forecasts—spiking 2-year Treasury yields to 4.14% and pushing Fed hike odds to 58% by December. That, combined with Broadcom’s (AVGO) soft AI chip outlook and Anthropic’s public call for a global AI development pause, has triggered a ‘risk-off’ rotation. The NASDAQ fell 2.5% on Friday, with NVIDIA contributing 91 points to the decline. Semiconductor stocks bore the brunt—SOXX dropped 6.8%, while NVIDIA, AMD, and Micron collectively erased over $500 billion in market cap. Bank of America’s Vivek Arya maintains a Buy rating and $350 target, stressing NVIDIA’s widening moat and $200 billion agentic AI CPU opportunity—but acknowledges valuation sensitivity in a higher-rate environment.

How does NVIDIA compare to peers amid AI infrastructure saturation?

Appearing as a witness will give you an opportunity to testify about Nvidia’s views on U.S. export control laws and regulations and Nvidia’s business in China.— Senator Elizabeth Warren

While NVIDIA remains the AI infrastructure anchor—accounting for 18.6% of the Vanguard Information Technology ETF (VGT)—its 19% YTD gain lags SOXX’s 99% surge, revealing market rotation toward memory and networking enablers. Micron trades at a forward P/E of 11.5—well below NVIDIA’s 23.75—and has sold out its 2026 HBM3E/HBM4 capacity. Yet NVIDIA’s dominance persists: it supplies every major hyperscaler and model maker, and its Vera Rubin platform is expected to boost AI infrastructure content per gigawatt from $40 billion today to $100 billion+ with the Feynman architecture. Gil Luria notes NVIDIA’s 22x earnings multiple remains safer than Broadcom’s 35x, but RBC Capital Markets cautions that custom silicon from Amazon and Google could erode margins if capex flattens. With 58 of 61 analysts maintaining Buy ratings and a $298.07 consensus target, the bull case remains intact—but hinges on Q2 execution and China policy clarity.