Can NVIDIA China Access unlock a new growth leg just as Wall Street starts treating the AI leader like a bargain?

What Does NVIDIA China Access Mean for Q3 Earnings?

NVIDIA China Access is now operational: Beijing has authorized Chinese AI firms — including Alibaba, ByteDance, and DeepSeq — to purchase up to 200,000 H200 chips, following U.S. licensing approval. This isn’t theoretical — it’s a $20 billion near-term revenue pipeline, directly supporting NVIDIA’s guidance for accelerating data center revenue in Q3 2026. With supply-chain commitments now totaling $119 billion across Blackwell and Vera Rubin platforms, the H200 greenlight adds critical liquidity to NVIDIA’s China revenue stream, which had been constrained since late 2023. Crucially, this NVIDIA China Access doesn’t require new chip redesigns or export licenses per shipment — it’s a scalable, policy-backed channel that Wall Street analysts now model into Q3 and Q4 forecasts.

How Is Nemotron 3 Ultra Changing the AI Stack?

NVIDIA’s Nemotron 3 Ultra isn’t just another open-source model — it’s a strategic moat expander. By slashing inference costs by 90% versus closed alternatives, it transforms NVIDIA from a hardware vendor into a full-stack AI infrastructure partner. The model runs efficiently on existing H200 and GB300 systems, accelerating adoption across cost-sensitive enterprise and government clients. This directly complements NVIDIA’s hardware dominance: with a 97% GPU market share in AI training (Bloomberg), Nemotron 3 Ultra ensures that software lock-in follows hardware lock-in. Competitors like Meta and Google are building custom chips, but none yet offer a comparable open, optimized, inference-optimized stack — making NVIDIA China Access even more valuable in markets that prioritize cost control and local model sovereignty.

Why Is Wall Street Doubling Down on NVIDIA?

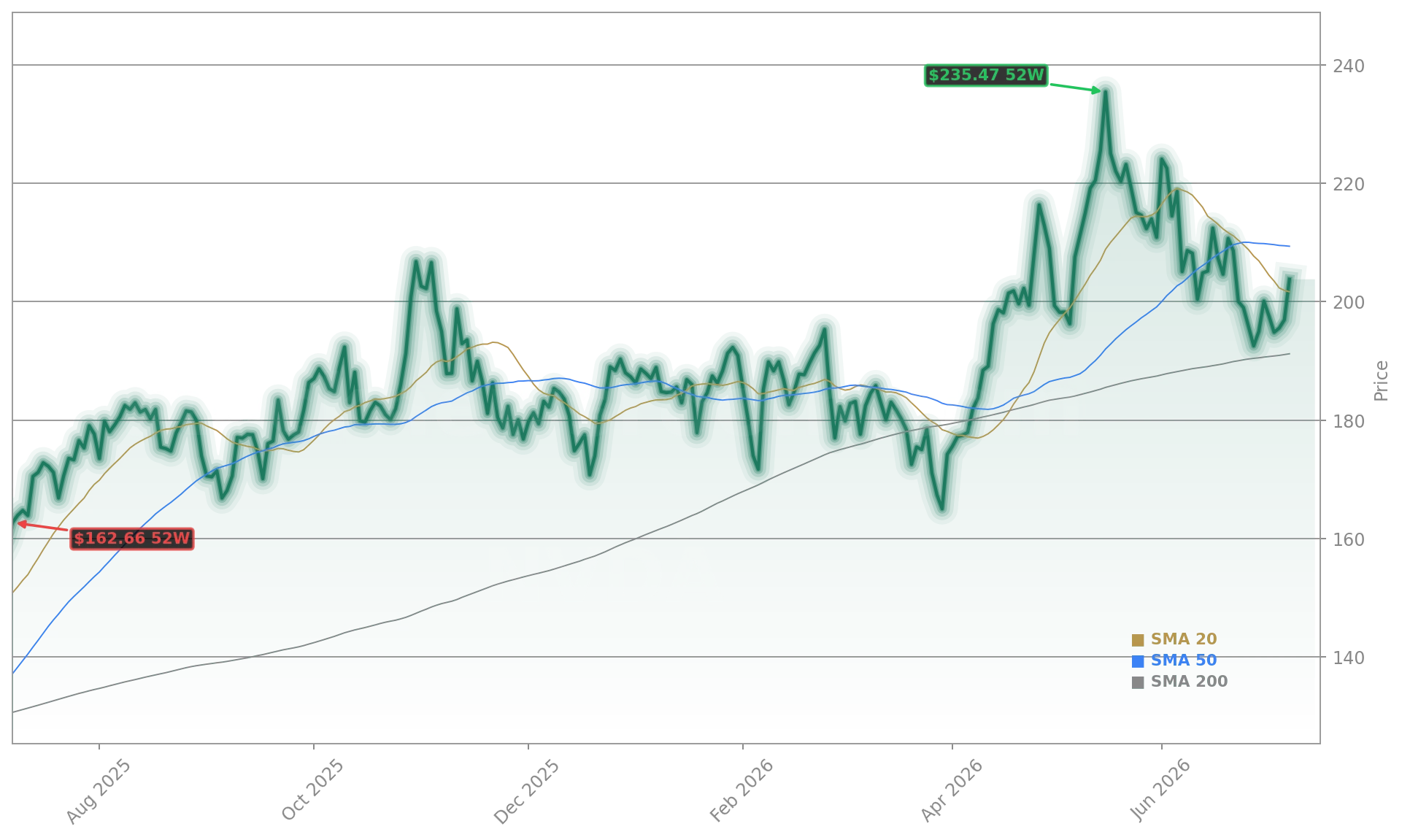

Bank of America analyst Vivek Arya reiterated his Buy rating and $350 price target on July 8, calling NVIDIA’s current forward P/E of 22x its lowest in seven years — a valuation that “takes the stock back to pre-AI boom territory.” Arya dismissed concerns over memory costs, custom chip competition, and cash deployment as overblown, noting NVIDIA’s data center segment grew 92% YoY to $75.2 billion and that its networking revenue surged 199%. He emphasized that NVIDIA’s $1 trillion in revenue visibility over 2026–2027 is anchored not just by chip sales, but by end-to-end systems — including Kyber rack-scale architecture, which NVIDIA confirmed remains on track for 2027 despite SemiAnalysis’ delay speculation. This NVIDIA China Access and Nemotron progress reinforce Arya’s thesis: “a unique, durable growth franchise” priced like a mature industrial.

How Does NVIDIA Compare to Its AI Infrastructure Peers?

NVIDIA’s roadmap is intact. We’re delivering on Blackwell, and Vera Rubin is on track for second-half 2026 volume shipments.— Jensen Huang, CEO of NVIDIA Corporation

While Advanced Micro Devices surged 141.79% YTD and Micron Technology jumped 8% on memory demand, NVIDIA’s 9.58% YTD gain reflects a deliberate valuation reset — not weakness. Unlike AMD, which relies on hyperscaler design wins, or Marvell, which supplies connectivity silicon, NVIDIA controls the entire AI stack: training (Blackwell), inference (Nemotron + GB300), networking (Spectrum-X), and soon CPU (Rubin). Meta’s Iris chip — entering production in September — won’t displace NVIDIA; it will augment it. As Jim Cramer noted on Mad Money, NVIDIA actively funds “neoclouds” like CoreWeave and Nebius to counter hyperscaler vertical integration. That ecosystem strategy, paired with NVIDIA China Access, makes NVIDIA less vulnerable to single-customer risk than peers — a key differentiator for S&P 500 and NASDAQ investors seeking AI exposure with structural resilience.