Can AMD AI Strategy turn the inference shift into a real challenge to NVIDIA’s dominance?

Why is AMD AI Strategy gaining traction?

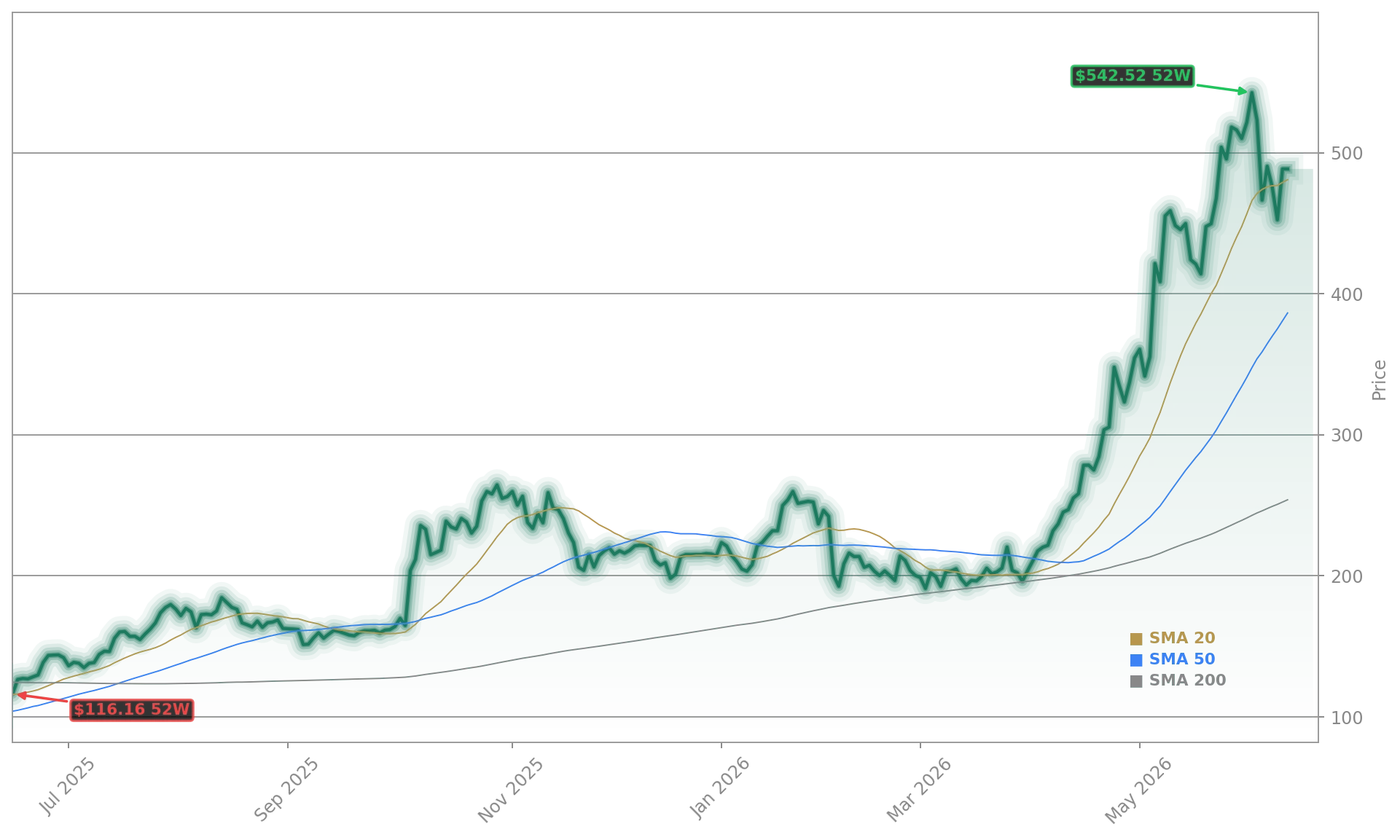

AMD was among the standout gainers in the semiconductor group on Wednesday as investors rotated back into AI infrastructure names after a recent pullback. The latest move also pushed the stock above Citigroup’s new $460 target and closer to Evercore ISI’s far more aggressive $579 objective, showing how quickly sentiment has turned. For Wall Street, the current debate is no longer just about who wins AI training. It is increasingly about who can monetize inference efficiently at scale.

That shift matters for AMD because its story is broader than GPUs alone. The company sells server CPUs, accelerators, embedded chips, and client processors, giving it several ways to benefit from data center spending. In Q1 2026, AMD posted revenue of $10.25 billion, up 38% year over year, while Data Center revenue climbed 57% to $5.78 billion. Management also guided Q2 revenue to about $11.2 billion, implying roughly 46% growth.

Can AMD challenge NVIDIA?

NVIDIA still sets the pace in AI accelerators, but AMD is no longer viewed as a distant challenger. Investors increasingly see a broader competitive landscape in which hyperscalers want alternatives, internal custom silicon, and better economics around cost per token and total cost of ownership. Evercore ISI said its Q1 channel checks pointed to AI workloads shifting from a training-heavy market toward an inference-led market by the end of 2026. That is central to the AMD AI Strategy because inference typically rewards memory capacity, system efficiency, and balanced CPU-GPU architectures.

AMD appears well positioned for that transition. Inference and agentic AI use cases often require a higher CPU-to-GPU ratio than training workloads, and AMD already has a strong position in high-performance data center CPUs through EPYC. Its chiplet-based GPU approach is also seen as a potential advantage in memory-sensitive inference deployments. That helps explain why some investors are re-rating AMD as more than a second-source AI trade to NVIDIA.

Still, competition is intensifying. Cloud giants including Apple peers and other hyperscalers are developing in-house AI chips, while rivals such as Intel, Marvell, Arm, and platform customers continue to seek alternatives to premium GPU pricing. For AMD, winning share may depend less on matching NVIDIA feature for feature and more on delivering a compelling return on investment.

What are analysts and investors watching?

Citigroup raised its price target on AMD to $460 from $358 while keeping a Neutral rating, reflecting a larger view of the CPU market that now includes AI head nodes and agentic CPU applications. Evercore ISI reiterated Outperform and lifted its target to $579 from $358, arguing that the market is beginning to value the inference opportunity more seriously. CLSA also upgraded AMD to Outperform, reinforcing the view that the AI chip rally may still have room to run.

Institutional interest remains firm as well. Recent filings highlighted added positions from Adell Harriman & Carpenter and Tredje AP fonden, though investors are also balancing that against insider sales, including a Rule 10b5-1 sale by AMD Chief Technology Officer Mark Papermaster. Meanwhile, AMD’s enterprise AI partnership with Rackspace points to another angle in the AMD AI Strategy: regulated and managed infrastructure deployments beyond hyperscale customers.

Valuation remains the biggest risk. AMD’s rally has been dramatic, and several marketwide valuation gauges are flashing caution across US equities. That does not invalidate the growth case, but it raises the bar. Investors will now watch Tesla-style market leadership dynamics in AI hardware, NVIDIA’s upcoming earnings, and whether AMD can turn MI450 and Helios interest into sustained share gains.

Related Coverage: Investors tracking near-term execution should also read AMD AI Strategy -2.6% as MI450 Ramp Keeps Bulls Watching. That report digs deeper into the MI450 product cycle, partnership momentum, and why the recent pullback had not broken the broader bull case. It also adds useful context for how product ramps could influence the next leg of AMD sentiment.

We delivered an outstanding first quarter, driven by accelerating demand for AI infrastructure… Customer engagement around MI450 Series and Helios is strengthening, with leading customer forecasts exceeding our initial expectations.— Lisa Su

AMD AI Strategy now looks increasingly tied to inference economics, CPU attach, and real-world deployment wins rather than headline AI excitement alone. If AMD keeps converting that positioning into revenue growth and customer ramps, the stock could remain a key Wall Street AI contender through the rest of 2026.