Can NVIDIA Earnings still shock Wall Street when even explosive growth may no longer be enough?

Can NVIDIA Earnings clear the bar?

The setup is unusually demanding. Consensus points to roughly $79 billion in quarterly revenue and adjusted earnings per share near $1.76 to $1.81, implying around 80% top-line growth and another major profit surge. Yet for many investors, that is only the baseline. The real question in this NVIDIA Earnings report is whether management can again deliver the beat-and-raise formula that powered the stock for most of the AI boom.

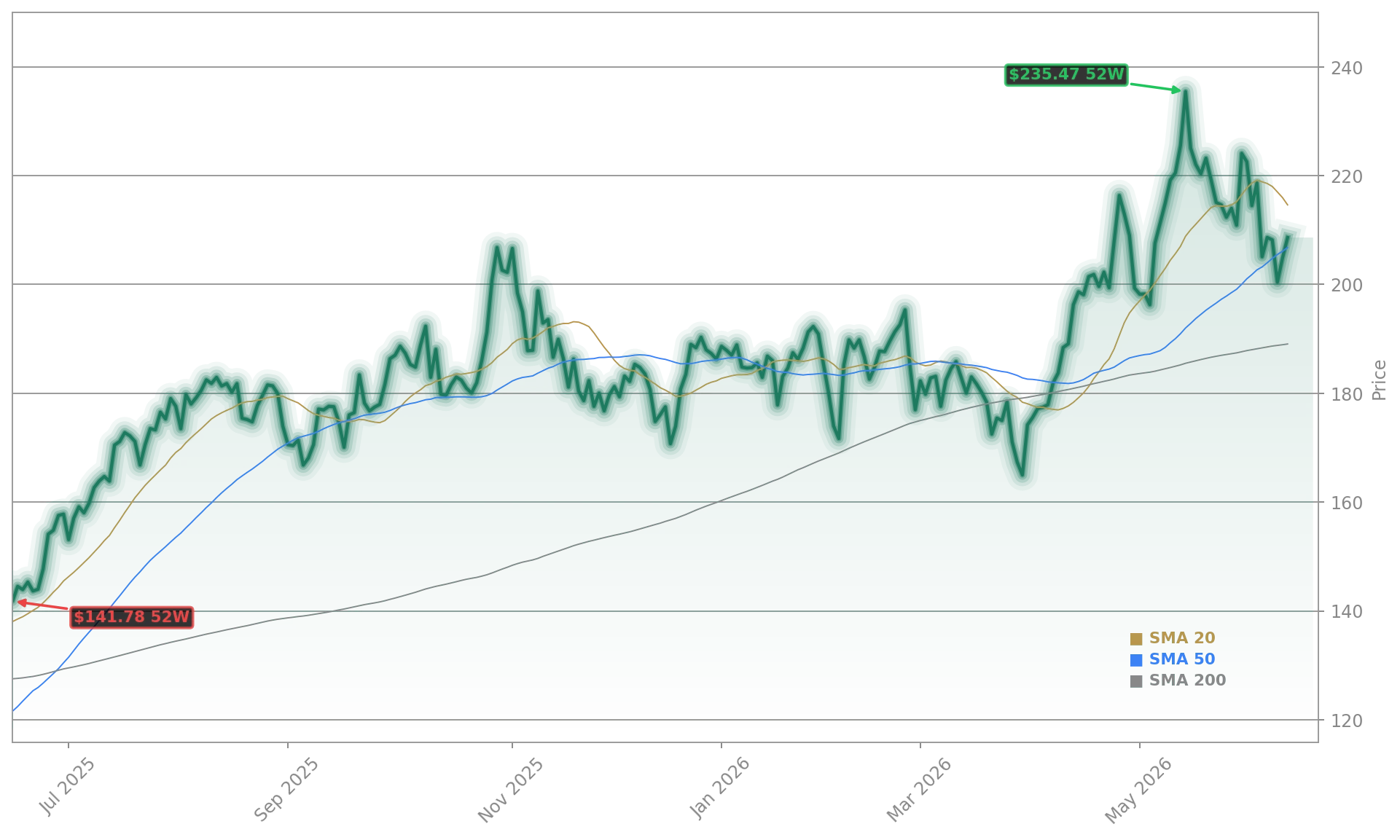

That challenge is harder now because expectations have moved higher even as post-earnings reactions have turned less forgiving. NVIDIA has fallen after several recent reports despite beating estimates, a sign that strong numbers alone may no longer be enough. Options markets are pricing a roughly 6% to 7% move after the release, underlining how much is riding on tonight’s update.

Is NVIDIA still driving Wall Street?

For US investors, this is no longer just a semiconductor story. NVIDIA carries enormous weight in the S&P 500 and NASDAQ, and strategists increasingly view it as a macro stock disguised as a chipmaker. If guidance disappoints, the damage could extend quickly to the broader AI complex, including AMD, Microsoft, Amazon, and equipment names tied to data-center buildouts.

The bullish case remains powerful. Hyperscalers continue spending aggressively on AI infrastructure, and NVIDIA still holds the dominant position in accelerated computing. Reuters reported Wednesday that Lambda won a cloud deal with Hudson River Trading that includes access to more than 1,000 Blackwell systems, another sign that demand for NVIDIA hardware remains deep. At the same time, chip stocks such as ASML and Infineon showed signs of stabilization after recent volatility, suggesting investors still want exposure if tonight’s numbers hold up.

What will NVIDIA say on margins?

Beyond revenue, gross margin may be the most closely watched operating metric. Management previously indicated about 75% non-GAAP gross margin, plus or minus 50 basis points. On Wall Street, that level has become a line in the sand because it speaks directly to pricing power as Blackwell ramps and competition grows.

Investors will also focus on the next-quarter revenue outlook. Market expectations center around $87 billion, while buy-side forecasts in some cases have drifted above $90 billion. That gap matters. A guide above the official consensus could reignite the AI trade, while anything meaningfully below it could trigger a sell-the-news reaction.

Analyst sentiment is still favorable. Evercore ISI noted that investor enthusiasm has cooled from last year’s extremes, but firms including DA Davidson, Wedbush, and KeyBanc have raised price targets into the report. CLSA has also stayed constructive on NVIDIA while lifting targets across major semiconductor names, and Barclays has pointed to call spreads as a way to position for upside while respecting elevated expectations.

How big are China and competition?

China remains an unresolved swing factor. NVIDIA has effectively excluded China data-center compute from near-term assumptions, and any sign of renewed access would be upside. But management also has to answer tougher questions about custom silicon from cloud giants and mounting competition from rivals. Apple is not a direct AI chip rival, yet its lower-margin profile is often used to highlight how exceptional NVIDIA’s profitability has become among mega-cap tech firms.

Related Coverage: Investors looking for a deeper preview can also read NVIDIA Earnings: AI Boom Faces China Risk and Big Expectations. That analysis looks more closely at the China angle and explains why even blockbuster growth may no longer be enough if the forward outlook slips.

NVIDIA Earnings now look like a referendum on AI spending, chip pricing, and market leadership all at once. If Jensen Huang delivers strong guidance, firm margins, and confidence around Blackwell supply, Wall Street may treat this as another green light for the AI rally. If not, tonight could reset expectations for NVIDIA and the broader tech trade heading into summer.