Could limited H200 access in China be the catalyst that resets NVIDIA’s growth narrative ahead of earnings?

What drove NVIDIA’s +8.5% weekly surge?

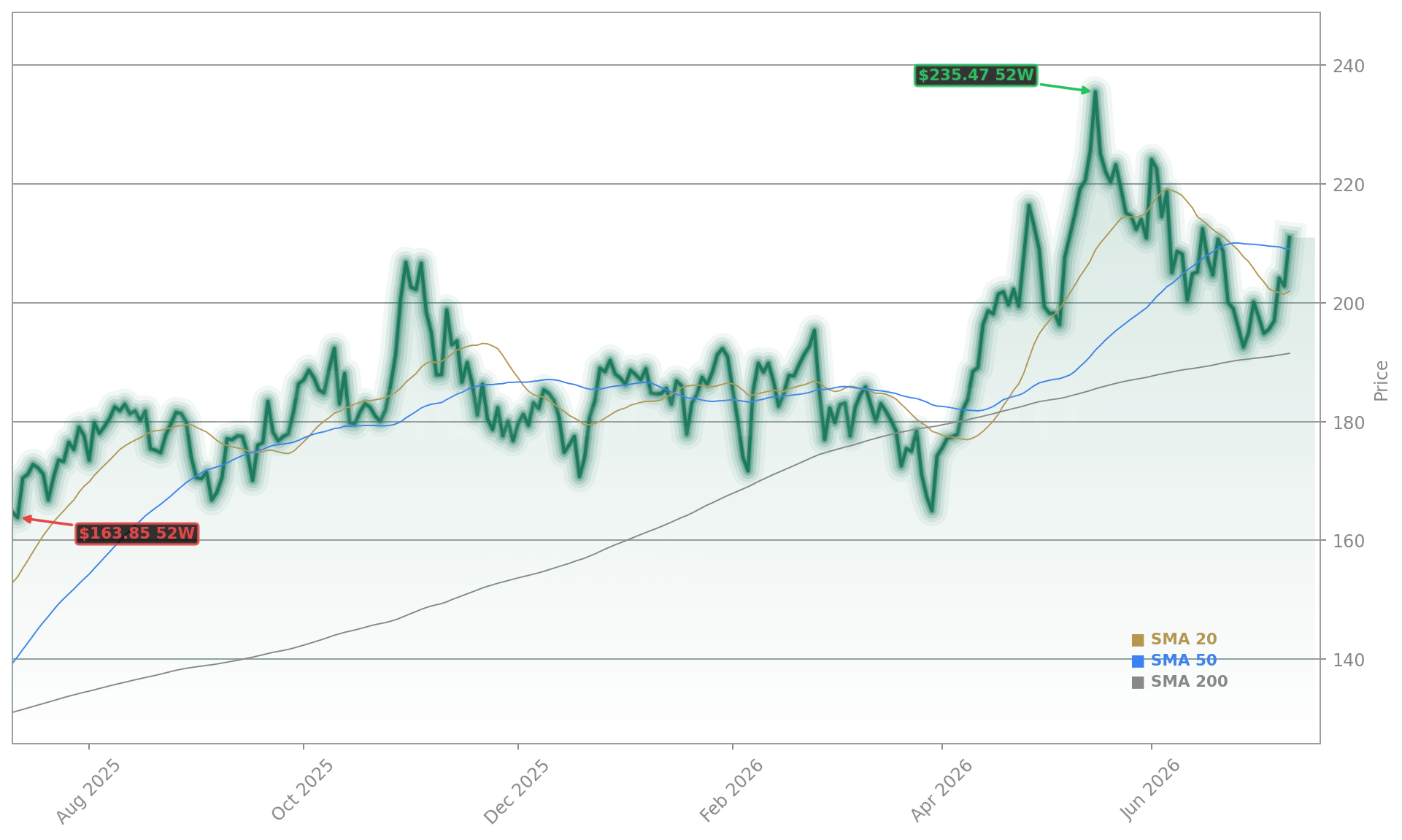

This week, NVIDIA Corporation posted a sharp +8.5% gain — from Monday’s open of $194.42 to Friday’s close of $210.96 — with a weekly high of $211.00 and low of $191.14. The rally was decisively anchored in two catalysts: first, credible reporting from The Information that Beijing would allow top-tier Chinese AI firms to purchase a limited number of H200 chips — a direct and material easing of prior restrictions. Second, SpaceX’s announcement of Grok 4.5, trained across “tens of thousands” of NVIDIA GB300 chips and ranked third globally by Artificial Analysis — validating NVIDIA’s hardware as the irreplaceable foundation for frontier AI training. These developments overrode earlier concerns about Kyber delays (dismissed by Mizuho as “noise”) and DeepSeek’s in-house chip efforts, shifting sentiment from defensive to opportunistic. The two outlier days — Wednesday’s +3.7% and Friday’s +4.0% — directly tracked these headlines, turning sentiment decisively bullish.

How did NVIDIA China AI Chips reshape the week’s narrative?

The NVIDIA China AI Chips theme dominated investor discourse and drove the week’s strongest intraday moves. For the first time since late 2025, credible reports confirmed that Chinese AI leaders — Alibaba, ByteDance, and DeepSeek — had received verbal assurances from regulators permitting limited H200 imports to address acute supply shortages. This wasn’t full reinstatement, but a calibrated, high-impact concession — one that Bank of America analysts immediately flagged as a key near-term catalyst for data center revenue visibility. It also clarified that NVIDIA’s China strategy remains intact: not reliant on volume, but on premium-tier, high-margin AI infrastructure access. The timing was critical — coming just before the August 26 earnings report — and directly countered bearish narratives about irreversible market share erosion. As TradingKey noted in its Alibaba analysis, this access is already fueling a 12% two-day rally in BABA stock and underpins its $160 price target — a strong signal of downstream demand validation.

What did analysts say about NVIDIA’s valuation and moat?

Analyst confidence surged this week, with multiple firms doubling down on NVIDIA’s structural advantages. Bank of America reiterated its “Buy” rating and $350 price target — implying 78% upside — calling NVIDIA’s pricing power and ecosystem moat “completely unappreciated” and its current 18x forward P/E a “7-year low.” Morgan Stanley maintained NVIDIA as its top semiconductor pick despite its large market cap, citing resilient hyperscaler demand, sovereign data center growth, and on-schedule Vera Rubin shipments. Citigroup analysts highlighted NVIDIA’s unmatched ROE of 33.06% — 25.16% above the semiconductor industry average — as proof of its superior capital allocation and pricing discipline. Meanwhile, Needham and DA Davidson both held their $270 and $300 targets, respectively, emphasizing the company’s “hardware + software + networking” convergence as an insurmountable barrier to competition.

What’s next for NVIDIA — catalysts and open questions?

Next week brings three key inflection points. First, TSMC’s July 16 earnings report — a critical barometer for AI chip supply constraints and wafer-start availability, given NVIDIA’s absolute dependence on TSMC’s N3 and N2 processes. Second, the continued rollout of Vera Rubin infrastructure — with Samsung’s mass production of the PM1763 PCIe 6.0 SSD confirming the ecosystem’s readiness. Third, the evolving geopolitical calculus: while the H200 access breakthrough is real, questions remain about long-term licensing pathways, Vera Rubin export eligibility, and whether this signals a broader U.S.-China AI détente or tactical recalibration. Investors will also monitor whether Grok 4.5’s performance triggers follow-on model training contracts for NVIDIA’s GB300 and next-gen platforms.

Why does this week matter for long-term investors?

This week wasn’t about short-term noise — it was about validation. The NVIDIA China AI Chips access breakthrough confirmed that NVIDIA retains strategic leverage in the world’s second-largest AI market, even under sanctions. The Grok 4.5 validation reaffirmed its hardware as the non-negotiable engine of frontier AI — not just for startups, but for SpaceX’s most ambitious AI initiatives. And the analyst consensus — from Bank of America to Morgan Stanley — coalesced around NVIDIA’s enduring moat: not just chips, but the entire AI stack. For investors, this means NVIDIA China AI Chips are no longer a regulatory risk — they’re a growth lever. The stock’s move above $210 and convergence of key moving averages near $203 signal a new, higher base. With strong free cash flow, a low 0.06 debt-to-equity ratio, and a forward P/E still below peers, the setup is clear: buy the strength, not the dip. NVIDIA China AI Chips are now a core, actionable growth pillar — and the earnings report on August 26 is the next major catalyst to confirm it.

NVIDIA China Access: $20B Boom Fuels AI Chip Outlook details how the H200 breakthrough is already unlocking a $20 billion near-term revenue tailwind, with Maik Kemper noting NVIDIA’s “roadmap is intact” and Blackwell deliveries accelerating. The article underscores that this isn’t incremental — it’s foundational to NVIDIA’s 2026 China growth thesis. Meanwhile, RKL Wealth Management’s portfolio update reveals that even as it trimmed NVIDIA by 10.4%, the stock remains its 18th-largest holding — a sign of strategic conviction, not retreat. Finally, Jim Cramer’s latest analysis powerfully reframes NVIDIA’s valuation: he calls it “the most proprietary chip company in history,” yet notes its forward P/E sits below SanDisk — proof the market still undervalues its software moat and CUDA ecosystem.

Nvidia is taking the gloves off with its open source model. They will own the whole stack.— Jason Calacanis

Fazit folgt.