Why did AMD plunge nearly 8% even as revenue, margins, and AI demand all pointed in the opposite direction?

Why Did AMD Drop Despite Strong Q1 Data?

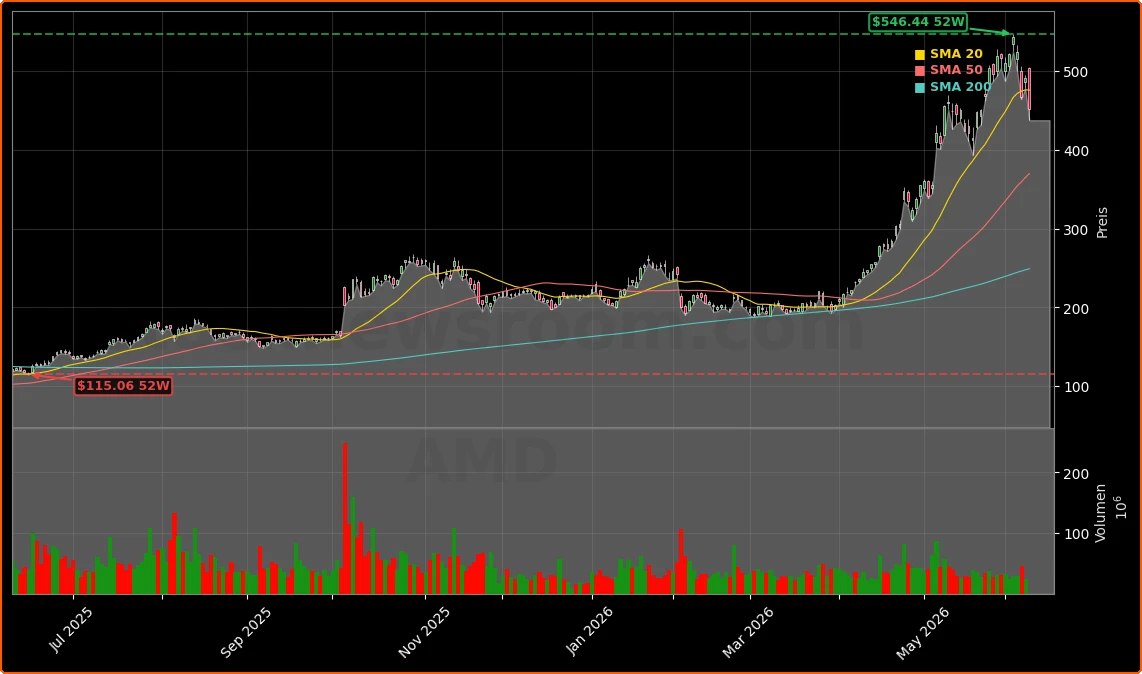

Advanced Micro Devices, Inc. slid sharply on Tuesday — down 7.82% to $452.00 — as the NASDAQ 100 contended with a 3% intraday pullback driven by semiconductor concentration risk. The sell-off followed AMD’s 129% year-to-date rally and came with no new negative catalyst. Instead, analysts point to aggressive profit-taking and rotation out of high-momentum AI names. The VIX rose 18% week-over-week to 18.92, signaling rising hedging activity. Notably, AMD’s Q1 2026 results were exceptionally strong: $10.25 billion in revenue (up 38% YoY), with data center segment revenue hitting $5.78 billion — a 57% increase. Gross margins expanded 300 basis points to 53%, and operating income jumped 83% to $1.48 billion. That resilience underscores why the AMD AI Forecast remains anchored in fundamentals — not sentiment.

How Does AMD Compare to NVIDIA and Intel?

While NVIDIA continues to dominate AI accelerator market share and trades at a lower forward P/OpInc multiple, AMD’s diversification remains a strategic advantage. Unlike NVIDIA, which draws over 90% of data center revenue from GPUs, AMD’s data center segment contributes 57% of total revenue — and includes CPUs, accelerators, and networking silicon. Intel reported Q1 data center and AI revenue up 22%, but its 291% overvaluation signal (per one model) and lower gross margin profile contrast with AMD’s more balanced execution. Gil Luria of DA Davidson notes AMD and Intel face higher valuation vulnerability as AI IPOs approach — but core AI infrastructure demand remains structurally sound. Meanwhile, Marvell Technology (MRVL) rose 4% on the same day, underscoring investor preference for ‘picks-and-shovels’ exposure across the AI stack.

What Does the AMD AI Forecast Say About 2026–2027?

The AMD AI Forecast is now explicitly tied to multi-year supply constraints. Mizuho’s $615 price target — raised from $515 — hinges on AI infrastructure demand staying supply-constrained through 2027, particularly for agentic AI workloads and next-gen hyperscaler deployments. That forecast aligns with AMD’s £2 billion UK investment to accelerate AI innovation and its JPMorgan Quantum-AI research partnership — both reinforcing its role as a sovereign AI infrastructure enabler. Importantly, the AMD AI Forecast also incorporates geopolitical tailwinds: Beijing’s push to use domestic suppliers like Huawei for 80% of AI chips indirectly validates AMD’s position as a critical non-Chinese alternative for Western hyperscalers and governments. That dynamic supports long-duration revenue visibility — even as short-term trading flows remain volatile.

Are Institutions Buying or Selling?

Institutional activity is bifurcated — revealing conviction beneath the noise. X Square Capital LLC sold 17,259 shares (a 27.7% reduction), yet Vanguard and State Street increased stakes. Endeavor Private Wealth Inc. acquired 1,298 new shares — a $278,000 position. Meanwhile, options data shows bullish sentiment: a $400.00 strike put trade on June 12 drew $40.4K in premium, signaling confidence in a near-term floor. This divergence reflects a broader Wall Street narrative: AMD is no longer just a momentum play — it’s a core holding for AI infrastructure exposure in portfolios tracking the S&P 500 and NASDAQ 100. Its 4.7% weighting in the ARTY fund — alongside NVIDIA, Broadcom, and Oracle — confirms its strategic weight among AI-focused allocations.

What’s Next for AMD Investors?

AI infrastructure demand is expected to stay supply-constrained through 2027, supporting continued pricing power and revenue growth for AMD’s next-generation platforms.— Mizuho Securities

With Q2 2026 earnings still three months away, the path forward hinges on execution of the MI450 Series ramp, Helios platform adoption, and hyperscaler contract renewals. Analysts at Mizuho emphasize that memory and CPU supply constraints may intensify late in 2026 — creating both risk and upside for AMD’s integrated offerings. The stock’s current P/E of 175x demands flawless delivery — but its diversified product portfolio and sovereign AI partnerships provide a buffer that pure-play GPU vendors lack. For long-term investors, the AMD AI Forecast remains a cornerstone thesis — not a speculative call.