If NVIDIA Earnings keep smashing records, why is Wall Street still acting like it expected even more?

Why did NVIDIA Earnings fail to spark a bigger rally?

NVIDIA Earnings once again showed the company’s dominance in AI infrastructure. Revenue for the quarter rose 85% year over year to about $81.6 billion, while adjusted earnings per share came in at $1.87, above consensus expectations. Data center revenue climbed to roughly $75 billion, underscoring how deeply NVIDIA remains tied to the global AI buildout.

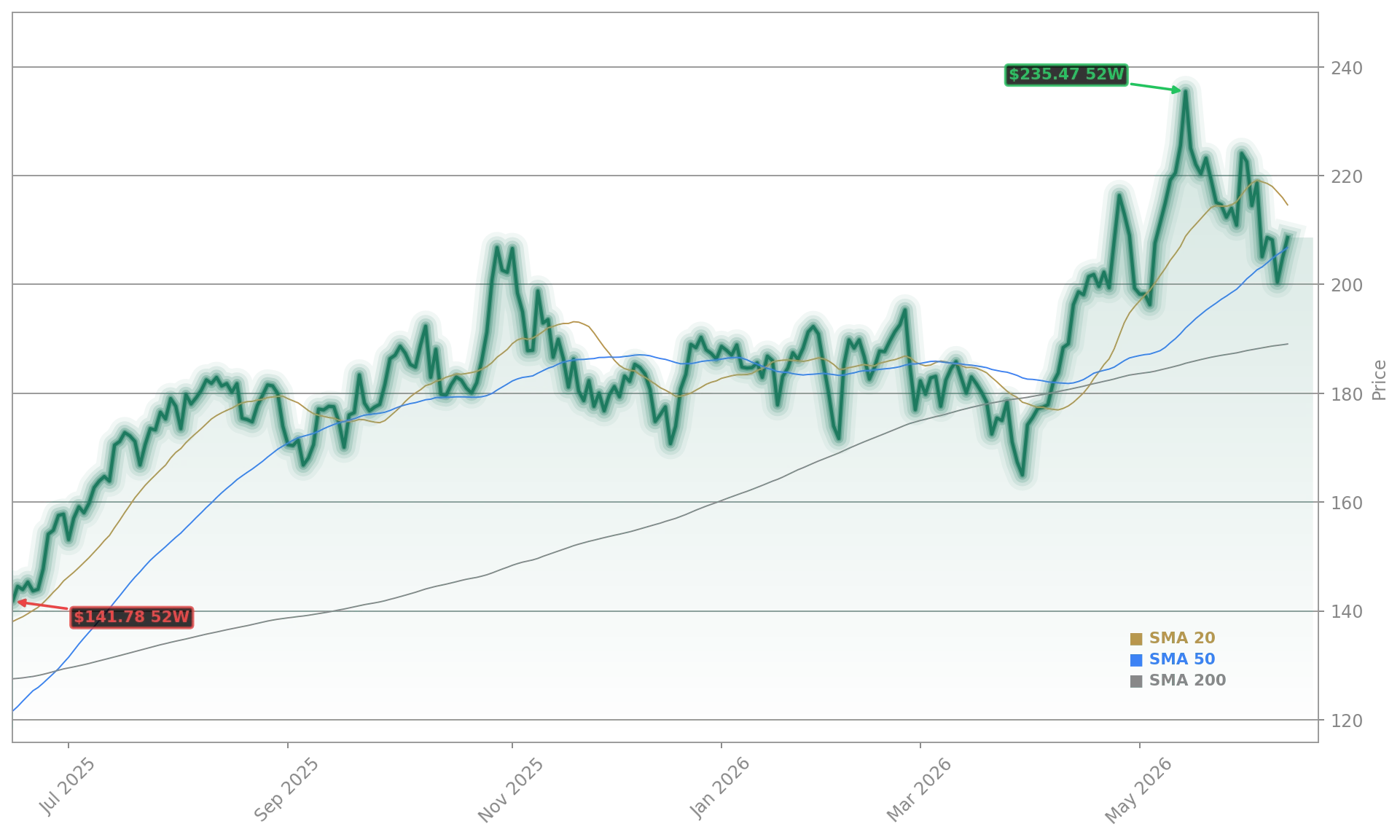

Even so, the stock response has been restrained. NVIDIA shares closed at $223.47 on Wednesday, up 1.30%, and were indicated at $222.91 in premarket trading Thursday, down 0.25%. That leaves the stock below its 52-week high of $236.54, so this is not a fresh breakout. The market appears to be pricing in not just strong execution, but repeated blowout quarters.

The forward view is part of that tension. NVIDIA projected current-quarter revenue of around $91 billion, ahead of the broader analyst consensus, but still shy of some of the highest buyside expectations that had built up after the stock’s sharp run since late March.

How is NVIDIA widening its AI story?

Management used the quarter to make a broader case that NVIDIA is no longer just a GPU story. Chief Executive Jensen Huang said demand remains extremely strong and suggested supply constraints could persist for the next-generation Vera Rubin systems, with initial shipments expected in the second half of the year.

The company is also pushing investors to think beyond hyperscalers. NVIDIA highlighted growing opportunities with enterprise customers, governments, robotics, autonomous systems, and what Huang described as physical AI. It also said CPUs could contribute $20 billion in revenue this year, an important signal as the company expands further into full-stack data center infrastructure and competes more directly with AMD, Intel, and custom silicon efforts from cloud giants such as Alphabet and Amazon.

One notable strategic overhang remains China. Huang said NVIDIA has largely conceded that AI chip market to Huawei under current export restrictions. The company is effectively assuming no China contribution in its near-term outlook, which some investors see as conservative positioning and others see as a cap on upside.

What do capital returns and analysts say about NVIDIA?

The biggest capital allocation surprise in these NVIDIA Earnings was shareholder return. NVIDIA raised its quarterly dividend from $0.01 to $0.25 per share and authorized an additional $80 billion in stock repurchases. That move suggests a more mature cash-return profile, even as the company continues investing heavily across supply chain, software, and AI infrastructure.

Analyst reactions have remained broadly positive. Jefferies lifted its price target to $300 and kept a Buy rating. Bank of America raised its target to $350 with a Buy rating. Goldman Sachs increased its target to $285, while Bernstein moved to $315 and reiterated Outperform. Deutsche Bank raised its target to $255 but stayed at Hold. Citigroup also highlighted the new data center revenue split as a positive step for transparency around non-hyperscaler demand.

Outside the earnings print, NVIDIA’s ecosystem keeps widening. Reuters reported a Taiwan investigation into alleged illegal exports of AI servers carrying NVIDIA chips, a reminder of how central the company’s hardware has become to global controls and demand. Separately, Ubergizmo reported a new restaurant AI partnership with Yum Brands, extending NVIDIA’s reach into real-world enterprise deployments.

Related Coverage: Investors tracking the bigger setup around this report can also read this analysis of how NVIDIA’s $91 billion outlook is reshaping the AI trade. That piece looks at the same earnings cycle from a broader market perspective and helps frame why expectations for NVIDIA have become so unusually difficult to beat.

NVIDIA Earnings confirmed that the company is still setting the pace in AI infrastructure, but they also showed that Wall Street now expects excellence as the baseline. For investors, the next test is whether new growth pillars like CPUs, robotics, and enterprise AI can support the stock as competition rises and the bar keeps moving higher.

The demand in China is quite large. Huawei is very, very strong. We’ve really largely conceded that market to them.— Jensen Huang

Fazit folgt.