Can NVIDIA Earnings keep justifying the AI frenzy as revenue surges and a massive new outlook raises the bar again?

Why did NVIDIA Earnings matter so much?

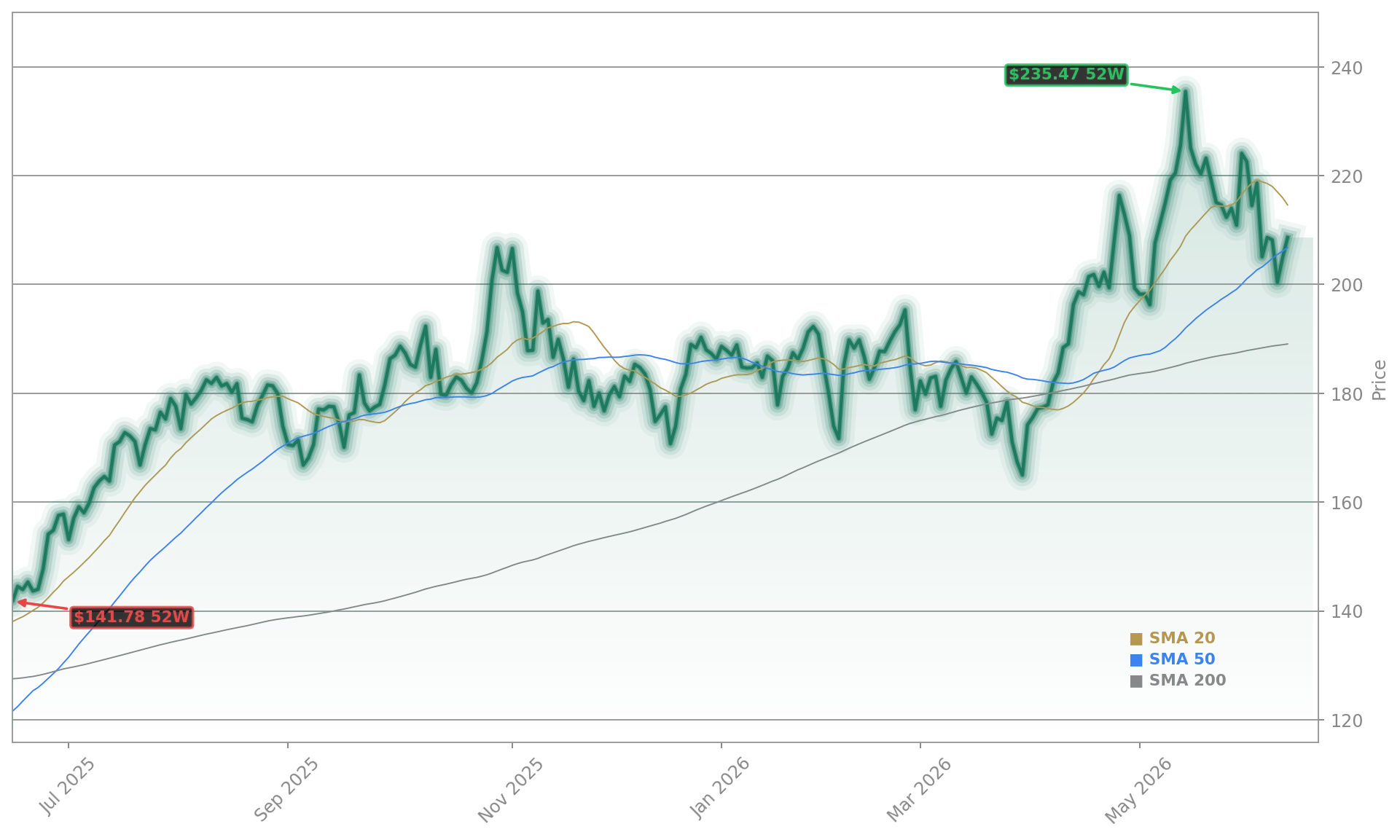

NVIDIA Corporation reported fiscal first-quarter revenue of $81.6 billion, up 85% from a year earlier and above expectations near $79 billion. Non-GAAP diluted earnings per share came in at $1.87, also ahead of consensus. The stock closed Wednesday at $223.47, up 1.30% from the prior close of $221.54, then slipped to $222.23 in after-hours trading, down 0.55% as investors weighed just how much of the beat had already been priced in.

The real headline was guidance. NVIDIA said second-quarter revenue is expected at $91.0 billion, plus or minus 2%, well above the roughly $87 billion sell-side consensus and close to the more aggressive buy-side whisper range that had circulated before the release. Gross margin stayed firm at 75.0% on a non-GAAP basis, reinforcing the idea that the Blackwell ramp is not destroying profitability.

How strong was NVIDIA really?

Data Center remained the engine, with revenue of $75.2 billion, up 92% year over year. Under the prior reporting structure, data center compute revenue reached $60.4 billion while networking hit a record $14.8 billion, up 199% from a year ago. That matters because networking has become a cleaner signal for full-rack Blackwell deployments, not just standalone GPU demand.

Chief Executive Jensen Huang said the buildout of AI factories is accelerating and described agentic AI as already producing real economic value. Investors have heard bold language before, but this quarter backed it with numbers. NVIDIA also maintained its assumption of zero Data Center compute revenue from China in the current-quarter outlook, suggesting guidance strength came from demand elsewhere rather than from a hoped-for export rebound.

The company also moved aggressively on shareholder returns, authorizing an additional $80 billion in repurchases and lifting its quarterly dividend from $0.01 to $0.25 per share. That is a meaningful signal for larger institutions that have wanted NVIDIA to look more like Apple in capital allocation discipline.

What does NVIDIA mean for peers?

This report lands at a crucial moment for semiconductors. Ahead of the release, chip names like Micron, Marvell, and Intel had rallied as traders positioned for a healthy read on AI infrastructure spending. Reuters also reported that Lambda won a cloud deal with Hudson River Trading built around more than 1,000 NVIDIA Blackwell systems, underscoring how deeply NVIDIA hardware remains embedded across new AI capacity.

At the same time, Wall Street is still watching competitive pressure from custom chips at Amazon, Microsoft, and Alphabet, along with systems from Advanced Micro Devices. Even so, NVIDIA’s latest numbers suggest that the total AI spending pie is still expanding fast enough for the market leader to grow at extraordinary scale.

Analyst targets had already moved higher into the print. Morgan Stanley raised its target to $285, HSBC to $325, GF Securities to $308, KeyBanc to $300, while RBC and Goldman Sachs stayed more measured around $250. That spread shows the core debate: not whether demand is strong, but how much upside remains after a huge run and a 52-week high of $236.54 already set last week.

Can NVIDIA Earnings keep lifting markets?

NVIDIA Earnings were always likely to shape sentiment far beyond one stock. With an outsized index weight and a central role in AI capex, the company acts as a market-level confidence gauge. This quarter probably keeps the broader AI narrative intact: hyperscaler spending remains powerful, margins remain elite, and capital returns are now rising alongside revenue.

Related Coverage: Our earlier piece, NVIDIA Earnings +2.1%: Can Tonight’s AI Report Extend the Boom?, looked at whether sky-high expectations had become the bigger risk than the quarter itself. That preview highlighted the same core issue investors are debating now: a beat was expected, but guidance and market reaction would decide whether the AI rally still has fuel.

The buildout of AI factories — the largest infrastructure expansion in human history — is accelerating at extraordinary speed.— Jensen Huang

For investors, NVIDIA Earnings again cleared a very high bar. The next test is whether after-hours hesitation turns into renewed momentum once Wall Street fully digests the $91 billion outlook, stronger capital returns, and the message that AI demand is still scaling faster than most competitors can match.