Could NVIDIA China become the market’s next upside surprise just as Wall Street starts betting on a broader AI rebound?

Is NVIDIA China Finally Opening?

China’s reported decision to allow Alibaba, ByteDance, and DeepSeek to purchase a limited volume of NVIDIA H200 chips marks the most credible opening in over 18 months. According to The Information, Beijing’s conditional approval — aimed at easing AI chip shortages — could unlock up to 200,000 units, representing a meaningful, albeit incremental, revenue lift for NVIDIA. Crucially, the company has baked zero China revenue into its fiscal 2026 guidance, meaning any realized sales constitute pure upside. Analyst Dan Ives of Wedbush reaffirmed this is a net positive, noting that investors have “completely priced out” any China contribution — making even modest H200 shipments a powerful sentiment catalyst. For U.S. portfolios, NVIDIA China exposure remains a high-conviction, low-probability option — but one that could shift rapidly if orders materialize ahead of the August 26 earnings report.

What’s Driving NVIDIA’s CPU Breakthrough?

NVIDIA’s Vera Rubin CPU platform is no longer theoretical — it’s shipping. Perplexity AI confirmed it will deploy Vera CPUs for AI agent workloads, citing 1.5x performance gains over traditional CPUs. OpenAI, Anthropic, and Oracle are also lining up as early adopters. With NVIDIA targeting $20 billion in CPU revenue this year — against a $200 billion total addressable market — the move signals a strategic pivot from GPU dominance to full-stack AI infrastructure. This directly challenges Intel and AMD, whose data center CPU businesses have struggled to gain traction against cloud-optimized architectures. For investors, Vera isn’t just diversification: it’s a structural moat expansion, reinforcing NVIDIA’s role as the de facto operating system for AI compute — not just the chip supplier.

Why Is Bank of America So Bullish?

Bank of America has firmly reiterated its Buy rating on NVIDIA, lifting its price target to $350 — implying 78% upside from current levels. Analyst Vivek Arya argues the market is mispricing NVIDIA’s durability, citing a seven-year low forward P/E of 18x — 30–35% cheaper than mega-cap tech peers despite 85% YoY data center revenue growth. BofA dismisses fears around HBM cost pressure, asserting NVIDIA’s pricing power, scale, and $119 billion supply chain investment insulate margins, which are expected to hold in the mid-70% range. The firm also reaffirms NVIDIA’s projected 65–70% AI accelerator market share through 2030 — a figure validated by its 97% server GPU dominance at year-end 2025.

How Does This Fit Into the Broader AI Trade?

While the Philadelphia Semiconductor Index (SOX) surged 74% YTD — powered by Micron’s 229% rally — NVIDIA lagged with just a 5.6% gain. That underperformance created a rare valuation dislocation: NVIDIA now trades below the S&P 500’s 20x forward P/E and below the Nasdaq-100’s 23x. Yet its fundamentals remain unmatched — $81.6 billion in Q1 fiscal 2027 revenue, 115% YoY hyperscaler sales growth, and a $1.5 trillion global AI infrastructure spend forecast for 2026. The rotation into memory and storage names reflects tactical trading, not a fundamental shift. As DA Davidson’s Gil Luria notes, NVIDIA remains ‘sub-market multiple’ and ‘well-priced if AI demand continues’ — a view echoed by RBC Capital Markets, which recently upgraded its rating to ‘Outperform’ on Vera and Kyber execution confidence.

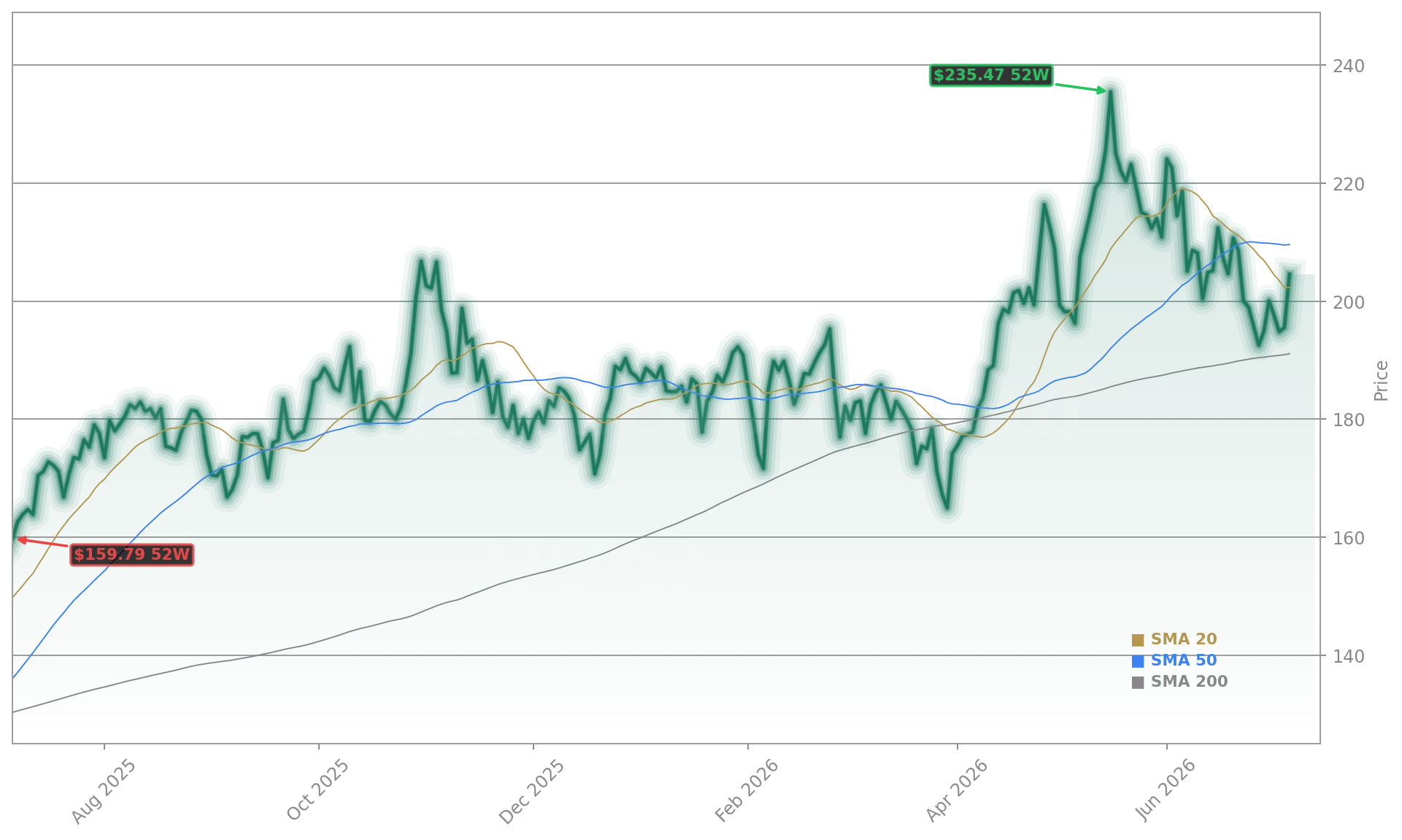

Is the Technical Setup Finally Turning?

NVIDIA is trading at a seven-year low 18 times forward P.E. ratio, representing a massive 30–35% valuation discount compared to its mega-cap technology peers.— Vivek Arya, Bank of America Global Research

Technically, NVIDIA has broken key resistance at $200 — a level that had capped rallies since May. With shares now trading 1.8% above their 20-day moving average and holding well above the 200-day SMA ($191.37), the near-term trend is shifting from defensive to constructive. Volume has spiked on the China and Vera news, and options activity shows renewed call interest — particularly in August and September $210–$225 strikes. For S&P 500 and Nasdaq investors, NVIDIA’s 6.5% weight in major tech ETFs means its rebound has outsized index implications. With Q2 earnings just weeks away, the stock is no longer priced for perfection — but for resilience. And that’s exactly what Wall Street is beginning to recognize.